From time to time, we may receive blank cheques from our banks in our letterboxes. In Singapore, we’ve been brought up to be very cynical whenever we’re offered something for free – especially money. Upon closer inspection of these blank cheques, we would quickly realise that they are simply marketing tools, trying to get us to take up more of their services – namely, a credit card balance transfer.

Further down in the article, you will see that we used DBS as the example. This is only because it was the blank cheque that came in most recently and was surprisingly quite useful. We have received blank cheques from other banks in the past, and looking at online chatter, it seems that most other banks in Singapore employ this marketing strategy.

Is This An Ethical Practice?

Our good friend at Budget Babe called into question, via an article she wrote, the ethics behind this marketing tactic.

Read Also: Warning: Do NOT Bank In These “Cheques” You Get From The Banks!

There are really two facets of ethics to consider: 1) is it a legitimate product VS a scam? and 2) is it being marketed in a fair way.

The first part of the question is quite clear to answer. These blank cheques are marketing a legitimate and, in many cases, extremely useful product called credit card balance transfers. It is far from a scam.

The second aspect of the question is less straightforward – is it marketed in a fair way? For someone who is younger or the financially savvy, there should be no question that most of us would be aware of what we’re getting into – especially if we got money we don’t own from a financial institution in our mailboxes.

It’s also hard to imagine that our banks are deliberately targeting older or illiterate people. First and foremost, we’re fairly confident that our financial institutions do not work in such an unethical or prejudicial method.

More importantly, this is simply a form of targeted marketing, and usually based on data of our credit usage and/ or worthiness, rather than financial literacy. It’s also quite fair to assume that people, both young or older, would be financially-savvy and familiar with banking practices if they’re already utilising several banking products.

In the off chance an older or illiterate person receives such blank cheques, we’re confident that growing up in Singapore would have made this person extremely guarded to receiving free money, especially in form of a blank cheque.

Arguably, the older generation may be even more vigilant about tracking every cent they own, spend and would be receiving. Not to mention, they’re also very apprehensive when encountering anything new or foreign (think internet or mobile banking), and will most likely ask family members or friends if they’re unsure about this blank cheque.

Yes, these blank cheques are a curious thing to receive in our mail. However, we believe most people would see it for what it is – the marketing of a product.

We Banked In Our Cheque So You’d Know What Really Happens

If you’ve ever wondered what would happen if you banked in one of these cheques, we did it so you don’t have to continue guessing.

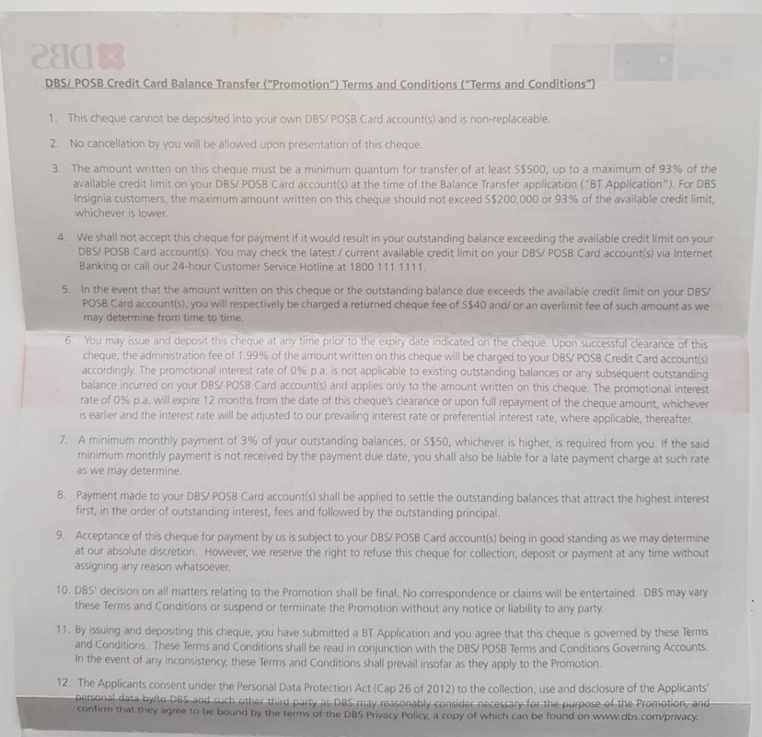

Firstly, here’s the blank cheque and accompanying letter one we received in our mail. It’s pretty straightforward: alerting us that this product is a credit card balance transfer product, as well as depicting the interest rate (and effective interest rate) we have to pay if we choose to proceed with the credit card balance transfer.

Having read the lengthy terms and conditions, we proceeded to fill in the details and deposited the cheque in our account. In particular, we had to take note of these T&Cs more carefully:

# 1 Take a credit card balance transfer of $500 or more;

# 2 Ensure we don’t write an amount that exceeds our credit limit (this means knowing how much we’ve spent as well as taking fees/ charges into consideration on the particular credit card that we’re using for the balance transfer);

# 3 Note that we have to pay a minimum of 3% of our credit card balance transfer amount each month;

# 4 Note that we have to settle the entire amount within 12 months to avoid getting charged the prevailing rates (which is currently close to 25% per annum)

Our credit limit was stated as $6,000. So, we veered on the safe side by writing a cheque for $4,000.

Within just two days of depositing our cheque, the $4,000 was deposited into our account.

Simultaneously, our credit limit on the credit card we applied the credit card balance transfer from was cut to $2,500 from $6,500. This was all done very smoothly, without any hiccups.

Pros And Cons Of Depositing This Blank Cheque

We’ve never really considered these blank cheques before as we never had the need for such credit. However, more people started asking us this question and while we had an idea of what was in store, first-hand experience and greater research needed to be done to deliver a comprehensive pros and cons narrative.

Read Also: Pros And Cons Of Taking A Credit Card Balance Transfer

The Pros

# i Easy And Convenient

It was a very simple process to take up the credit card balance transfer. The money was deposited into our account very promptly – within two days. This is great for people who are in urgent need of cash – either to pay for something or refinance other high-interest debts from other financial institutions.

As depicted via screenshots and pictures that we took, the payment terms were also exactly as stated on the mail, and we didn’t have any further hidden charges to deal with.

# ii Low Interest Rates

The low interest rate of 1.99% (effective interest rate (EIR): 2.32%) was very enticing. This could be used to pay off other high-interest debts that we may have (usually more than 25% per annum) or even to put into investments giving us better returns over a one-year period.

# iii Even Lower Interest Rates Than Promotional Rates On Its Website

Researching a little deeper, we realised the interest rates for banking in the blank cheque was even better than the rates stated on the DBS website for the same product, which carried a one-time processing fee of 4.5% (EIR: 5.2%).

This was most likely due to the fact that we were deliberately targeted by the DBS marketing team, for always paying our credit card bills on time and/ or have relatively good credit scores. Also, this product was pushed to us rather than us actively seeking it, thus, an enticing rate would have been required.

The Cons

# i Lower Credit Limit On Our Card

Our credit limit fell to $2,500. This means that instead of being able to spend up to $6,500 previously, we will only be able to spend up to $2,500. This was further reduced by $80, or the one-time administration fee, when it came time to settling our first payment.

Miscalculating this, coupled with spending to our maximum credit limit available, could have left us in a situation where we bust our credit limit, and potentially incur penalties.

Another point to note is that we could easily increase our credit limit by up to 4X our monthly salary or apply for another credit card to get more credit, if required.

# ii Limited Tenure Of 12 Month

We are limited by the 12-month tenure of this credit card balance transfer. Which means that if we are unable to pay the amount in full within 12 months, we will incur the prevailing rates of close to 25% per annum.

We may not be able to extend this tenure easily, which means any refinancing or investment decisions will be limited by this tenure.

We also can’t use this to pay for longer term loans such as our student loans, renovation loans or other higher-interest debt that’s substantial, mainly due to the short tenure of this loan facility.

Read Also: Have Unpaid Credit Card Bills? Here’s How Taking A Credit Card Balance Transfer Can Help You

# iii This Is Ultimately A Credit Facility

Applying for too much credit will affect our credit scores in the longer-term. In addition, carrying too much debt may put a burden on our finances, especially if we have a short runway (of 12 months) to repay the loan.

Repaying This Credit Card Balance Transfer

At the end of the month, we were notified of what we were supposed to pay to the bank.

As you can see, we owed them $4,079.60. This was our $4,000 credit card balance transfer, that we received in cash, and the administration fee of $79.60, or 1.99% of our credit card balance transfer.

At the same time, our credit limit fell by the additional amount of our administration fee. So, we have to note this when we’re taking up this promotion as well, to not bust our credit limit.

In total, we had to pay a minimum of $122.39 by 11 September. This amounted to approximately 3% of our total outstanding balance. Which was also as promised by the mail that we received.

We need to have these figures in our mind as we look for other credit card balance transfers to take out in the future as well as keep up with existing payments in order to avoid hefty fees that will be slapped on us if we fail to pay the minimum monthly amount and outstanding amount after 12 months.

In a way, the banks are giving us extremely cheap loans to establish good relationships with good borrowers. For the bad borrowers, they’re betting that they can receive better returns in the long term by getting them to transfer their debt from another company to them.

Advertiser Message

Thinking Of Switching Brokers Or Consolidating Your Holdings?

Tiger Brokers is currently running a transfer-in campaign where eligible clients can receive an iPhone 17 Pro Max* when they transfer in their assets.

For SGX investors, there is also a CDP Transfer promotion with 0* commissions on Singapore stocks.

Find out more here. *T&Cs apply.

Bonds and Fixed Income

StashAway Income Portfolio: How You Can Earn 4.6%* Dividends From Your Investments Each Year