This article is written in collaboration with OCBC. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, and is purely for informational purposes and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions and readers are encouraged to do their own due diligence. You can view our full editorial policy.

Like many children growing up, I learnt about money through weekly allowances, birthday gifts and the red packets I received during festive occasions. Most of these lessons centred around one idea: save your money.

As a child, I was taught that being financially responsible meant being a good saver. If I received money, I should spend as little of it as possible and put the rest aside for the future.

As a parent today, I still think saving is an important habit. However, I have also realised that it is not the only money habit our children need to develop.

It Is Harder To Learn About Money When Money Is Invisible

One reason many parents developed an intuitive understanding of money is that we physically handled it when we were younger.

If we spent $10 at McDonald’s, we could see $10 leaving our wallet. When we took a taxi ride, we watched the meter running and knew exactly how much the journey was costing us. Spending felt real because we could literally see money changing hands.

Today, that is no longer the case.

Whether we are paying for a Grab ride, buying movie tickets or shopping online, a simple tap or click is often all it takes to complete a transaction. Our children may watch us make purchases throughout the day without fully appreciating how much money has just been spent.

This is not a criticism of cashless payments. Digital payments are faster, more convenient and have become a normal part of everyday life. However, it means that many of the financial lessons previous generations naturally learned may now need to be taught more intentionally.

Last year, I brought my daughter to OCBC Wisma Atria to open an OCBC My Own Account for her.

While I could have done it online, I wanted her to experience for herself what going to a bank is like. I also wanted her to physically deposit her cash and coin savings through the ATM, so that she could see that money can also be kept safely in the bank, rather than to be hidden at home. The aim was to give her early exposure to how tools offered by banks, such as a savings account and a debit card, can help her develop her money habits as she grows up.

The Four Money Habits Every Child Should Learn

In my view, there are four money habits children should learn today. They should learn how to save diligently, spend responsibly, share generously and grow their money wisely.

Habit #1: Learning To Save Diligently

Saving is often the first financial lesson children learn.

Having a savings account allows children to see their money accumulate over time. Instead of keeping money in a piggy bank, they can track how much they have in their account, and understand that setting money aside today creates options for tomorrow.

Parents can make this lesson more tangible by helping children set savings goals.

For example, when my daughter started asking for a Nintendo Switch 2, it became a useful opportunity to talk about saving towards something she really wanted, rather than simply expecting us to buy it for her.

We could break down the cost with her, decide how much of her allowance or ang bao money she wanted to set aside, and let her track her progress over time. As children move closer to their targets, they will begin to understand the relationship between patience and rewards.

Habit #2: Learning To Spend Responsibly

Saving is important, but being financially responsible is not simply about putting money aside. Our children also need opportunities to make conscious decisions about how they spend.

This can be challenging in a cashless environment because spending is less visible than before. A digital payment only takes seconds, making it easy to overlook the fact that money has actually left an account. Sometimes, our children don’t even know how we may have spent when we bring them to a café.

With an OCBC MyOwn debit card or through the OCBC App, children can experience how cashless payments work while learning an important lesson: digital payments are still real spending decisions.

More importantly, every spending decision involves a trade-off.

For example, both my daughters are currently in primary school and receive a weekly allowance. This gives them the autonomy to manage their own money, deciding how much to spend during the week and how much to save. If they want to save towards something, they have to think twice before buying an extra snack or drink.

The lesson is not that they should never spend, but rather, it is that spending should be intentional. Over time, they learn that every dollar spent today is a dollar that cannot be used elsewhere, and that small daily choices can affect what they are able to do later.

Habit #3: Learning To Share

Children may think money is meant only for saving and spending, but that is not the full story. Money can also be used to care for others.

When my second daughter started school this year, we realised that she enjoys using part of her weekly allowance to buy things for her younger sister. Nobody specifically asked her to do it. It was simply a decision she made on her own.

To her, being able to buy something for her younger sister is a sign that she is growing up and making her own choices. These experiences help children understand that money is not only about personal consumption but can also be used to care for the people they love, and the causes that matter to them.

Habit #4: Learning How Money Can Grow

Another important lesson we should teach our children is that money does not always remain static.

One simple way to explain this is to compare money to a seed. A seed may look small and ordinary at the start. But when it is planted, watered and given time to grow, it can eventually produce something much larger.

Money can work in a similar way. A child who receives a sum of money from birthdays and festive occasions may not think much about what happens after the money is deposited into a savings account. Over time, however, they can begin to see that money can earn interest and gradually grow.

As children get older, this can become a natural bridge towards understanding investing and the power of compound interest. Of course, growing money takes time. But that is precisely the lesson. It teaches children patience, long-term thinking and the value of giving something enough time to develop instead of always seeking instant gratification.

Helping Children Make Intentional Money Decisions

Imagine a child receives $300 as a reward for doing well in school.

They could spend all of it immediately, save all of it, share some of it with others, or set aside a portion to grow over time.

In my opinion, the goal is not necessarily to convince our children that saving every dollar is always the best financial decision. Rather, it is to help them understand the implications of each choice and encourage them to make intentional decisions instead of impulsive ones.

The earlier children learn these lessons, the more prepared they may be when they eventually start managing larger amounts of money through internship salaries, part-time jobs or NS allowances.

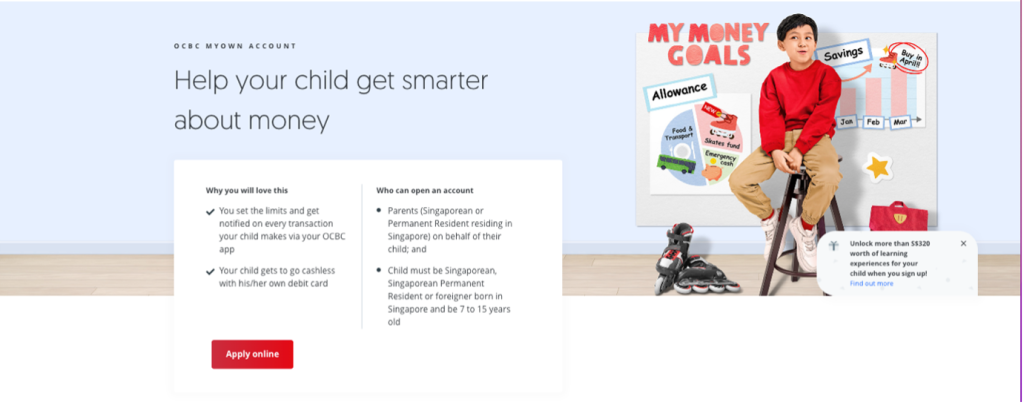

OCBC MyOwn Account: A Practical Way To Build Healthy Money Habits

This is where having a dedicated children’s account such as the OCBC MyOwn Account can be useful. Rather than simply telling children to save, parents can use the account as a practical tool to help them build healthy money habits from a young age.

By having an account under their own name, children can develop a greater sense of ownership over the money they receive, spend and save. Over time, this helps them better understand how their everyday choices affect their bank balance, and encourages them to think more carefully about each money decision.

The account comes with built-in guardrails to assure parents. Parents can set daily spending and withdrawal limits and receive real-time notifications so that they can monitor their children’s activity through their own OCBC app while giving their children the autonomy to make financial decisions.

Allowing children to personalise their OCBC MyOwn Debit Card with a design of their choice can further strengthen this sense of ownership, making both the account and the card feel more personal to them.

Parents can also use the account to introduce goal-based saving. Whether a child hopes to buy a toy, game or gadget, setting a savings target allows them to experience first-hand the trade-offs that come with every financial decision.

Teaching Financial Literacy Beyond The Classroom

While saving, spending, sharing and growing money are important habits, there is another lesson that underpins all four: understanding how money is earned in the first place.

Financial literacy is not something children learn through a single conversation. It develops through experiences and opportunities to engage with money in meaningful ways.

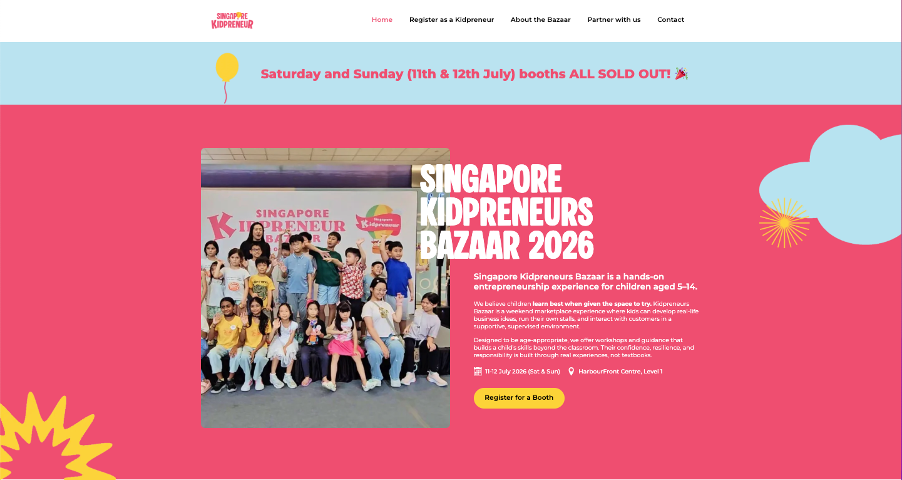

One such event that DollarsAndSense will be organising is the Singapore Kidpreneurs Bazaar 2026, taking place at HarbourFront Centre from 11 to 12 July.

At this event, children aged 5 to 14 will get to experience what it is like to start and run their own mini business, giving them a hands-on opportunity to appreciate how challenging it can be to earn money.

After all, few lessons are more meaningful than helping children understand the value of money by letting them experience the effort required to earn it.

OCBC will be joining us as the Official Banking Partner for the event, supporting our shared goal of helping children build stronger financial foundations from a young age.

Together with practical tools such as the OCBC MyOwn Account, we hope the experience will make financial literacy feel more real for children, not just something they hear about from adults, but something they can understand through their own decisions and experiences.

By giving them opportunities to save, spend, share and grow money, we can help them build habits that will serve them well throughout adulthood.

Read Also: I Opened A Child’s Savings Account For My Daughter. Here’s Why We Decided To Do It “In Person”

T&Cs apply. Insured up to S$100k by SDIC.