This article was written in collaboration with Capital Group. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, are purely for informational purposes, and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions, and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

Markets have not made investing easy lately. One week, we are watching inflation data to gauge whether interest rates will stay higher for longer. The next, markets are reacting to tariff headlines, recession fears or geopolitical developments that shift sentiment almost overnight.

For many of us, this constant uncertainty can make investing emotionally draining. Our challenge today is no longer just about finding the next high-growth opportunity. It is also about building a portfolio resilient enough for us to stay committed, even when markets turn volatile.

This is why balanced portfolios are attracting renewed attention. Instead of relying heavily on equities for returns, balanced portfolios combine growth assets, such as stocks, with defensive assets, such as bonds. The aim is to create a smoother investment experience that still allows us to participate in long-term market growth, while reducing some of the sharp swings that make staying invested difficult.

What Exactly Is A Balanced Portfolio?

At its core, a balanced portfolio combines equities and fixed income within a single investment strategy.

Equities give us exposure to long-term corporate earnings growth and allow us to participate in broader economic expansion. Over time, stocks have historically been one of the strongest drivers of portfolio growth. However, they also come with higher volatility and sharper short-term declines.

Bonds play a different role. They can provide income, offer diversification and help cushion portfolio declines during periods of market stress. While bonds may not offer the same long-term growth potential as equities, they can add potential stability when markets become unsettled.

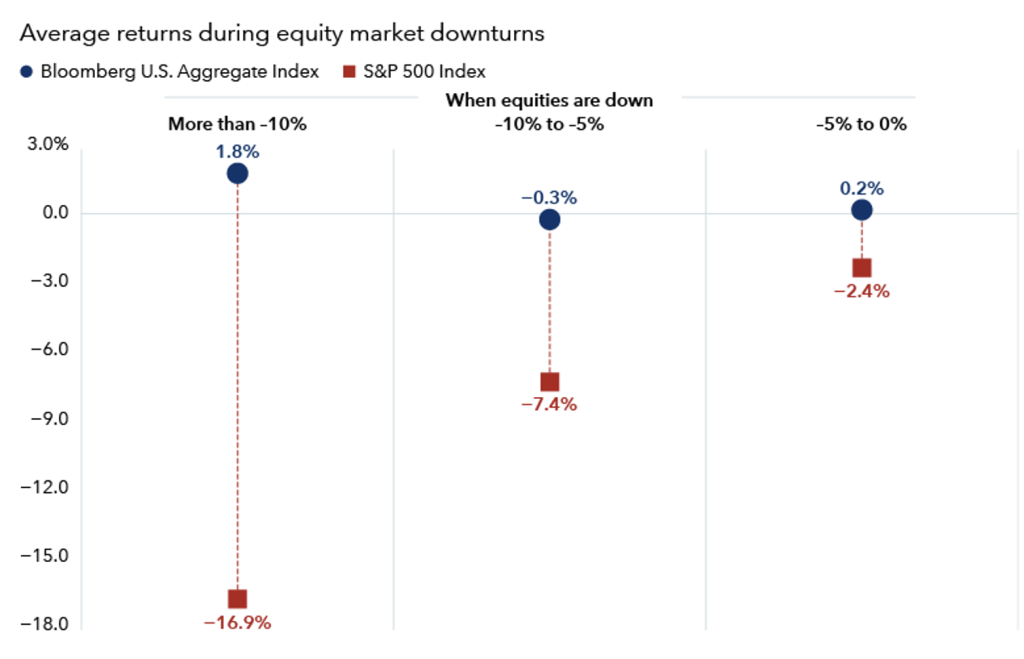

Bonds have offered diversification during equity selloffs

Past results are not a guarantee of future results

Sources: Capital Group, Bloomberg. Figures reflect monthly data using rolling three-month total returns between February 2006 and February 2026. Total number of decline periods is 63, or 26%, of all monthly periods in the sample. As of 28 February 2026.

A classic example is the traditional 60/40 portfolio, where 60% is allocated to equities and 40% to bonds. This approach has long been used as a practical way to balance growth and stability.

The objective is not to eliminate risk entirely. Balanced portfolios can still suffer losses during broad market sell-offs. Instead, the goal is to reduce portfolio volatility while maintaining exposure to long-term growth opportunities.

This matters because even well-designed investment strategies can fail if we abandon them during difficult periods. A balanced portfolio can help make downturns more manageable, increasing the likelihood that we stay invested through market cycles. This is often one of the biggest contributors to long-term investment success.

Why Balanced Portfolios Are Relevant Again

For much of the past decade, balanced portfolios lost some of their appeal.

When interest rates were near historic lows, bond yields offered limited income. Many investors questioned whether fixed income still deserved a meaningful place in portfolios, especially as equities, particularly large US technology stocks, delivered strong returns.

Today, the investing environment looks very different.

Higher interest rates have pushed bond yields higher, making fixed income potentially more attractive again as a source of income and diversification. At the same time, market volatility has reminded us that equity-heavy portfolios can produce large swings that are difficult to sit through.

According to Capital Group research, traditional balanced strategies such as 60/40 portfolios have historically shown resilience across rolling five-year periods spanning different market environments, from economic expansions to recessions and inflationary cycles.

Why Diversification Alone Is Not Enough

Diversification is often described as the foundation of sound investing. But simply owning a mix of stocks and bonds does not automatically create a resilient portfolio. The quality of the underlying assets matters too.

On the equity side, many balanced strategies focus on companies with durable business models, strong balance sheets, healthy cash flows and consistent profitability. These qualities can help businesses navigate slower growth, inflationary pressure or broader market weakness more effectively.

On the fixed income side, investors are increasingly looking towards higher-quality investment-grade bonds that may offer greater stability during uncertain conditions.

For long-term investors, combining income generation with quality-focused diversification can help create a steadier investment experience that may be easier to stick with when volatility rises.

Why Active Management Matters More Than We Think In Uneven Markets

Over the past decade, passive investing benefited significantly from a narrow group of mega-cap technology stocks that drove much of the overall market performance. In that environment, simply tracking an index often delivered strong results.

Today’s backdrop is more complex.

Persistent inflation pressures, elevated interest rates and ongoing geopolitical uncertainty have created a market environment where performance leadership may become broader and less predictable.

This is where active management can potentially add value.

Unlike passive strategies that mirror an index, active managers can adjust allocations in response to changing conditions. This could include shifting exposure across sectors, adjusting bond duration or identifying companies with stronger fundamentals.

Active management does not guarantee outperformance, and some actively managed strategies will underperform their benchmarks. However, in more uneven markets, experienced managers may have more opportunities to distinguish between stronger and weaker investment opportunities.

How Capital Group Applies This Balanced Approach

One example of this strategy is the Capital Group American Balanced Fund (LUX) (the “fund”), which is built on Capital Group’s broader American Balanced strategy with more than 50 years of investment history.

The fund is built around the idea of combining income, quality and resilience within a single portfolio.

Income can provide a steadier stream of returns, even when markets are uneven. Receiving income from a portfolio may make it easier to stay invested during more volatile periods.

Quality matters because not all companies and bonds are equal. In uncertain times, investors may prefer businesses with stronger balance sheets, more consistent earnings and durable business models.

Resilience means building a portfolio that may be better able to withstand periods of stress, recover more steadily and reduce the impact of extreme swings.

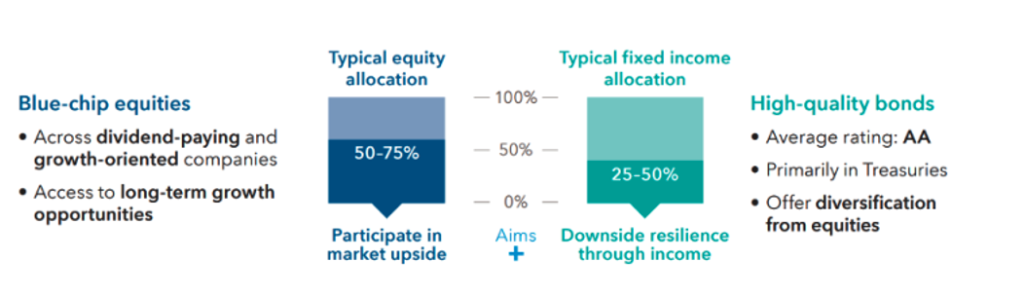

On the equity side, the strategy focuses on high-quality US companies, including dividend-paying businesses with durable fundamentals. On the fixed income side, it invests primarily in higher-quality bonds intended to provide income and diversification benefits.

The strategy also retains flexibility to adjust allocations between equities and bonds depending on market conditions, while operating within disciplined allocation parameters.

You can read more about the fund in its product brochure.

Balanced Portfolios Still Come With Risks

To be clear, balanced portfolios should not be mistaken for risk-free investments. We should still expect periods of volatility and temporary losses, especially during broad market downturns when both equities and bonds may come under pressure.

For Singapore-based investors, there are also additional considerations, such as currency fluctuations, interest-rate sensitivity affecting bond prices, and the possibility that active managers may underperform their benchmarks. Diversification helps manage risk, but it cannot eliminate it entirely.

The Goal Is Not To Avoid Volatility, But To Stay Invested Through It

Market uncertainty is unlikely to disappear anytime soon.

For most of us, the goal should not be to avoid volatility altogether or to perfectly time every market move. Instead, it is to build a portfolio that can navigate different market environments while still pursuing long-term growth.

Balanced portfolios may not always deliver the strongest returns during powerful bull markets. But for investors who value a combination of growth, income and resilience, they can offer a more sustainable way to stay invested over time.

And in investing, staying invested consistently often matters far more than trying to predict what markets will do next.

Read Also: Why A Balanced Portfolio Matters More Today In A Volatile World

Photo Credit: iStock/Andrii Yalanskyi

Glossary

Active vs. passive: ‘Active funds’ are managed by managers who attempt to surpass an index over time, while ‘passive funds’ track an index.

Blue chip: Common stock of a nationally known company that has a long record of profit growth and dividend payment and a reputation for quality management, products and services.

Downside protection / resilience: An investment position that seeks to reduce the frequency and/or magnitude of capital losses resulting from the decline of a stock or a fall in the overall market.

Duration: A measure of the approximate sensitivity of a bond portfolio’s value to interest rate changes.

Fundamental analysis / research: A method of evaluating a security in an attempt to measure its intrinsic value, by examining related economic, financial and other qualitative and quantitative factors.

Investment grade bond: Assets rated BBB- or higher by rating agencies Moody’s, Standard & Poor’s or Fitch.

Upside: Refers to the potential for an investment to increase in value, as measured in terms of money or percentage.

Yield: The income returned on an investment, such as the interest or dividends received from holding an asset. The yield is usually expressed as an annual percentage rate based on the investment’s current market cost.

Disclaimer

Risk factors you should consider before investing:

- This material is not intended to provide investment advice or be considered a personal recommendation.

- The value of investments and income from them can go down as well as up and you may lose some or all of your initial investment.

- Past results are not a guarantee of future results.

- If the currency in which you invest strengthens against the currency in which the underlying investments of the fund are made, the value of your investment will decrease. Currency hedging seeks to limit this, but there is no guarantee that hedging will be totally successful.

- Some portfolios may invest in financial derivative instruments for investment purposes, hedging and/or efficient portfolio management.

- The Prospectus – together with locally required offering documentation – sets out risks which, depending on the fund, may include risks associated with investing in fixed income, derivatives, emerging markets and/or high-yield securities; emerging markets are volatile and may suffer from liquidity problems.

This communication is intended for the internal and confidential use of the recipient and not for onward transmission to any other third party.

In Singapore, this communication has been prepared by Capital Group Investment Management Pte. Ltd. (CGIMPL), a member of Capital Group, a company incorporated in Singapore.

This advertisement or publication has not been reviewed by the Monetary Authority of Singapore or any other regulator.

This communication is of a general nature, and not intended to provide investment, tax or other advice, or to be a solicitation to buy or sell any securities. All information is as at the date indicated and attributed to Capital Group unless otherwise stated. While Capital Group uses reasonable efforts to obtain information from third-party sources that it believes to be accurate, this cannot be guaranteed.

The fund(s) is (are) offered only by Prospectus, together with any locally required offering documentation.

In Singapore, this is the Product Highlights Sheet (PHS).

These documents are available free of charge and in English and local languages at capitalgroup.com, and should be read carefully before investing.

The material is not intended to be distributed or used by persons in jurisdictions that prohibit its distribution. If you act as representative of a client it is your responsibility to ensure that the offering or sale of fund shares complies with relevant local laws and regulations.

The information in relation to the index is provided for context and illustration only. The fund is actively managed. It is not managed in reference to a benchmark.

For Singapore: CGIMPL is the appointed Singapore Representative of the Fund.

The list of countries where the fund is registered for distribution can be obtained online at www.capitalgroup.com

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company. All other company names mentioned are the property of their respective companies.

© 2026 Capital Group. All rights reserved.