This article was written in collaboration with HSBC Life. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

When it comes to retiring in Singapore, there are typically two main goals that people living in Singapore have. Retiring well is the first obvious goal. Given the high cost of living and the relatively luxurious lifestyle that many of us may be used to, retirees need to ensure they have enough passive income in their golden years.

The other goal some retirees have is to leave a legacy for their children. This usually refers to what we leave behind, including our financial assets.

This desire to leave a financial legacy while still having enough to retire well may appear to be contradictory goals. After all, retiring well is likely to incur more spending – implying that we may leave a smaller legacy to our children or grandchildren.

For many Singaporeans, our CPF savings and HDB flats are the main instruments that we rely on to retire well while leaving behind a legacy. Through CPF LIFE, we receive a lifelong monthly income that can be used to cover basic living expenses during retirement. Due to the manner CPF LIFE payouts are structured, the tradeoff is that we may not have a substantial bequest of CPF monies, if any, when we pass on.

For elderly Singaporeans who own and live in their HDB flats, leaving behind their flats is one way to leave a legacy. However, if our adult children already have their HDB flats or private properties, they can’t take over ownership of our flats, unless they sell their existing properties.

Retiring Well & Leaving A Legacy Doesn’t Need To Be Mutually Exclusive Retirement Goals

When we look at our CPF savings and HDB flats, it’s easy to think that retiring well and leaving a legacy are mutually exclusive retirement goals. However, this isn’t necessarily true.

Using the right financial products, we can plan for a comfortable retirement, while ensuring that we leave a legacy for our children.

Introducing Flexible, Long Term Saving-Focused Insurance Plan

We don’t have to rely solely on our CPF accounts and HDB flats for our retirement and to grow wealth. Through flexible long term saving-focused insurance plans, we can grow our wealth and have the financial assurance we need for ourselves and the next generation.

An example of such a product is the HSBC Life Wealth Builder. This product, which is a long-term endowment plan, can be used not only to supplement our own retirement adequacy, but also that of our children, or even grandchildren!

The HSBC Life Wealth Builder covers life insured up to age 120 years and can be passed from one policyowner to another. While the plan constantly builds up cash value, policyowners can enjoy access to the cash value of your policy as and when it’s required to fund key milestones in life, be it for your retirement or when your child enters tertiary education.

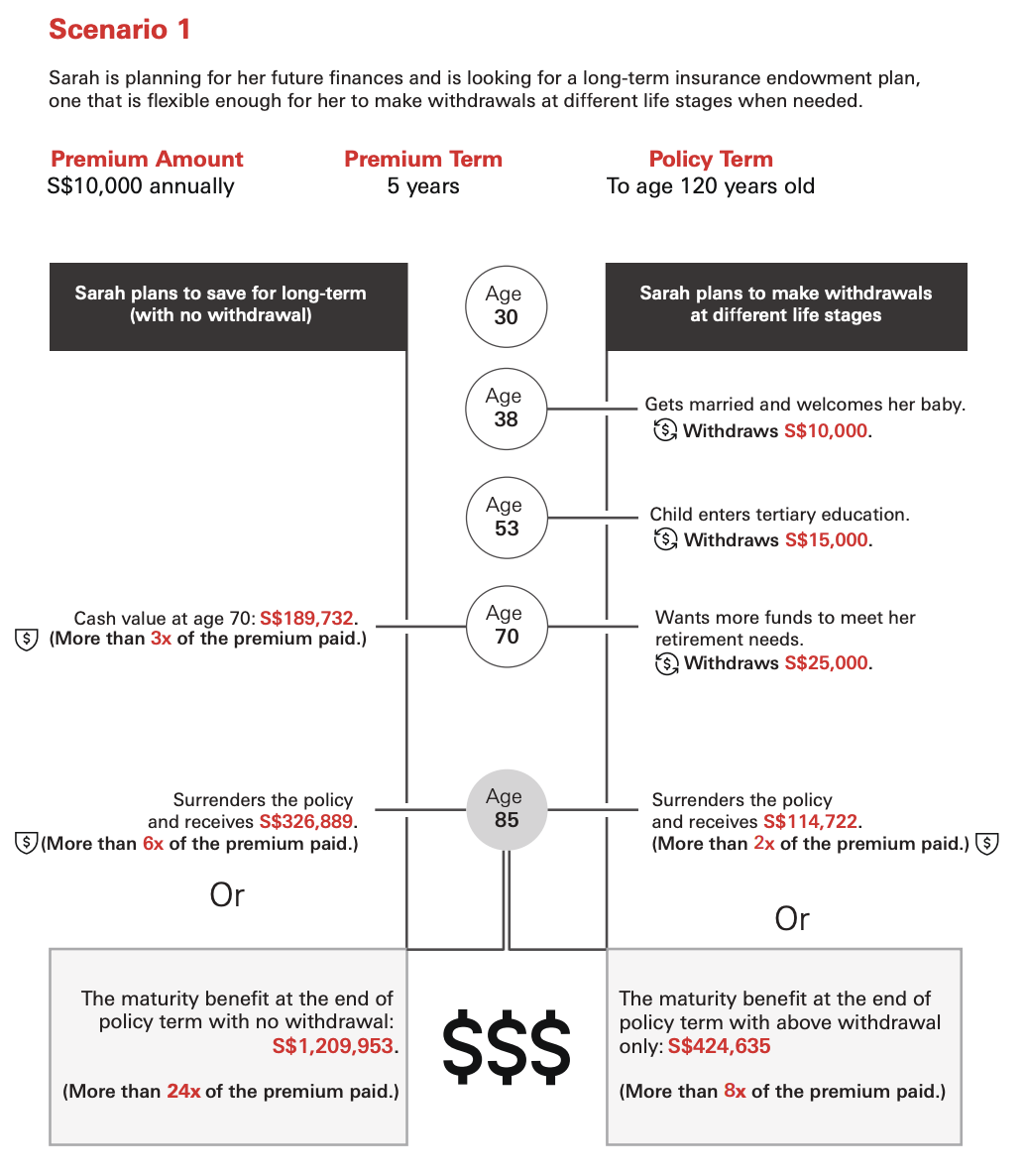

Source: HSBC Life Wealth Builder Product Brochure

The above figures are for illustrative purposes only and are based on Illustrated investment rate of return of 4.25% p.a. Bonuses are not guaranteed and actual benefits payable will vary according to the performance of the participating fund.

In the first example above, we can see that despite withdrawing S$50,000 across three different life stages, Sarah still enjoys a maturity benefit that is more than 8x of the original premiums (S$10,000 annually for 5 years) that she paid by the end of the premium term.

With a coverage lasting up to age 120 year old of the (first) life assured, the HSBC Life Wealth Builder allows parents to buy this long-term endowment plan for themselves, and subsequently transfer ownership of the plan to your child if you want. Doing so will enable parents to stretch the lifespan of this policy beyond what you can reasonably expect yourselves to live.

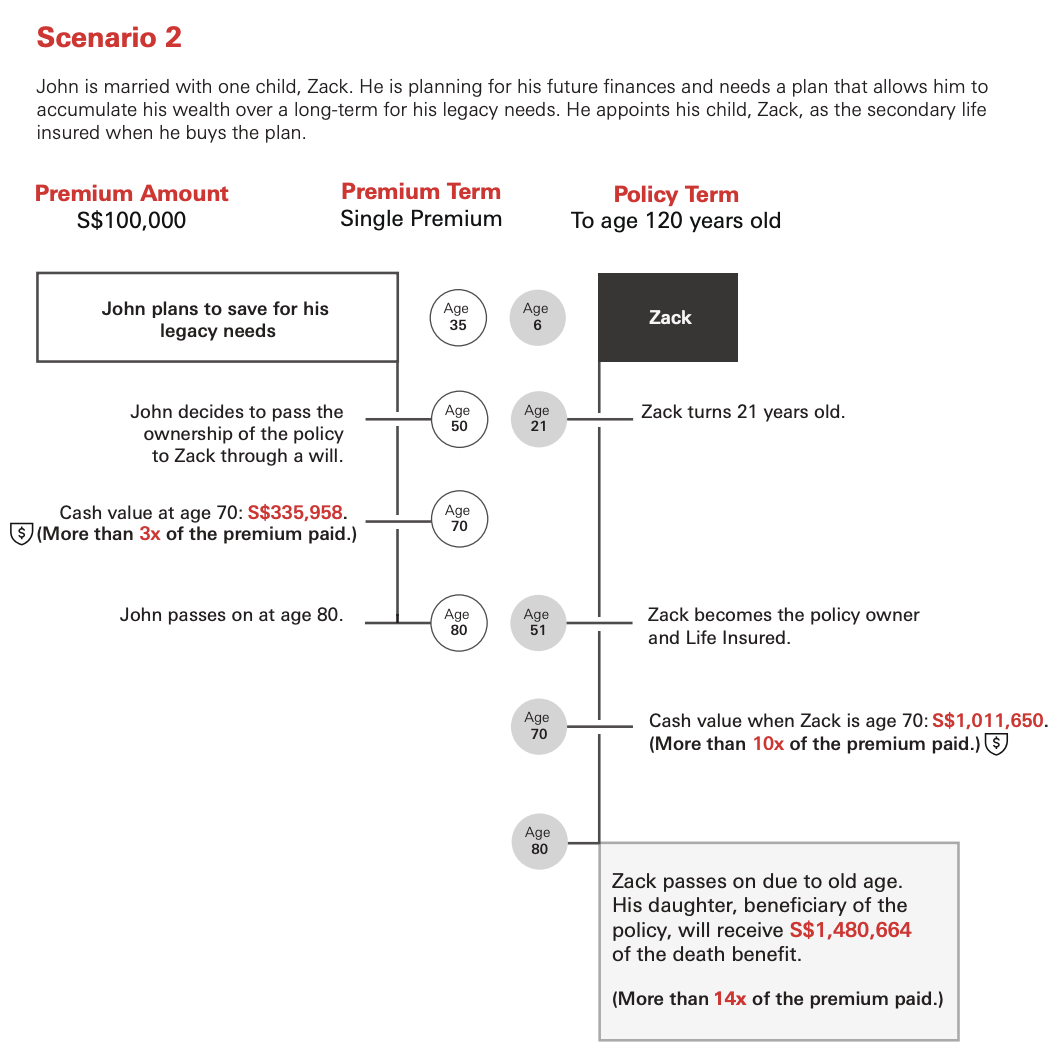

Source: HSBC Life Wealth Builder Product Brochure

The above figures are for illustrative purposes only and are based on Illustrated investment rate of return of 4.25% p.a. Bonuses are not guaranteed and actual benefits payable will vary according to the performance of the participating fund.

In the second example above, we can see that a father, John purchases the plan at age 35 via a single premium of S$100,000 and subsequently, transfers the ownership of the policy to his son Zack through a will. In the illustration, having held the plan for a total of 74 years (across both father and son), the total payout when the son passes on at age 80 is S$1,480,664, more than 14x the original premium (S$100,000) paid.

The example above assumes that neither the father nor son make any withdrawals from the plan contributing to the accrual of a larger lump sum payout upon the insured event happening. However, if they had preferred, both policyowners would have been able to withdraw from the plan as and when they needed perhaps to fund any shortfall in their respective retirement or for any other milestone life stages.

In this way, the HSBC Life Wealth Builder can give you, as parents, potentially the best of both worlds. As you start saving and contributing towards this plan at a younger age, the amount accumulated in the policy will not only grow over time, but can also be used to fund your retirement, and serve as a legacy that can secure your children’s retirement.

Besides the flexibility in making withdrawals, other advantages of the plan are that policyowners can choose a premium term that fits your payment preference. This can be a one-time single premium, or over 5, 10 or 15-year premium term. Do note that cash value, as illustrated in the plan, comprises of both guaranteed and non-guaranteed bonuses. If the policyowner suffers from Total and Permanent Disability (“TPD”), the remaining premiums will be waived.

Start Planning From A Young Age

One of the key reasons why the HSBC Life Wealth Builder can be used to fund both your retirement and to secure a legacy for your children is because it utilises time to work in its favour. With a coverage of (first) life insured to 120 years old, the plan gives you the option to build wealth over multiple generations, and not just during your lifetime.

At the same time, unlike investing in an expensive property and locking up your retirement nest egg, such a plan allows you to fund your retirement today, while leaving a legacy for the future.

If you are keen to consider this product, you can find out more details about this plan on the HSBC Life website. To better understand how this product may be suitable for you, we strongly recommend that you speak to a HSBC relationship manager who can share more details about this plan. Make an appointment or visit your nearest HSBC branch to apply in person.

Note:

Based on an illustrated investment rate of return of 3.00% p.a., the total potential cash value for:

Scenario 1: If Sarah makes no withdrawal: Cash value at age 70 is S$126,627, full surrender value at age 85 is S$203,008, maturity benefit at the end of the policy term is S$642,584.

If Sarah makes the above withdrawals: Full surrender value at age 85 is S$45,460, maturity benefit at the end of the policy term is S$143,895.

Scenario 2: Cash value when John is age 70: S$231,654, cash value when Zack is age 70: S$591,250, death benefit when Zack passes on at age 80: S$827,980.

Disclaimer

HSBC Life Wealth Builder is underwritten by HSBC Insurance (Singapore) Pte. Limited

(Reg. No. 195400150N).

This article contains only general information and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person. This is not a contract of insurance and is not intended as an offer or recommendation to buy the product. A copy of the product summary may be obtained from our authorised product distributors. You should read the product summary before deciding whether to purchase the product. You may wish to seek advice from a financial adviser before making a commitment to purchase the product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. Please refer to the policy contract for the exact terms and conditions, specific details and exclusion of this product. As buying a life insurance policy is a long-term commitment, an early termination of the policy usually incurs high cost and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid. Buying health insurance products that are not suitable for you may impact your ability to finance your future healthcare needs. It is also detrimental to replace an existing life insurance policy with a new one as the new policy may cost more or have fewer benefits at the same cost.

This policy is protected under the Policy Owners Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us or visit the LIA or SDIC websites (www.lia.org.sg or www.sdic.org.sg).

Information is correct as at 6 January 2022.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Bonds and Fixed Income

StashAway Income Portfolio: How You Can Earn 4.6%* Dividends From Your Investments Each Year

Branded Content

How To Build A Retirement Portfolio That Can Last A Lifetime