This article was written in collaboration with Endowus. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

If you are a regular reader of DollarsAndSense, it’s safe to assume that you understand the importance of investing. The simple fact is that for most of us, we will eventually reach the stage in our lives where we would stop working and rely on other forms of income.

While CPF savings provide some basic income via CPF LIFE, the amount may not be sufficient for those who need more so that we can enjoy the desired lifestyle we want during our golden years. For this, we need our investment to generate an income that can fund our retirement.

Capital Gain VS Dividend Income? Investment Returns For Different Purposes

When it comes to investing, the aim is to generate high returns, or returns that are in line with market expectation, and that at least beat the risk-free rate.

Generally speaking, investment returns can occur in two forms. We can earn returns via capital gain — which is when the prices of the shares we invest in increase — or through dividend income — when the investments pay us dividends or coupon payments.

While both capital gain and dividend income are considered as returns, investors can’t ignore how these returns are derived.

For example, with capital gains, returns can only be realised when the investment is sold at a higher price than what it was purchased at. Meanwhile, dividends and coupon payments are paid out to shareholders or bondholders directly by the company, which means these returns can be realised as soon as they are paid out.

If we are still working, we may not be too concerned with dividends and coupon payments since we have a job that gives us the regular income we need. At this age, our aim, typically, is to grow our wealth over the long term.

For retirees, or those looking to build an investment portfolio for their retirement, a portfolio that is only centered around high-growth companies designed to capture capital gain may not directly serve our needs. This is because our primary objective isn’t just to build wealth, but also to ensure that we can easily access this wealth and get a steady stream of income that can fund our retirement.

A Case Of Two Portfolios: Which Is Better For Our Retirement?

If the main objective for investing is to fund our retirement, then the way we construct our portfolio needs to be tailored for that.

High returns are great, but they are less valuable if the way these returns are realised isn’t suitable for our retirement.

Here’s an extreme, hypothetical example. Suppose I invest well in private companies during my younger days. Having invested $50,000 each in 5 different companies (total of $250,000), I now enter retirement with my shareholdings in two of these companies being worth $500,000 each (total of $1 million). The other three companies failed.

On paper, this is great. Having a portfolio worth $1 million should mean a secured retirement. However, the challenge here is how I can make this private business portfolio valuable for my retirement. For me to recognise the gains in my investment, I need to be able to liquidate my portfolio. For example, I must sell my shareholding in the businesses to someone who is willing to purchase it from me to realise this profit to fund our retirement.

The above scenario illustrates the challenge that an asset-rich, cash-poor retiree may have. Even though the retiree may have assets that are worth a large sum of money, the person is unable to effectively use them to fund his retirement.

In contrast, if we were to own a portfolio of equities and bonds worth $1 million that pays out passive income (via dividends and coupon payment), this can be easily used to fund our retirement. Such a portfolio would allow us to realise our returns (the passive income) without the need to sell off our equities and bonds. A well-selected investment portfolio may also increase in value over time, while giving us returns on a regular basis.

In both scenarios, the portfolio is worth $1 million. However, you can see that owning an investment portfolio that gives us passive income is a more ideal retirement plan than owning private businesses that we can’t monetise without first selling our stake in the company.

When A Portfolio Is Ill-Suited For Our Golden Years

Similarly, when it comes to our own investment portfolio, there are portfolios that are constructed primarily for capital gains, while other portfolios may focus on providing a stream of regular income.

The problem for many retail investors, even those of us with investment experiences, is that we may spend the bulk of our working years constructing a portfolio that is designed for capital gain, only to realise that what we need for our retirement is a portfolio that gives us stable, regular income.

At that point in time, even if we want to switch our portfolio, it wouldn’t be easy. We will need to sell shares that we have spent years analysing and are already comfortable owning, and to instead, start learning how to invest in shares or bonds that we may not be as familiar with, but that are meant to give us a regular income.

Endowus Income Portfolios: Passive Income Solutions For Every Stage Of Life

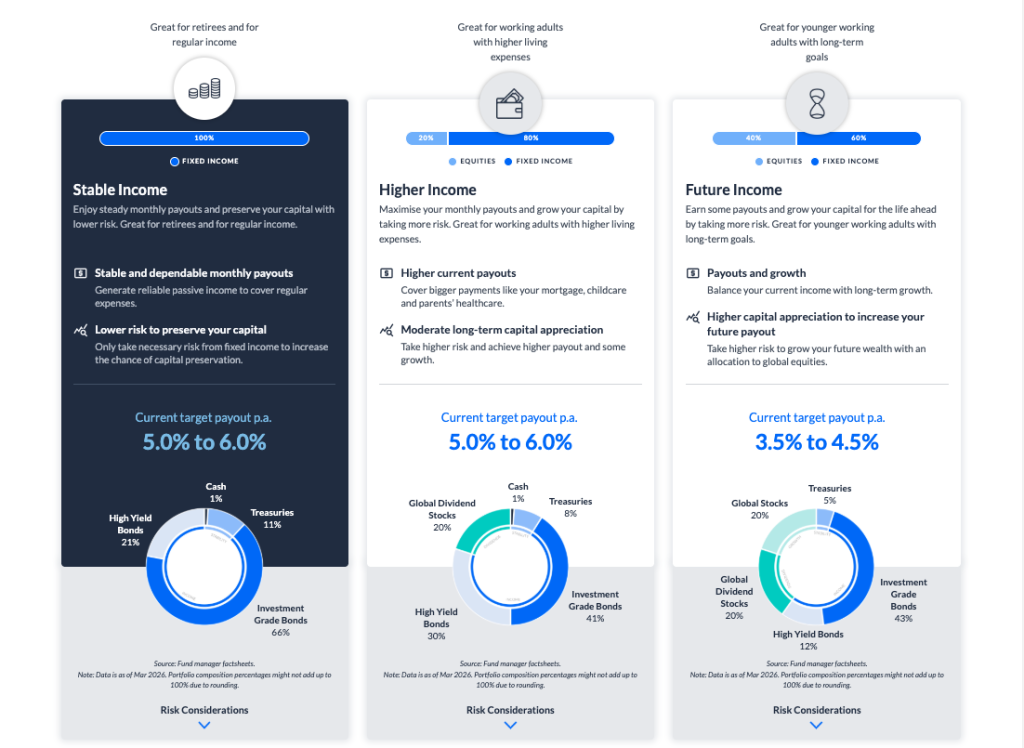

Endowus offers three Income Portfolios designed to provide regular payouts while seeking to preserve or grow investors’ capital: Stable Income, Higher Income and Future Income. The portfolios have different allocations and risk levels to cater to investors with different income requirements and investment horizons.

One thing that we really like about the Endowus Income portfolios is that the company recognises the varying needs of income investors who are at different stages in their lives. For example, as a working adult, I can afford to take more risk with my investment portfolio as I still have a long investment horizon. By contrast, my parents, who are retired, would prefer a more stable portfolio that gives them regular monthly payouts.

With Endowus, we can choose from three different income portfolios – Stable Income, Higher Income, and Future Income.

Stable Income allocates 100% of our investment funds to fixed income. This makes the portfolio less volatile and risky, while giving us better payout predictability. Such a portfolio would be ideal for retirees and those who are seeking regular, stable income. It pays out an income monthly.

Higher Income allocates 20% of our investment funds to equities with the remaining 80% in fixed income. With a slightly higher payout target as well, this makes it suitable for working adults with higher living expenses who have higher risk tolerance and who want a higher payout. It pays out an income monthly.

Future Income allocates 40% of our investment funds to equities with the remaining 60% in fixed income. It has a lower payout target, but the highest estimated capital appreciation among the three income portfolios since it has the highest weightage in equities. Young working adults who don’t need high payouts yet and would like to grow their income portfolio over time can opt for this. It pays out an income either monthly or quarterly.

These target payouts are estimates rather than guaranteed returns. The actual distributions and value of the portfolios can rise or fall depending on market conditions and decisions made by the underlying fund managers.

With Endowus, You Don’t Need To Choose Income Over Capital Gain

One of the things to highlight for investors is that there is no need to choose between income and capital gain. As a retail investor, it’s perfectly fine for us to have portfolios that serve both needs concurrently.

So, if like us, you are an existing investor of the Endowus Flagship portfolio, you should remain invested in it. However, if you are also keen to build a separate portfolio that can give you regular income, then you can pick an Endowus Income portfolio.

Endowus Income Portfolios Are Suitable For Investors Of All Ages

Today, most robo-advisory portfolios would typically advise investors to take on a long-term investment horizon, and for good reason. With a longer investment time horizon, we can ride out short-term volatility in the financial market.

Unfortunately, what this also means is that older investors are sometimes excluded. With the Endowus Income portfolios – particularly the Stable Income portfolio – older investors such as retirees can choose to immediately switch to an income-generating portfolio if they want, without the hassle of needing the knowledge and time to choose a well-diversified portfolio of income-generating assets.

So if you are someone who currently has a large portfolio of growth companies but are now prioritising a steady stream of income over growth for your investment portfolio, you can liquidate your investment holdings and invest in the Endowus Income portfolio.

To be clear, and this is what Endowus says, the “Income Portfolios are different from the other Endowus Core or Satellite portfolios as it has a specific goal in mind — to pay out a regular and passive income stream for investors.”

This means that the “primary objective (of providing a payout) overrides other objectives in investing such as maximising returns. If you do not need or want income distributed from your investment, you probably do not need to have an income portfolio.”

For investors who don’t want or need regular income, the Endowus Core portfolios such as the Flagship and ESG sustainable portfolios would be suitable, as both of these portfolios prioritise growth and wealth-building for the long term.

Beyond Retirement — A Tool For Our Legacy

A good thing about Endowus Income portfolios is that beyond their primary objective of helping us fund our retirement through passive income, they can also serve as a legacy tool. Since the Endowus Income portfolios focus on capital preservation with limited or some growth (depending on the portfolio you choose), this means that even after we are no longer around, they can still act as an income stream for our loved ones!

As with all Endowus portfolios, there are no sales charges or transaction fees, and 100% of trailer fees are returned to investors. The only thing that Endowus charges is a simple, transparent, all-in-one Access Fee that ranges from 0.25% to 0.60%p.a., depending on the investment amount held under management.

Disclaimer: Investment involves risk. Past performance is not necessarily a guide to future performance or returns. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested. Rates of exchange may cause the value of investments to go up or down. Individual stock performance does not represent the return of a fund.

Any forward-looking statements, prediction, projection or forecast on the economy, stock market, bond market or economic trends of the markets contained in this material are subject to market influences and contingent upon matters outside the control of Endow.us Pte. Ltd (“Endowus”) and therefore may not be realised in the future. Further, any opinion or estimate is made on a general basis and subject to change without notice. In presenting the information above, none of Endowus Pte. Ltd., its affiliates, directors, employees, representatives or agents have given any consideration to, nor have made any investigation of the objective, financial situation or particular need of any user, reader, any specific person or group of persons. Therefore, no representation is made as to the completeness and adequacy of the information to make an informed decision. You should carefully consider (i) whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances. You may also wish to seek financial advice through a financial advisor or the Endowus platform and independent legal, accounting, regulatory or tax advice, as appropriate.

Investment into collective investment schemes: Please refer to respective funds’ prospectuses for details of the funds, their related fees, charges and risk factors, The listing of units of the fund on a stock exchange does not guarantee a liquid market for the units. Before making an investment decision, you are reminded to refer to the relevant prospectus for specific risk considerations.

This article was first published in 2022 and we have updated it with the latest rates

This article contains affiliate links. DollarsAndSense may receive a share of the revenue from your sign-ups. You can refer to our editorial policy here.