When a recent article by The Straits Times highlighted a 71-year-old retiree receiving about $4,600 a month from her CPF, many Singaporeans understandably did a double-take. That is more than what some people earn while working full-time.

According to the article, she may “hold the current record for receiving the highest CPF monthly payout”.

One key detail that can easily be overlooked is that the retiree is currently on the old Retirement Sum Scheme. That means her monthly payouts come directly from her CPF Retirement Account savings, and they will eventually run out, likely around age 90. She is not on CPF LIFE, which provides payouts for as long as you live.

It brings us to the question. Can we get a similar or even higher amount, say $5,000 a month under CPF LIFE, and what are some practical steps that it would take for us to get there?

How CPF LIFE Works

Let’s first understand how CPF LIFE works.

CPF LIFE is essentially an annuity. At age 65 (it can be extended to 70), our Retirement Account savings are used to buy into the CPF LIFE scheme, which pays us a monthly income for life. The more we have in our Retirement Account at that point, the higher our monthly CPF LIFE payout will naturally be.

Unlike the old Retirement Sum Scheme, CPF LIFE pools longevity risk. In simple terms, it means CPF members will not need to worry about outliving their retirement savings. You receive your CPF LIFE payout for life.

Read Also: CPF LIFE VS Retirement Sum Scheme (RSS): What’s The Difference?

Under the current Enhanced Retirement Sum (ERS), CPF members who set aside $440,800 at age 55 in 2026 can expect to receive a monthly payout of about $3,440 from age 65 under CPF LIFE. This $440,800 is also the maximum amount that members aged 55 and above can top up their Retirement Account to in 2026.

At first glance, this figure appears to set a natural ceiling. And for most working Singaporeans, that may indeed be the practical upper limit to strive towards. Reaching the ERS, on its own, already requires years of steady contributions, disciplined top-ups, and leaving our CPF savings untouched to compound.

However, there are other ways to achieve a higher payout.

Deferred The Start Of CPF LIFE Payout Till 70

The first, and most obvious way, is to simply defer our payout till 70. According to the CPF Board, for each year that payout is deferred, your monthly payout can increase by 7%.

Do Regular Top Ups To Your RA To The ERS

At age 55, our Retirement Account (RA) is created. Our Special Account (SA) savings are automatically transferred into the RA. We can also choose to transfer some of our Ordinary Account (OA) savings to top it up to the ERS, which is $440,800 in 2026.

If we do this, it represents the maximum amount we can top up at that point. However, the ERS increases each year. This means we can continue making voluntary top-ups whenever the ERS is raised. For example, someone who turns 55 in 2026 will have an ERS of $440,800. When the ERS increases to $456,400 for the 2027 cohort, that same person can top up an additional $15,600. Importantly, the interest earned in our RA does not count towards the ERS cap. In other words, we can top up to the new ERS limit regardless of how much interest has already been credited.

While we do not know what the Full Retirement Sum (FRS), and therefore the ERS, will be when younger members turn 55, we can make a reasonable projection. For someone who is 55 in 2026 and will turn 65 in 2036, if we assume the FRS increases by 3.5 per cent each year, the FRS could reach about $311,013 by 2036. Since the ERS is set at twice the FRS, this would mean an ERS of approximately $622,026.

In practical terms, this means that from 2026 to 2036, a CPF member who had already set aside the 2026 ERS of $440,800 could potentially top up an additional $181,226 over time as the ERS rises. This will obviously increase the amount they have in their RA, and thus, their eventual CPF LIFE payout.

How Much Do You Need To Receive $5,000 A Month From CPF LIFE?

We use the CPF Monthly payout estimator to determine how much we need to receive, about $5,000 a month.

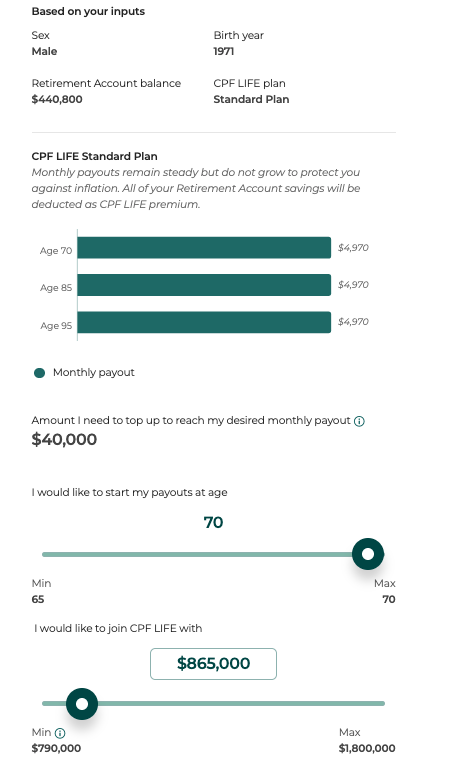

In the first scenario, let us assume a 55-year-old male sets aside the current ERS of $440,800. Based on the CPF LIFE Standard Plan, he would receive about $3,410 per month starting at age 65. The estimator also shows that by age 65, his Retirement Account would have grown to around $645,000 before he joins CPF LIFE. This growth comes from the 4 per cent interest earned over the 10 years.

Now, let us consider a second scenario. Instead of stopping at $440,800, the member continues topping up his Retirement Account each year as the ERS increases. As discussed earlier, this could amount to an additional $181,226 over 10 years, or about $18,126 a year.

Assuming a 4.0 per cent annual interest rate, these additional top-ups would grow to about $217,622 over the decade. If we add this to the projected $645,500 in the first scenario, the total Retirement Account balance at age 65 could reach approximately $863,122.

If he then defers starting his CPF LIFE payouts to age 70, the monthly payout increases further. Based on the estimator, joining CPF LIFE with about $860,000 (the calculator rounds the figure down) would generate a payout of roughly $4,940 a month. That is effectively at our $5,000 target.

Read Also: Here’s What Your CPF Full Retirement Sum Might Look Like When You’re 55

Ultimately, receiving $5,000 a month from CPF LIFE is not impossible, but it depends on several key assumptions. In our example, we assumed the ERS increases by 3.5 per cent per year, that we consistently top up our Retirement Account as the ceiling rises, and that we defer payouts to age 70 to boost our monthly income. This projection also applies specifically to the cohort turning 55 this year, starting from the 2026 ERS of $440,800.

Under these specific circumstances, achieving or getting close to $5,000 a month from our CPF LIFE is mathematically possible. But it requires steady top-ups, strong cash flow, and the discipline to delay withdrawals. For most of us, the takeaway is not just the headline figure, but understanding how CPF LIFE can work for our retirement and making our own decision about how much we wish to receive in payouts once we retire.

Photo Credit: Raymond Quek/DollarsAndSense