This article was contributed to us by AIA Singapore.

Getting a critical illness insurance policy is an important step in plugging your overall insurance protection gap in Singapore.

According to the Life Insurance Association of Singapore (LIA), economically-active Singaporeans and Permanent Residents (PRs) have a critical illness protection gap of 80% and mortality protection gap of 23%.

This demonstrates that critical illness protection needs may be neglected by a substantial number of people in Singapore. While critical illness plans are not new in the market, there may be a few reasons why they may be more overlooked than life protection.

Before you get your critical illness insurance coverage, you need to know these 5 things first.

Read Also: 5 Reasons Why Many Singaporeans Have A Huge Critical Illness Protection Gap

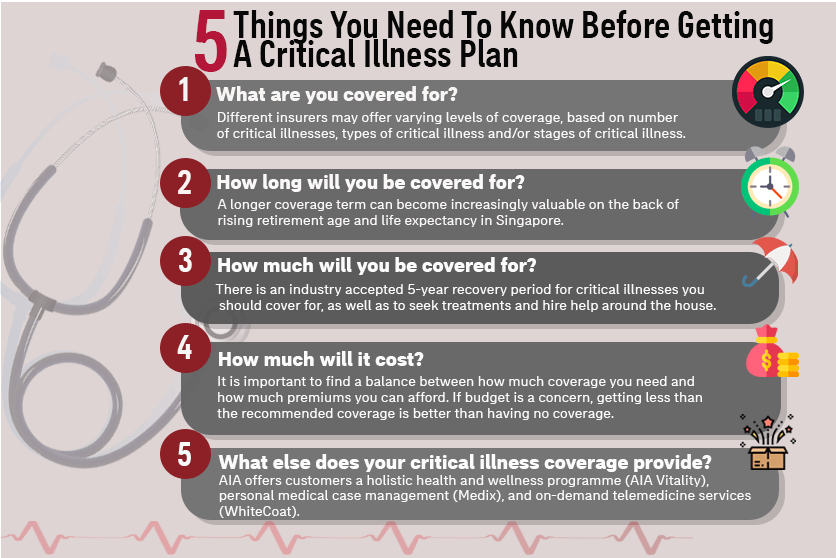

#1 What Is Covered Under Your Critical Illness Insurance?

Critical illness coverage can be more complex than life insurance coverage. For life insurance plans, a payout to your beneficiaries is triggered when you pass on or are left in a situation of total permanent disability (TPD).

For critical illness coverage, different insurers may offer varying levels of coverage, based on the number of critical illnesses, types of critical illnesses and/or stages of critical illnesses covered. Another factor that may prevent people from trying to learn more about critical illness insurance is the medical jargon that is commonly used to describe coverage levels.

Rather than avoid the topic, you should spend more time and effort trying to learn more about critical illness plans and which provides the most suitable coverage for your needs.

One way to determine if a critical illness insurance plan is comprehensive is to look into the LIA’s critical illness framework detailing an industry-accepted list of 37 critical illnesses and its definitions. You can also refer to data from the Ministry of Health (MOH) for principal causes of death in Singapore.

For example, AIA’s latest critical illness plan, AIA Power Critical Cover, offers comprehensive coverage for 175 conditions. This includes 10 Pre-Early Benefit, 150 multi-stage critical illnesses and 15 special conditions.

The policy also provides a Power Reset Benefit, which fully restores your coverage amount once 12 months have passed from your last claim allowing you to make multiple claims of up to 500% of your coverage amount. There’s also a Power Relapse Benefit, which provides up to 200% coverage amount if you suffer from any of the five leading critical illnesses same critical illness once 24 months have passed from the last claim.

You can read about this in greater detail in our AIA Power Critical Cover brochure.

#2 How Long Does Your Critical Illness Insurance Provide Coverage For?

Each of us will have our unique critical illness insurance needs and wants. While there are critical illness insurance plans that offer an option to extend our coverage up till age 100, there are also plans with shorter coverage tenures.

In general, longer-term critical illness coverage can become increasingly valuable on the back of increasing retirement age and life expectancy in Singapore. Even in the scenario you retire or do not have any dependents, you may continue to need a critical illness payout to sustain your current lifestyle, or to hire help to care for yourself. With rising life expectancy, you may also have elderly dependents to care for even after you stop working in the future.

AIA Power Critical Cover provides two options for your preferred coverage period. AIA Power Critical Cover Value Plan provides coverage up to 75, while the AIA Power Critical Cover Life Plan provides coverage up to 100. Under the Life Plan, you will also have a Maturity Benefit[2] at age 100, as well as Surrender Benefit[2] of between 75% and 99% of your coverage should you decide to surrender your policy.

With certainty of coverage till 100, you are assured that no matter when you are diagnosed with a critical illness, you have a financial safety net for yourself and your loved ones.

In the event of your untimely death, your loved ones will receive 100% of your coverage amount, less any critical illness benefits already paid, as well as a compassionate benefit of $5,000.

#3 How Much Should Your Critical Illness Insurance Coverage Be?

When deciding how much we need to be covered for, we can again refer to the LIA for its benchmark 5-year recovery period for critical illnesses.

While you are recovering from a critical illness, the last thing you want to stress about is how you can continue to afford your current lifestyle. At the same time, you have to continue paying for your home loans, electricity and water bills, mobile and internet bills, children’s allowance and so on.

While you may be able to tap on your savings to pay for these expenses, it may put your family’s financial future at greater risk, especially in the worst-case scenario where you don’t recover and cannot replenish that savings.

This is where a payout from a critical illness plan becomes valuable. Apart from just taking away the stress of being able to continue paying for your daily expenses, you can also use this payout to seek treatment.

To calculate the actual number that you would need coverage for, a safe figure would be more than five years of your annual expenses. This is because, in addition to your current expenses, you may also incur additional expenses from getting the treatments that you want and potentially needing to hire help around the house or to provide care for you.

#4 How Much Will Critical Illness Insurance Cost?

Having a comprehensive critical illness plan can be valuable, but it also costs money. We need to consider the affordability of the plan, while striking a balance between other important expenses, such as our daily living expenses, investing for our retirement and saving for our children’s education.

Even if you have trouble affording a coverage level worth the recommended five-year recovery period, you should consider getting lower coverage rather than no coverage.

#5 What Else Does Your Critical Illness Coverage Provide?

Some insurers provide value-added services to help keep their customers healthy.

For instance, when you purchase AIA Power Critical Cover, you will able to leverage on AIA Vitality, a health and wellness programme designed to encourage and reward you for living well. The programme takes a comprehensive approach in providing you with the tools and support you need to understand your health, and ways you can improve it, while providing you with rewards to motivate you along the way.

Another value-added service you will have access to is Medix, which allows you to get personalised medical support from world-leading specialists for your critical illness condition for a minimum of 3 months.

Through AIA, you will also be able to tap on WhiteCoat, an online medical consultation service. With a flat consultation fee of $12 (excluding GST and delivery charges), you will be able to receive professional medical advice from Singapore-registered doctors via video consultations and have your prescribed medicine delivered to your doorstep within 90 minutes.

[1] Re-diagnosed major cancer, recurred heart attack, recurred stroke, repeated major organ/bone marrow transplantation, repeated heart valve surgery.

[2]The surrender benefit of 75% of the coverage amount shall be payable on or after the 60th policy anniversary or at age 75, whichever is earlier, plus additional 1% for each progressive year from age 76 onwards. The maturity benefit of 100% of the coverage amount will only be payable when the policy matures at age 100. Both surrender and maturity benefits will be subject to deduction of any critical illness benefit paid and amounts owing to us.

Read Also: Understanding Critical Illness Plans: How Different Types Of CI Plans Work