This article was written in collaboration with Prudential Singapore. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, are purely for informational purposes, and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions, and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

When Singaporeans think about financial protection, critical illness (CI) insurance is often one of the first products that comes to mind. While conditions such as cancer, stroke and heart attack can result in significant medical costs, many people underestimate the financial strain on individuals and their families. This is especially during “health gap years”, when one stops work to focus on recovery, but expenses continue.

Yet despite the importance of critical illness coverage, misconceptions remain surprisingly common. Some people assume CI insurance is meant to pay hospital bills. Others believe that since they have bought a policy years ago, they no longer have to worry about CI coverage.

Here are seven common misconceptions Singaporeans have about critical illness insurance.

Misconception #1: CI Insurance Is For Hospital Bills

One of the biggest misconceptions is that all ‘medical’ related insurance policies are the same. This isn’t true and it’s important to understand the differences between the two main types – hospitalisation and critical illness coverage.

Hospitalisation coverage is meant to pay for eligible hospital and surgery expenses, while critical illness coverage helps with income replacement during your “health gap years”.

In Singapore, we have MediShield Life, a national health insurance scheme for all Singapore Citizens and Permanent Residents, and Integrated Shield Plans by private health insurers that cover eligible hospitalisation and treatment costs. Depending on our coverage, these plans can significantly reduce the amount we pay out of pocket for hospitalisation and medical bills. Eligible expenses for inpatient/day surgery and outpatient benefits are paid directly to the hospital and any remaining out-of-pocket expenses will be borne by you.

Critical illness insurance serves a different purpose. It provides a lump-sum payout when we are diagnosed with a covered condition that meets the policy’s claim criteria. Such a payout goes directly to you and can be used to replace lost income or take care of other household expenses.

Misconception #2: If I Already Have An Integrated Shield Plan, I Don’t Need Critical Illness Coverage

Many Singaporeans already have hospitalisation coverage and assume they are adequately protected against major illnesses. However, even if treatment costs are largely covered by our MediShield Life and private Integrated Shield Plans, a critical illness can create other financial challenges.

For example, you may need to take an extended break from work or “health gap years” to recover from the illness. Additional support such as rehabilitation, transport expenses or caregiving assistance may also be required. It’s also possible that your medical expenses are not fully covered by your hospitalisation plan, leading to some out-of-pocket expenses.

Because critical illness payouts are typically paid as a lump sum, policyholders have the flexibility to use the money depending on where it is needed most.

Misconception #3: A Critical Illness Plan I Bought 10 Years Ago Should Offer The Same Protection As Today’s Plans

Insurance products evolve just like healthcare does. Over the past decade, critical illness plans have evolved in response to changing customer needs, medical advancements and claims experience.

A critical illness policy bought 10 years ago would have been designed and priced based on prevailing medical knowledge, treatment, and claims experience available at the time of policy design. Since then, advances in medical screening, diagnosis and treatment mean that some serious illnesses may be detected and managed differently today.

Newer CI plans may therefore include additional early critical illness benefits or additional covered conditions, with these enhancements reflected in how the plan is priced. This is why older and newer plans should not be compared as if they were designed on the same basis. Similarly, if these newer treatments or new conditions are extended retrospectively to older policies, this could increase claim costs and affect premiums for that earlier group of policyholders.

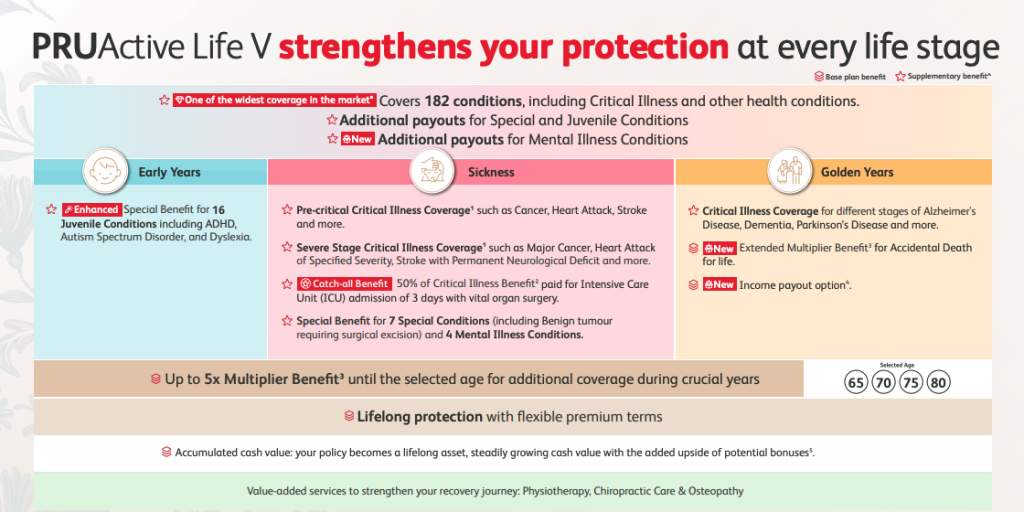

For example, PRUActive Life V provides coverage across 182 conditions, including early to severe-stage critical illness, special, juvenile and mental illness conditions through the critical illness add-ons.

Source: Prudential Singapore

Compared with many older CI plans, newer plans such as this one, may offer broader coverage, including coverage for additional early critical illnesses and additional health conditions.

Misconception #4: Claims Are Assessed Based On The Latest Medical Practices, Not Policy Wording

Many consumers naturally assume that once a doctor confirms a diagnosis, the claim outcome should automatically follow. However, this is not always the case.

Critical illness claims are assessed based on the policy definitions and conditions stated in the insurance contract. This means that the wording of a policy matters, including how each condition is defined and what claim requirements must be met.

Medical practices may evolve over time, but insurers still have to assess claims against the terms of the policy that was purchased. This is why consumers should review their policy documents and speak with their financial representatives to understand what their plan covers and whether it is sufficient for their needs.

Misconception #5: I Already Bought Critical Illness Coverage So I Am Sufficiently Covered

Having critical illness coverage is a good start. The more important question, however, is whether the amount of coverage remains relevant today. Are there newer conditions that you would like to be covered for?

A policy purchased in your twenties may have been adequate when your financial responsibilities were relatively modest as a young working adult with no dependants. Fast forward 10 or 15 years, and you may have a mortgage, young children, ageing parents and a significantly higher standard of living to support. At the same time, inflation means that the same payout amount may not stretch as far as it once did. The lump-sum payout from a critical illness plan is useful in supporting your health break as you recover.

Protection planning is therefore not a one-time exercise. Periodic reviews can help ensure that coverage continues to reflect changing life stages and financial obligations.

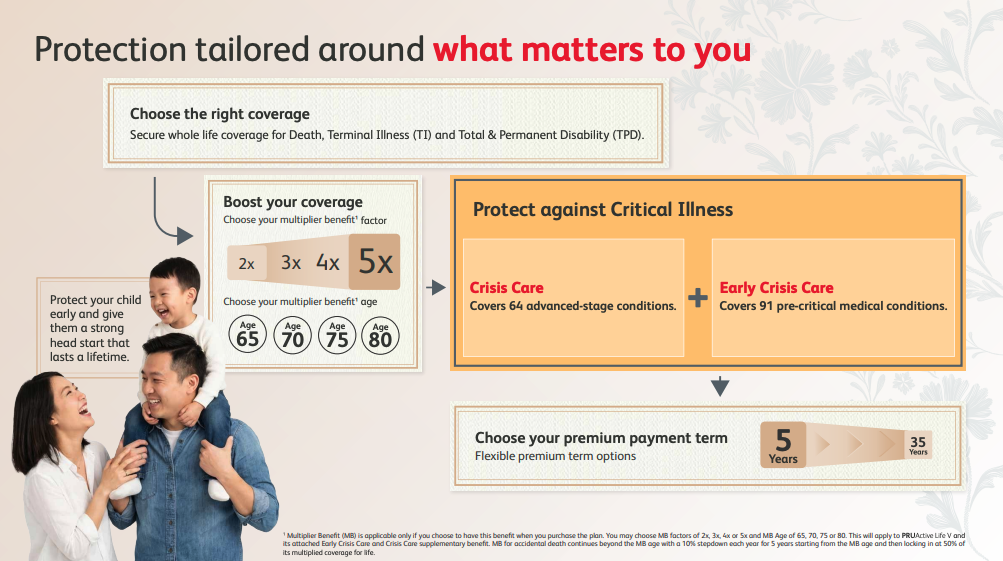

An insurance policy such as PRUActive Life V allows you to boost your coverage during key life stages through multiplier options that provide enhanced coverage during peak earning years, when financial responsibilities may be greatest.

Source: Prudential Singapore

Misconception #6: Critical Illness Payouts Are Mainly Used For Medical Bills

While medical expenses often receive the most attention, they may not always be the largest financial challenge following a critical illness.

For many families, the more significant concern is the loss of income. A working adult diagnosed with a serious illness may need months or even years before returning to full employment. During this period, mortgage payments, household expenses, children’s education costs and other financial commitments do not simply disappear.

For some, the financial impact of a critical illness extends well beyond treatment costs. Even after leaving the hospital, there may be months or years of reduced income while regular expenses continue.

Having access to a lump-sum payout can provide greater financial flexibility during this challenging period.

Misconception #7: All Critical Illness Plans Are The Same

At first glance, many critical illness plans may appear similar, covering the common illnesses such as cancer, stroke and heart attack.

However, there can be significant differences beneath the different types of CI plans. Plans may vary in the number of conditions covered, the severity levels eligible for claims, the definitions used, the scope of benefits provided and how long protection lasts.

Some plans may focus primarily on severe-stage critical illnesses, while others may provide coverage for earlier-stage conditions or additional health events that could have a significant impact on quality of life and finances.

When comparing CI plans, it may be helpful to look beyond premiums and examine factors such as the range of covered conditions, whether early-stage conditions are included, and how benefits are structured.

As Your Life Changes, Your Protection Needs May Change Too

Critical illness insurance is ultimately about more than just receiving a payout after a diagnosis. It helps protect the life you’ve built during your “health gap years”, a period when your focus should be on recovery.

As healthcare advances and Singaporeans live longer after serious illnesses, it is increasingly important to consider whether existing protection remains aligned with your current budget, needs and expectations.

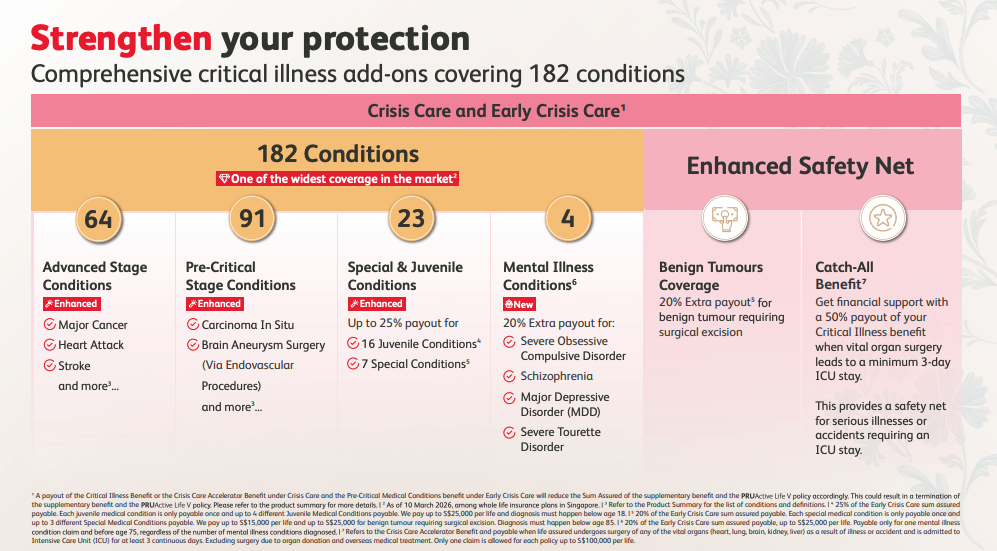

For those reviewing their coverage, solutions such as Prudential’s PRUActive Life V offer whole-life protection that can be enhanced with Crisis Care and Early Crisis Care riders. These optional benefits provide coverage across 182 conditions, including severe-stage critical illnesses, pre-critical conditions, selected mental illnesses and juvenile conditions.

Source: Prudential Singapore

More importantly, the plan is designed to help address the financial impact that can arise not just at the point of diagnosis, but throughout the years that follow.

Because when it comes to critical illness, recovery is often about much more than paying medical bills. It is also about having the financial confidence to focus on getting your life back on track.

Read Also: 5 Reasons Why Critical Illness (CI) Insurance Is Vital For Working Adults

Disclaimers:

- This article is for your information only and does not consider your specific investment objectives, financial situation or needs. We recommend that you seek advice from a Prudential Financial Representative before making a commitment to purchase a policy.

- This advertisement has not been reviewed by the Monetary Authority of Singapore.

- Information is correct as at 30 June 2026.

Photo Credit: iStock/Ivan-balvan