This article was written in collaboration with Endowus. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

When we think about retirement planning in Singapore, the topmost matters that come to mind usually revolve around how much we need to save, what we should invest in, and whether we should right-size our home to monetise it for our retirement.

While we presume CPF savings will make up a substantial portion of our retirement income, rarely do we actively think about how to further leverage it. Yet, knowing how to leverage our CPF savings is a very underrated financial decision that we can make to increase our retirement nest egg.

For example, while we may think we have enough savings to last us till age 90, it’s possible that many of us may even live beyond 90 and may aspire to live our golden years in comfort with our loved ones. Thus, investing (or not investing) our CPF savings could be the difference between a simple, no-frill retirement, or one that allows us to pursue our passions without having to worry about money.

Using Our CPF Ordinary Account (OA) For Our Home Down Payment & Monthly Mortgage

Very often, our CPF Ordinary Account (OA) is used mainly to fund our property purchase that includes both our down payment and monthly mortgage payments. However, this means that money meant for our future retirement is instead diverted away and channeled into our property purchase today. This may be a reason for why, according to the recently released CPF Annual Report, only 63.6% of Singaporeans aged 55 last year were able to meet the Full Retirement Sum.

Leaving Our CPF OA Monies Untouched

If not for housing we may leave funds untouched until age 55 when we can finally start withdrawing from our CPF account. The phrase, out of sight, out of mind, is an appropriate term to describe this behaviour. Since we can’t access the funds, we don’t put in any effort to manage the money.

Investing Our CPF OA Savings For Higher Returns

Leaving our CPF monies untouched isn’t without a little benefit. CPF savings in our OA earn a base interest rate of 2.5% p.a. while savings in our Special Account (SA) earn 4.0% p.a. But for those who wish to earn a higher return on their CPF savings, particularly funds in their OA, investing is one option to generate higher returns for retirement.

Endowus CPF Retirement Calculator – Helping Us To Forecast Our CPF Retirement Nest Egg

Even though we can’t withdraw funds from our CPF account like a regular savings account, knowing how much savings we will accumulate by the time we will reach 55 isn’t as easy as it seems.

This is because how much we have at age 55 is dependent not just on our monthly CPF contributions, but also on the CPF-related financial decisions we make today. For example, if we use a larger portion of our CPF OA funds for home purchases, then we will naturally have lesser savings for our retirement.

To help us calculate this, Endowus has introduced the Endowus CPF Calculator. With this tool, we can find out how CPF-related decisions we make today can significantly impact the amount of CPF savings we have for retirement.

Walkthrough of the Endowus CPF Calculator Webpage

The Endowus CPF calculator is free to use for anyone. Just go to the Endowus website and scroll down to the calculator. There are many tooltips to guide us with the inputs, and help us understand the right numbers to fill in.

Step 1: Fill in the basic personal information required, including our current salary, bonus, and CPF balances.

Step 2: Share our preferred retirement lifestyle decisions. For instance, our ideal retirement age, expected spending (based on today’s dollars) per month during retirement, and the amount we are willing to invest via CPF OA.

Step 3: Based on our input, Endowus will generate a personalised illustration of the projected income that we can get from CPF and the projected withdrawal balance from CPF Special Account and Ordinary Account. This shows an estimate of how much we will have at every age, and how much more we will have if we were to invest a portion of our investable CPF OA funds.

For example, at age 34 with $20,000 in OA and $20,000 in SA, a monthly salary of $5,000, and being open to investing 25% of CPF OA investable balance, we will have $554,929 that can be withdrawn from our CPF Special Account and Ordinary Account at age 55, after setting aside the FRS in our CPF Retirement account. This is about $88,723 more than what we will have if we choose not to invest at all, assuming we can achieve a return of 7.6% on our invested CPF funds.

If the amount we have above in our CPF seems higher than what most of us would expect, it’s due to the assumption that we did not use our CPF funds for home mortgage repayment – more on this later.

If the amount we have above in our CPF seems higher than what most of us would expect, it’s due to the assumption that we did not use our CPF funds for home mortgage repayment – more on this later.

Endowus also shows us the projected income that we can expect to withdraw from our CPF SA and OA each year, to fund any shortfall in our retirement allowance from CPF LIFE.

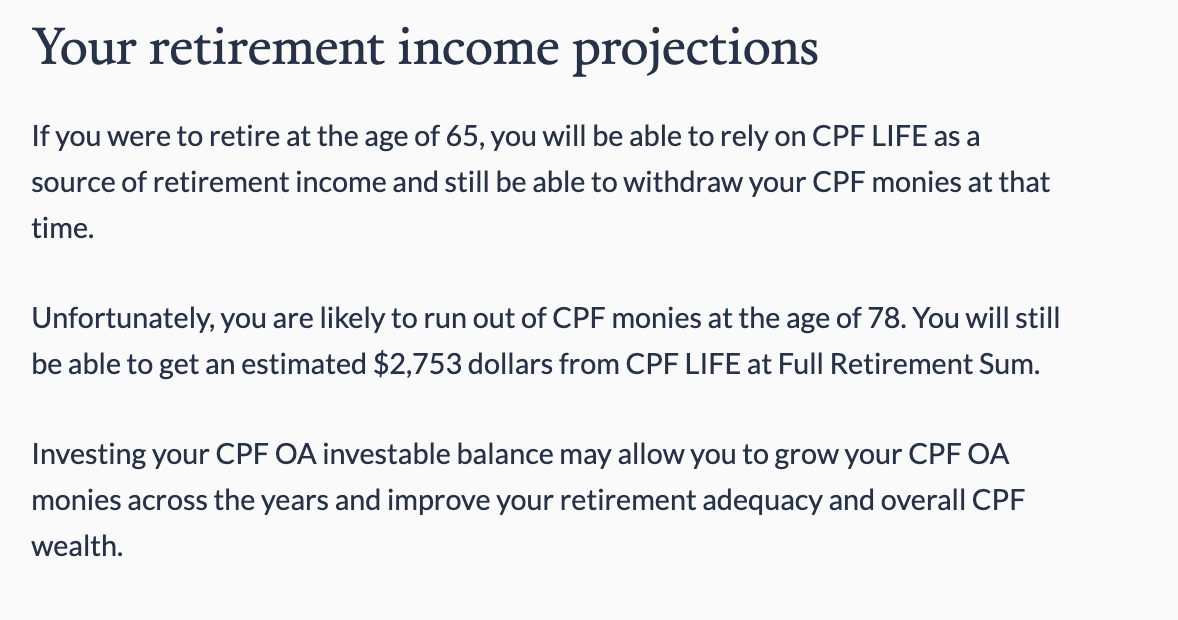

In our illustration above, we can see that there is a withdrawal from our CPF and thus the savings gradually fall over time. This withdrawal considers how much we want to spend each month (with inflation accounted for), and how much we are getting from CPF LIFE. More importantly, it predicts whether we are likely to outlive our CPF savings. Here’s another chart to depict this.

In the scenario above, we stated that we want to have a spendable income of $4,000 each month (in today’s dollar). Based on the CPF projections, we can see that we will not have sufficient CPF savings to enjoy our preferred monthly income once we turn 79 even with CPF LIFE payouts. However, by investing 25% of our investable OA savings, we may generate sufficient income from CPF to fund our ideal retirement payout until age 95.

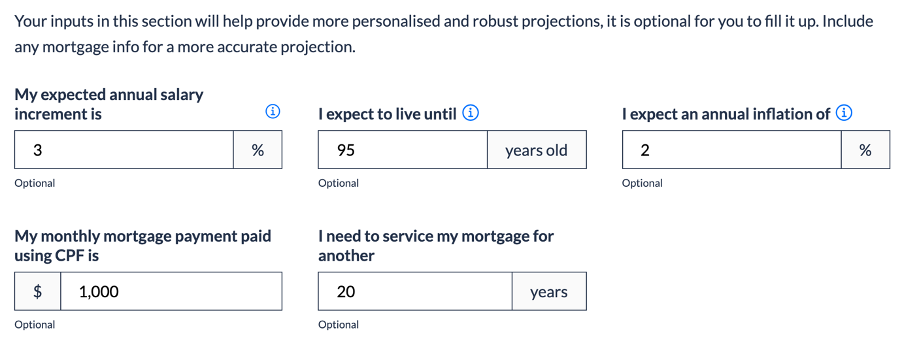

Step 4: Adjust the assumptions if needed. The above calculation is based on a few assumptions, including: an annual salary increment of 3%, an annual inflation rate of 2%, and a life expectancy of 95 years. You can adjust any input, and the calculation for the benefit illustration will change accordingly.

Impact of Mortgage on CPF Retirement Adequacy

We can also provide inputs to major decisions that may affect how much we have in our CPF account. For example, if we intend to service a mortgage using $1,000 from our CPF OA each month for the next 20 years, this will reduce how much we have in our CPF account.

Compared to our earlier illustration, we will now have $319,096 less in our CPF account (assuming we don’t invest any CPF monies) at age 55 since a large part of our OA funds has been diverted to service our home mortgage.

Compared to our earlier illustration, we will now have $319,096 less in our CPF account (assuming we don’t invest any CPF monies) at age 55 since a large part of our OA funds has been diverted to service our home mortgage.

In the illustration above, without investing our CPF, we are expected to deplete our CPF withdrawable balance for retirement income by age 71. However, if we were to 1) reduce the monthly mortgage that we pay using CPF from $1,000 to $500, and 2) concurrently, increase the proportion of our CPF OA funds to be invested from 0% to 50%, our savings is expected to last us till age 92. If we invest 75%, our CPF savings will be expected to outlive us.

In other words, by making our CPF OA work harder for us, we can extend the duration of our CPF withdrawals to finance our ideal retirement. Even though these financial planning tweaks can be done manually done by us, a sensitivity analysis of these is given to us by our customised report

Download Our Customised CPF Preparedness Report For Further Insights

Besides providing the inputs and getting the chart on the CPF calculator, we can also download an elaborated report with more details.

With this report, we can get additional insights based on our inputs provided. Here’s a recap of the inputs we have provided.

We can use these insights to reconsider our CPF decisions. For example, based on our initial inputs, we will have about $557,387 to withdraw from our CPF account at age 65 and are projected to run out of CPF withdrawable balance at 74.

However, if we were to invest 50% of our investable CPF OA balance, we will have about $918,284 instead. This is about $360,897 more as compared to not investing. Most importantly, it extends our CPF withdrawable balance such that it’s expected to run out only at age 92. This demonstrates how our CPF investment decisions can have a tangible impact on our retirement nest egg.

Understanding How Investing More Can Grow Our CPF Withdrawable Balances

Another interesting insight that Endowus provides is how much more we will have in our CPF account if we were to reduce the percentage of our mortgage that is paid through CPF. In our example, if we were to reduce the mortgage payment paid using CPF from $500 to $250, our retirement balance will increase by about $100,000 by age 65, assuming no investment is made. If we invest this amount, the difference could be higher.

Understanding How Using Less CPF For Our Mortgage Can Help Us Grow Our CPF

The table above illustrates the trade-off that we make when we commit CPF funds for home mortgages. While we get short-term cash flow respite, it comes at the expense of our retirement. Conversely, if we use more cash today for our home mortgage repayment, we accumulate more CPF savings for retirement.

The Limitations With The Endowus CPF Calculator

As most of us would realise by now, how CPF contributions, interest rates and withdrawals work is complex and can be difficult to understand, even though the information are all publicly available information. Beyond understanding them, the calculations can also be tricky as certain assumptions on how the CPF Full Retirement Sum and Basic Healthcare Sum will have to be made. These are shared transparently by Endowus.

The Endowus CPF Calculator does come with certain assumptions and limitations that are stated on their website and are worth taking note of. For example, one major assumption is that investment returns are linear to simplify the calculation. Volatility in investment returns especially during retirement can have a significant impact on how fast your retirement wealth can last you. The assumed return is also fixed – at 7.6% p.a, which may not be the case since no one can predict how future investment returns will be.

There is also an assumption that we will be employed throughout the course of our career earning the same salary and even enjoying a gradual increment this year. This may not be realistic. Throughout our career, there may be occasions when we are not working and getting CPF contributions or may not be able to earn the same level of salary.

Yet, despite these limitations, the Endowus CPF Calculator is still exceptionally useful in illustrating to us how small CPF decisions, like investing a part of our OA, can make a significant difference in our CPF savings for retirement.

CPF Decisions Can Have A Significant Impact On Our Retirement

For those of us who want to invest our CPF monies but do not have the knowledge or the time to do so, Endowus allows us to invest our CPF monies through them. The all-in-one access fee that Endowus charges is 0.40%. Do note that these fees are not inclusive of the fund management fees which are charged at the fund level. According to Endowus, the fund-level fees for its portfolios are at institutional levels ranging from 0.50% to 0.56% per annum, which is significantly lower than what typical retail funds charge (and what investors generally must pay when using a traditional advisor).

Even if we are not planning to invest our CPF monies now, it’s still important for us to understand how the decisions (or non-decisions) we make today can have a major impact on our future retirement. The Endowus CPF Retirement Calculator helps to forecast our CPF balance during retirement, and the type of decisions we can make today to grow our retirement nest egg.

If you have not invested your CPF with Endowus, or are new to Endowus, you can get $20 off your access fee by leaving your email address for the CPF calculator report.

Read Also: How Much More (Or Less) Would You Have For Retirement If You Invest Your CPF Savings