Singapore’s property market is showing signs of slowing down. The HDB resale price index has dropped quarter-on-quarter for the first time since 2019, while URA’s private residential price index rose moderately by 3.3% year-on-year, the smallest increase in a year since 2020. Potential homebuyers among us may be wondering whether this is the best time to buy property and whether we can afford it.

One way to determine affordability is based on the minimum salaries required to qualify for the housing loan amounts needed to finance our mortgage repayments. Based on the median prices of all types of resale property in Singapore in 2025, let’s look at how much you need to earn to buy your dream home.

| Housing Type | Median Resale Price | Minimum Downpayment | Monthly Repayments | Monthly Household Income |

| HDB 3-Room | $445,000 | $111,250 | $1,600 | $5,872 |

| HDB 4-Room | $630,000 | $157,500 | $1,912 | $8,313 |

| HDB 5-Room | $736,000 | $184,000 | $2,234 | $9,712 |

| HDB Executive | $900,000 | $225,000 | $2,731 | $11,876 |

| Executive Condominium | $1,518,000 | $379,500 | $4,607 | $9,882 |

| Condominium (OCR) | $1,650,000 | $412,500 | $5,007 | $10,742 |

| Condominium (RCR) | $2,012,000 | $503,000 | $6,106 | $13,099 |

| Condominium (CCR) | $2,370,000 | $592,500 | $7,193 | $15,429 |

| Terrace House | $3,300,000 | $825,000 | $10,015 | $21,484 |

| Semi-Detached House | $4,090,000 | $1,022,500 | $12,413 | $26,627 |

| Bungalow | $4,125,000 | $1,031,250 | $12,519 | $26,855 |

| Good Class Bungalow (GCB) | $30,750,000 | $7,687,500 | $93,323 | $200,189 |

(Calculations were done using the Reverse Affordability Calculator and Mortgage Calculator provided by Mortgage Master. HDB flat resale transaction data obtained from HDB, private property resale transaction data obtained from URA. For data purposes, GCB is defined as having a minimum land area of 1,400 square metres, and located in Districts 10, 11, 20, 21, and 23)

The data assumes:

- No housing grants are used to buy HDB flats

- A minimum downpayment of 25% for all property purchases, regardless of the loan eligibility and financial capacity of the borrowers. In other words, we assume the borrower qualifies for a 75% Loan-To-Value (LTV).

- Homebuyer has no other loans or financial commitments into consideration. This may unnaturally inflate the Mortgage Servicing Ratio (MSR) or Total Debt Servicing Ratio (TDSR). The 30% MSR rate is used to determine the salary required for HDB flats. The TDSR rate of 55% is used to determine the salary required for ECs (where the minimum occupation period has been fulfilled) and private properties.

- A 25-year home loan tenure with a fixed interest rate of 1.6% to determine the monthly repayments.

- Prices exclude all other additional payments, including agent fees, buyer’s stamp duty (BSD), legal fees, renovation or other related expenses that are typically incurred during a property purchase.

How Much You Need To Earn To Buy An HDB Flat

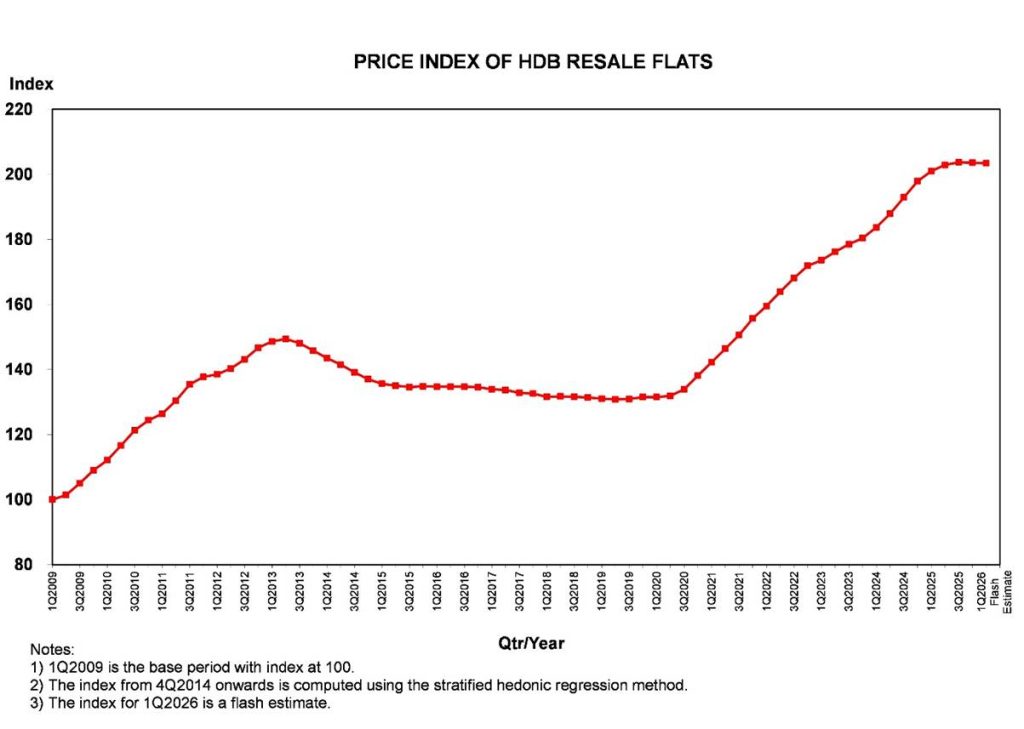

The HBD Resale Price Index climbed to a new high of 203.7 in 2025. However, at the tail end of the year, prices dropped for the first time since 2019, with flash estimates currently putting the Resale Price Index at 203.4 in Q12026.

Source: HBD Resale Price Index

For those buying HDB flats, the median household salary you need to finance your home loan repayments (not taking any housing grants into consideration) ranges between $5,872 and $11,876, depending on the size of the flat.

Read Also: HDB Price Guide: Cheapest And Most Expensive Estates In 2025

How Much You Need To Earn To Buy An Executive Condominium (EC)

Discussions in Parliament over the affordability of Executive Condominiums (ECs) have led Mr Chee Hong Tat, Minister for National Development to announce that the EC policy would be reviewed. Median prices of ECs were $1,754 per square foot in 2025. It was $1,537 per square foot in 2024.

To afford a median EC resale unit based on 2025 prices, buyers would need a combined monthly household income of at least $9,982.

Note that there’s a key difference between buying ECs first-hand from the developers, which will subject you to the MSR (30%) limit. This will increase the income required to afford an EC. On the other hand, for resale ECs that have completed their 5-year minimum occupation period (MOP), buyers would be subjected to the TDSR (55%) limit. This allows them to use a larger portion of their income to finance the mortgage payments.

Read Also: Complete First-Timers’ Guide To Buying A New Executive Condominium (EC) In Singapore

How Much You Need To Earn To Buy A Private Condominium

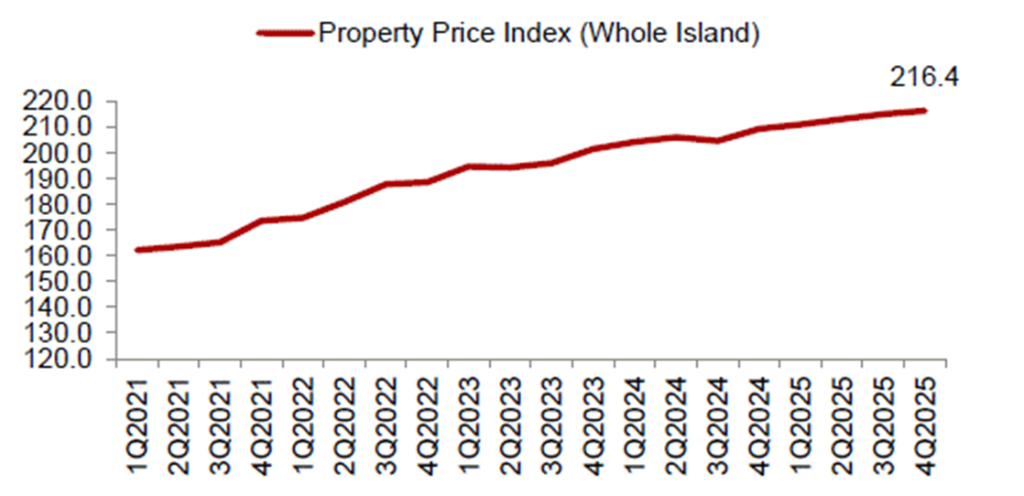

There was also slowed growth in the private (non-landed) residential property market over the past year. The URA Private Property Index hit a new high of 216.4 in 4Q2025.

Source: URA Private Property Price Index

The private condominium market is segmented based on three regions: the Core Central Region (CCR), the Rest of Central Region (RCR), and the Outside Central Region (OCR).

Aside from the minimum salary required to finance a private property, it’s worth noting the downpayment of between $487,500 and $712,500 that buyers have to put down either in cash or CPF. This can be as much as 7 times the minimum downpayment required for HDB flats.

Read Also: CCR, RCR, OCR: What Do These District Classifications Mean When Looking For Your Property Purchase

How Much You Need To Earn To Buy A Landed Property

Landed properties, which consist of less than 5% of Singapore’s total residential housing stock, are classified as terrace units, semi-detached units, and detached units (also referred to as bungalows).

To finance the mortgage payments for a landed property, a household income of between $21,484 and $26,855 is needed.

In reality, buyers would need to earn more than this to cover the higher maintenance and running costs of landed properties. Furthermore, with minimum downpayments of $825,000 to $1,031,250, buyers would need sizeable cash savings to afford these properties.

Read Also: Complete Guide To Buying Landed Property In Singapore

How Much You Need To Earn To Buy A Good Class Bungalow (GCB)

The median price for the crown jewel of residential properties in Singapore, i.e., the coveted Good Class Bungalow (GCB), was derived from URA transaction records for landed properties larger than 1,400 sq m (about 15,000 sq ft).

There was a total of 21 transactions that met this requirement in 2025, with the lowest transaction recorded at around $30 million in the Caldecott Hill Estate. In contrast, the highest transaction was recorded at the end of the year, a Peirce Road GCB that is reportedly sold at $148 million. That was a whole $90 million more than the next highest transaction, also in the Caldecott Hill Estate, at $58 million.

Read Also: 4 Reasons Why A Good Class Bungalow (Assuming You Can Afford It) Is A Great Investment

You Are Buying A Home, Not Investing Your Life Savings

With rising property prices, we may think that affordability is worsening, which might prevent us from taking action to purchase our dream home. Determining the minimum salary required to own each home type is based on multiple assumptions, but it still serve as a useful reference for the minimum salary needed to finance mortgage payments.

That’s why it’s best to consult a mortgage broker for such decisions. Mortgage brokers in Singapore offer their time and advice to help you make the decision that is right for your individual needs. Since they are often paid the same commission rates by the banks they refer you to, they offer their services to you for free. Consider our friends over at RedBrick and Cashew.

If you prefer a DIY approach, Cashew offers a user-friendly platform to compare packages across banks based on your loan inputs. Additionally, Cashew’s advisors also assist you in applying for the preferred loan package, all from the comfort of your home.

Alternatively, RedBrick offers a more personalised experience, with its professional mortgage brokers sharing insights into the nuances of each loan package during a free, non-obligatory consultation. Check out our home loan guide for more information.

Ultimately, the best choice is to work with a mortgage broker who has years of industry experience. As we’ve mentioned consistently in this article, mortgage rates are cyclical, and only the most experienced brokers are aware of the nuances and can provide advice on choosing a fixed or floating rate that not only benefits you in the short term but also in the long term.

Read Also: HDB Loan or Bank Loan? Choosing The Right Mortgage Plan