For platform workers delivering food or driving passengers, CPF contributions can make a meaningful difference to their long-term savings. Unlike traditional employees, platform workers have historically not received employer CPF contributions. That changed from 1 January 2025.

Under the Platform Workers Act, platform operators such as Grab and Foodpanda are now required to make CPF contributions for their platform workers. For those born in 1995 or later, these contributions are mandatory. For workers born before 1995, CPF contributions apply only if they choose to opt in and contribute to all three CPF accounts.

As of September 2025, about 26,500 platform workers, or 27 per cent of eligible workers, had opted in, according to the Ministry of Manpower. In other words, nearly three in four eligible older platform workers have not opted in, even though doing so would allow them to receive additional CPF contributions from platform operators on top of their cash earnings.

How Much Would Platform Operators Need To Contribute To Workers’ CPF Accounts?

Let us start with a simple scenario.

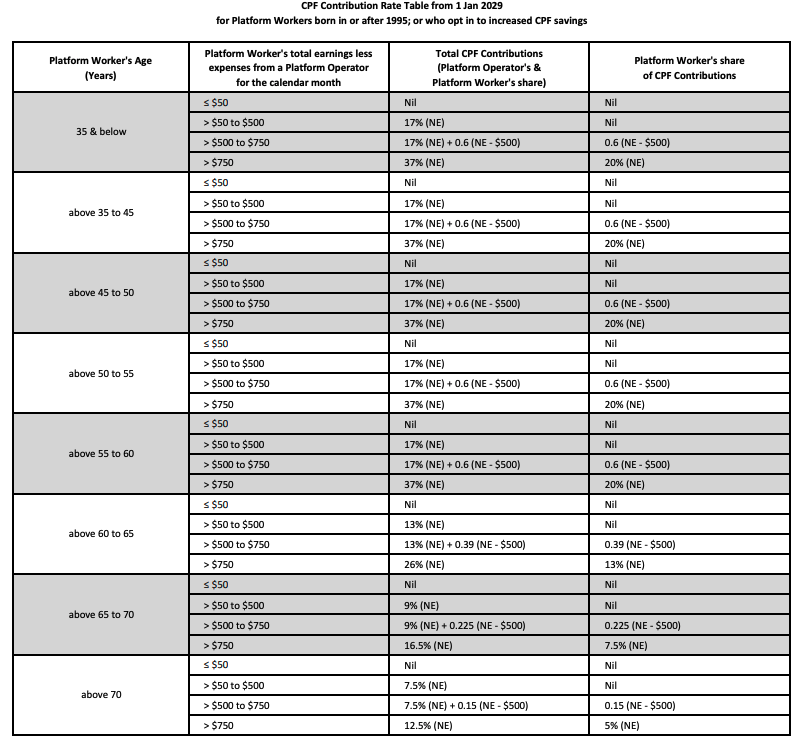

Assume a 40-year-old platform worker earns $2,500 a month in net earnings, after accounting for vehicle rental, petrol and other operating expenses. If he does not opt in to CPF contributions, he still needs to make mandatory Medisave contributions as a self-employed person. At age 40, the Medisave contribution rate is 9 per cent of net earnings. That works out to $225 a month.

This means his effective take-home income is $2,275. He receives no CPF contribution from the platform operator.

Now consider what happens if the same worker opts in to contribute to all three CPF accounts.

In 2026, his own CPF contribution rate would be 14 per cent of net earnings, or $350. On top of that, the platform operator would need to contribute 7 per cent, or $175.

This means a total of $525 is contributed to his CPF accounts each month. More importantly, this $525 is allocated across his Ordinary Account, Special Account, and Medisave Account, rather than just to Medisave. While his cash take-home is slightly lower at $2,150, he now receives an additional $175 CPF contributions from the platform operator.

Contribution Rates Will Rise By 2029

The impact becomes even more significant over time.

By 2029, the contribution rates will increase to 20 per cent from the worker and 17 per cent from the platform operator, matching the full employee-employer CPF structure for younger workers.

Using the same $2,500 monthly net income assumption:

- Worker contributes 20 per cent: $500

- Platform contributes 17 per cent: $425

- Total CPF contribution: $925

This is a substantial sum. Over a year, that amounts to $11,100 in CPF savings.

Workers who choose not to opt in would effectively forgo the additional 17 per cent contribution from the platform operator. They would still need to contribute to Medisave as self-employed persons, but they would not receive any CPF contribution from their operator.

In simple terms, by contributing an additional 11 per cent beyond Medisave (to move from 9 per cent Medisave-only to 20 per cent full CPF by 2029), the worker unlocks an additional 17 per cent from the platform.

What Does This Mean For Platform Operators?

It should be clear by now that CPF contributions represent a high cost for platform operators. Any increase in labour-related costs directly affects profitability. In recent years, some operators have introduced new fee structures and partner fees, likely in response to rising regulatory and operating costs.

To understand the magnitude, let us look at a simplified example.

Assume a driver generates $10,000 in gross job value in a month. If the platform takes a 25 per cent commission, the breakdown may look like this:

| Revenue generated from jobs | $10,000 |

| Platform commission (25%) | (-$2,500) |

| Gross Earnings to platform workers | $7,500 |

| Expenses (Assuming 60% for driver based on FEDR) | (-$4,000) |

| Net Earnings | $3,000 |

| CPF Contribution From Worker (20% of $3,000) | $600 |

| CPF Contribution From Platform (17% of $3,000) | $510 |

The additional $510 that the platform must contribute is equivalent to about 20 per cent of its $2,500 commission revenue. If a worker opts in, that $510 belongs to him as CPF savings. If he does not opt in, the platform does not need to make that contribution and effectively retains that cost within its profit margin.

From a policy perspective, the intent is clear. Platform workers gain retirement and healthcare savings that more closely resemble traditional employment. From a business perspective, however, this is an additional cost.

Ultimately, the decision comes down to whether workers are willing to accept lower immediate cash flow in exchange for significantly higher long-term CPF accumulation. Those who opt in are effectively strengthening their retirement and healthcare savings through CPF contributions from the platform. Those who choose not to opt in retain slightly more cash today, but forgo the additional CPF contributions that platform operators would otherwise be required to make.

Read Also: How CPF Is Changing Long-Term Financial Planning For Platform Workers

Photo Credit: Moo Kar Ming, DollarsAndSense