Over the past few years, I have started investing a portion of my excess CPF OA savings through Endowus.

The logic behind this is fairly straightforward. By “excess” OA savings, this refers to funds beyond what I need to comfortably cover my home mortgage payments for a few years, if I were to lose my job and stop receiving an income. Once that safety buffer is in place, it seems reasonable to ask whether the remaining balance (and the interest rates that I earn on the entire balance) could be put to better use. In my case, I decided that investing part of these excess OA savings could help grow my retirement funds faster over the long term.

Of course, investing is not the only option. I could also transfer some OA savings to my Special Account to reach the Full Retirement Sum earlier. But while that would increase the nest egg I have in my CPF account, it does not provide any additional tax benefit. For me, that made investing the excess OA funds a preferred option at this point in time for me.

Still, investing CPF OA savings through the CPF Investment Scheme (CPFIS) is not something we should do casually, and there are a few valid reasons why we need to be careful when investing our CPF savings.

Investing Our CPFOA Comes With A Cost

The first point to recognise is that investing our CPF savings comes with a cost. CPF OA savings already earn a guaranteed 2.5% a year, risk-free. What many CPF members may not fully appreciate is that this return is not only risk-free, but also cost-free. We don’t pay any management fees or transaction fees to earn this return.

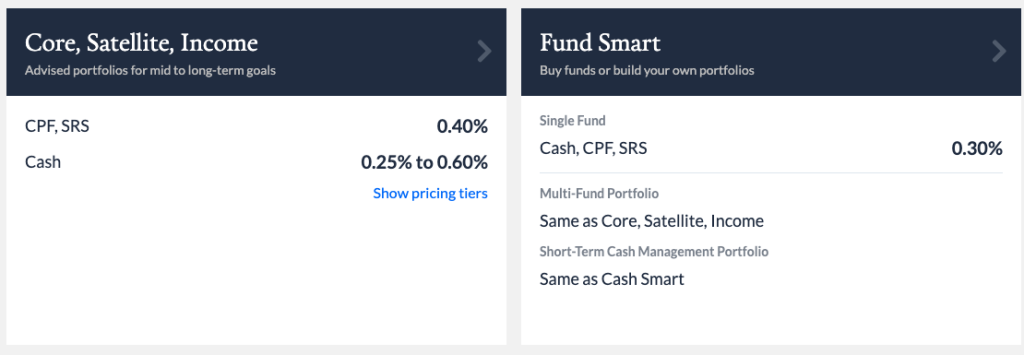

Once we choose to invest our CPF OA savings, that changes. For example, by investing my CPF OA through Endowus through its advised portfolio, I pay a 0.40% annual management fee. On top of that, the underlying funds also charge their own fees, which further reduce the net return we eventually receive. This means the question is not just whether investing can deliver higher returns, but whether those higher returns are enough to justify the added risk and cost.

Endowus Fees for CPF Investments

Investing Our CPF OA Requires Us To Take On Additional Risk

Just as importantly, investing our CPF OA means being okay to accept some level of investment risk. Unlike the 2.5% interest we earn in the Ordinary Account, investment returns are not guaranteed. They depend on market conditions, the timing of our investments, and, of course, the portfolio we choose. This means we need to be prepared for the possibility of losses, at least in some years.

That said, there are ways to manage this risk. One is to 1) choose a more conservative portfolio, with a higher allocation to fixed income assets rather than going fully into equities. Another is to 2) invest with a sufficiently long time horizon so we have a better chance of riding out short-term market volatility. Finally, building a 3) globally diversified portfolio can also reduce concentration risk, since we are not relying too heavily on any single market, sector or company.

Why Investing My CPF Savings Through Endowus Makes Sense For Me

While Endowus does let CPF investors pick their own CPFIS-eligible funds via Fund Smart, that is not the route I took. This is because building your own portfolio means doing the research, choosing the right funds and making sure every investment fits with how you think about risk and long-term returns. While I could do that if I wanted to, it also takes time and ongoing attention. At this stage of life, with work, family, and everything else being the higher priority for me, I preferred to use Endowus’ advised portfolio and leave portfolio construction to a system built for that purpose.

Another reason is the access to global markets. In my view, one of the biggest limitations of staying too focused on Singapore is that our market is relatively small and concentrated. Through CPFIS, we can invest in local stocks and ETFs if we want, but a globally diversified portfolio gives us exposure to a much wider range of companies, sectors and economies.

That includes many of the large-cap businesses in the US and other major markets that have driven a significant share of global equity returns over time. Of course, there are no guarantees, but I believe a global portfolio gives me a better chance of achieving stronger long-term growth.

The final reason is simply my time horizon. Since I am still decades away from accessing my CPF savings, I feel I can afford to take a more aggressive, longer-term view.

For me, as long as I have already kept enough in my OA to cover my home mortgage for the next few years, I do not mind taking on more short-term volatility in exchange for the potential of higher long-term returns.

Thus far, returns have been strong in the past few years since I started investing my CPFOA through Endowus, but as we all should already know, relying on past returns to project future returns is not a good idea.

The Case For Investing Your CPF OA Savings

Investing some of your CPF OA savings can make sense, but in my view, only if the basics are already in place.

That means having enough set aside for your housing needs if you are using your OA for housing instalments, being comfortable with the reality of market risk, and having a long enough investment horizon to ride out the inevitable ups and downs. In practice, that usually means thinking in terms of at least 10 years, and ideally much longer.

Just as importantly, how you invest matters as much as whether you invest. While Endowus gives you the option to choose individual CPFIS-eligible funds yourself, that route is not for everyone. For those who do not have the time (like me), interest or confidence to build and monitor their own portfolio, an advised portfolio might be the more practical and disciplined approach.

At the end of the day, CPF OA money is not money we should put at risk lightly. But if you have excess OA savings, a mortgage buffer in place, and decades before retirement, leaving everything untouched at 2.5% may not always be the most efficient choice either. For some CPF members, allocating a portion of their savings to a globally diversified portfolio could be a sensible way to pursue better long-term growth. For others, transferring your OA to your SA could be the obvious choice.

The key is not to ask whether investing your CPF OA is good or bad. The better question is whether it fits your risk tolerance, current housing needs and retirement timeline. If it does, then investing your excess CPF OA may not just be an option worth considering. It may be one of the smarter long-term moves you can make.

Invest Better With Endowus

If you’re interested to start investing with Endowus, you’ll be happy to know that DollarsAndSense readers can enjoy $50 off their access fee Sign-up using this link to claim this special offer. Terms & Conditions apply.

Read Also: 8 Types Of Investments You Can Make Using Your CPF OA Monies Via The CPFIS-OA

This article contains affiliate links. DollarsAndSense may receive a share of the revenue from your sign-ups. You can refer to our editorial policy here.