This article was first published by Cheerfulegg.

When I first started work, I used to go clubbing all the time. I don’t even know why I went so often – most of the time I was just sipping beers with my buddies trying to look cool. Every weekend, I’ll throw down like a hundred buckeroos trying to get tipsy on beer and Graveyards.

One day, I woke up and realised that I probably spent like $1,500 in butterfactory over the course of a year. It was scary. Dammit, butterfactory!

So I realised that I should proooooobably track my spending a little closer (and live a little more sensibly).

Since then, I’ve made improvements in how I manage my spending. I still splurge on the things I love, but the difference is that I now know exactly where my money goes to, and I drive it to where I want it to go.

Over the past 2 weeks, I shared with you the Automatic Money Jar System I use to manage my moolah:

So today, I’m gonna show you how to track the money you spend from your Money Jars.

Lots of financial bloggers track their spending. For example, my friend 15HWW posts his expenses on his blog every month – all the way down to the individual items. I really admire him – because I’m definitely not disciplined enough to do that.

Sooooo, I created a way to track my spendizzle without feeling like killing myself every time.

But tracking is such a pain in the ass!

I know what most people are thinking:

I know what most people are thinking:

I don’t wanna track my spending on $1.20 coffee and $4.50 ban mian! I just want to spend my hard-earned money and not feel guilty about it. Stop telling me how to live my life, Lionel!

But people who focus only on the act of tracking are missing the point.

My friend Kyith from Investment Moats wrote a great article talking about why tracking your spending – on its own – is just data collection. If you want to improve your wealth, you need to do something with that data.

90% of people live their lives having only a vague idea of where their money goes to. They’ll say things like:

I think I spent too much on travelling last month, so I think I shouldn’t spend so much this month.

while munching on the cucumber sticks that they brought for lunch.

But imagine how powerful you’d be if you KNEW exactly where your money went to every month:

- You can pinpoint where you’re overspending, and know EXACTLY how much to cut down

- You can spend on things you love like travel, shopping, and movies, absolutely guilt-free.

- You can consciously redirect funds to your savings. A mere $50 increase in your monthly savings, properly invested, could be worth close to $10,000 after 10 years.

With the right system, tracking your spending is actually a super awesome way to get richer, and not just in the monetary sense.

But how do we make it as easy as possible?

The Fitbit Method of Money Management

Let’s take a leaf from the world of tech. In the past, if you wanted to know how much exercise you were getting, you had no choice but to guess. You’d say things like “I walked instead of taking the bus today, so I guess I exercised more”.

But now, with wearables like Fitbit – you can automatically track how many steps you’ve taken. Best of all, you can use it to change your behaviour: Fitbit lets you know whether you’re on track to meet your goal of walking say, 10,000 steps a day. If it’s 5pm and you’ve only taken 4,000 steps, you know it’s time to take the stairs instead of the escalator.

Easy, automated, effective.

Is there a Fitbit equivalent of spend tracking? Yes – it’s called a credit card.

Think about it: Charging everything to your card lets you:

- Consolidate everything into one convenient statement

- Earn points, rebates or miles for everything you spend on (hello, free flights!)

2 years ago, it was a pain to pay by credit card. Transactions were slow, and merchants gave me a death stare every time I paid for small items. But these days, you can use your card even for tiny expenses (yay, Visa Paywave!). I use my card for everything – from my $3,000 wedding dinner deposit to my $2.50 coffee at McDonald’s.

Of course, this only works well if you’re not an out-of-control spender racking up crazzzyyy credit card debt every month. Most Singaporeans are pretty prudent with their credit cards, so this will probably work for most of you. But if you have issues with paying off your credit card in full every month, stop reading. Use cash.

For the rest of you, read on:

Soooo… How Do We Do This?

Alright, let’s do this. It may seem like a lot of steps, but once you set it up, tracking your expenses becomes a breeze. This exercise takes me no more than 15 minutes a month, which is way shorter than an episode of Modern Family.

- Decide on the card you’ll use. Ideally, you should be using one card for 80-90% of your expenses so that you only have to go through one statement at the end of the month. It should preferably come equipped with Visa Paywave or MasterCard Passpass so you can tap for purchases quickly.

- Track your cash expenses– What about when you have to use cash, like when you’re buying food at the hawker centre or splitting a restaurant bill with friends? In these scenarios, do one of two things:

- If the item is below $10, don’t bother tracking it. It’s likely that your expenses on things like food/transport will average out, so just allocate a fixed lump sum (say, $300) on such expenses every month.

- If the item is more than $10, record it in a spend tracker app (I use iSpending), so that it can be easily accounted for at the end of the month. This literally takes just 10 seconds.

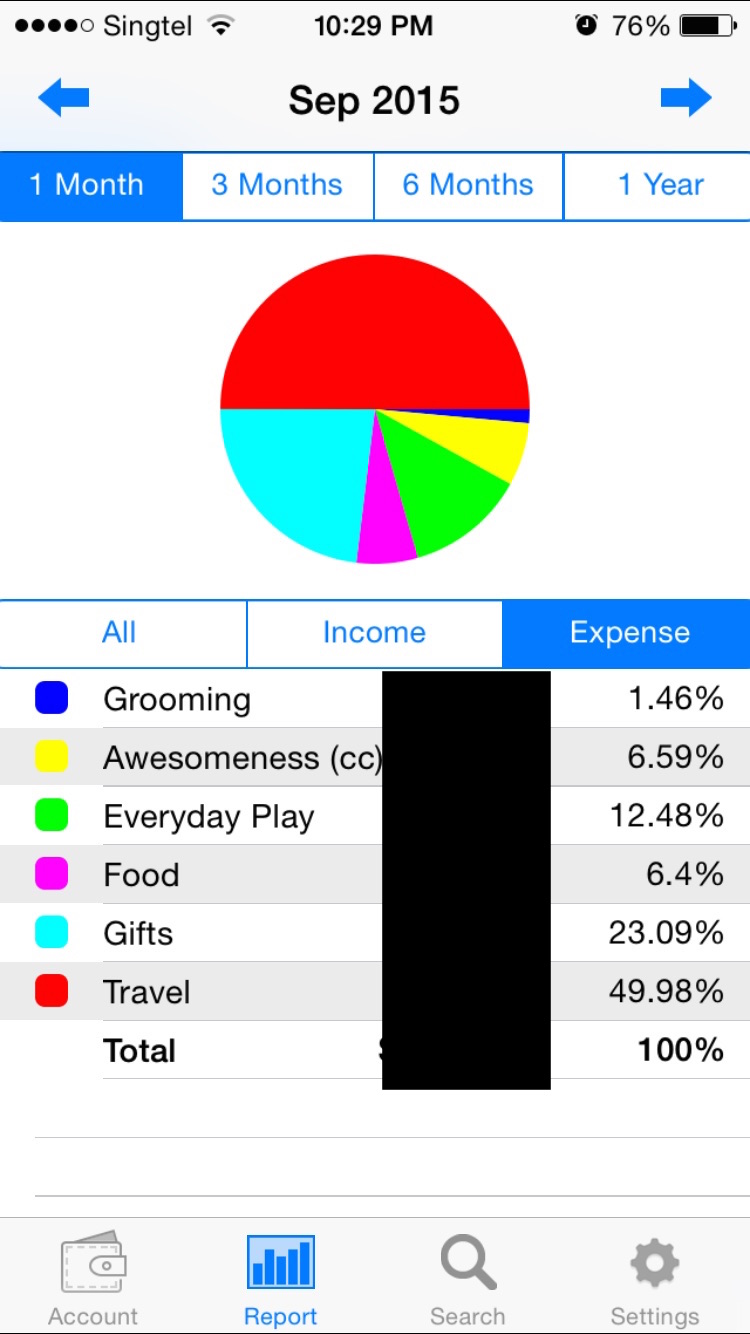

- Categorise your expenses – Go through your credit card statement when you get it at the end of the month (You should already be doing this anyway). The only difference is while you’re reviewing your statement, categorise your expenses into your pre-defined Money Jars. Personally, I like to key it all into my iSpending app. Then I tap “Report” and it generates a sweet pie chart for me:

I’m gross because I don’t spend much on grooming myself.

I’m gross because I don’t spend much on grooming myself.

Boom! I immediately know how much I spent on each category. You can also use a spreadsheet if you like, but I prefer using the app because my cash expenses are already on it.

- Pay off your credit card – Finally, transfer what you spent out of your Money Jars and into your main bank account. For example, if you spent $100 on movies this month, you’d transfer $100 out of your Entertainment Money Jar. Thereafter, you can use that cash to pay off your credit card.

Pro tip: Set up GIRO payments for your credit card, so that it’s paid off automatically every month.

Whatever Gets Measured Gets Managed

The point of this isn’t to know your expenses down to the last cent.

Instead, it’s about looking at your spending patterns and making sure they are what you want them to be. Are you spending too much buying stuff you don’t like? Are you spending too LITTLE on other areas, like your family, travel, or improving yourself?

After all, we can lie to ourselves, but what we spend on reflects who we really are. If we want to become better versions of ourselves, tracking where your money goes to is a good place to start.

So there you have it – a holistic system for managing your spending. To recap:

- We created our Money Jars

- We automated how much we put into them

- We tracked how much to take out of them

Most people won’t do this. Why? Because it’s a lot EASIER to stick to our old patterns. But all it takes is a simple system, throw in some technology, and we can get results like these:

“I do this so that there won’t be any financial surprises and there’d be money for everything that I need.” – Glanies T.

“This worked well for buying ETFs, (the) course fee for my songwriting class, and a Macbook for music arrangement.” – Ying W.

“One big category I had was (to) pay off a loan of over 80K. I am glad to say that category is now out of my list and replaced by travelling!!!” – Smita R.

Have you implemented a similar system for managing your money? Let me know in the comments about how it has helped you. I read every one.

To read more articles from Cheerfulegg, subscribe to their Cheerfulegg‘s VIP List.

Advertiser Message

Thinking Of Switching Brokers Or Consolidating Your Holdings?

Tiger Brokers is currently running a transfer-in campaign where eligible clients can receive an iPhone 17 Pro Max* when they transfer in their assets.

For SGX investors, there is also a CDP Transfer promotion with 0* commissions on Singapore stocks.

Find out more here. *T&Cs apply.