This article was written in collaboration with DBS. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, are purely for informational purposes, and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions, and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

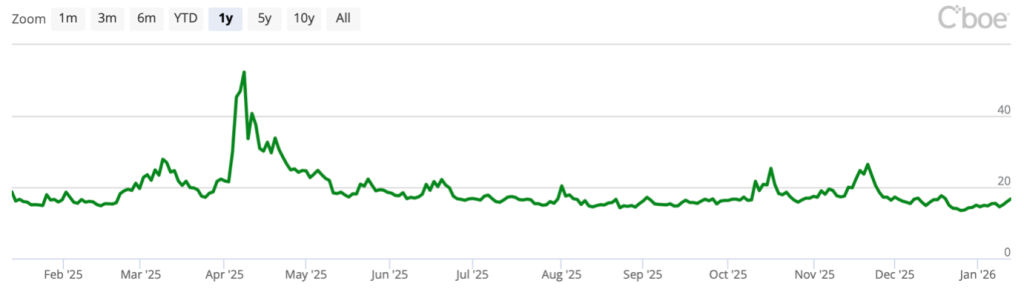

If you’re becoming more worried about your investments, you’re not alone. One common “fear gauge” for the market is the CBOE Volatility Index (VIX) – which signals heightened investor uncertainty when the index crosses 20 points.

In 2025, the VIX closed above 20 points on about 65 trading days – with the latest spike near the end of November 2025. In contrast, the VIX closed above 20 points on only 25 trading days in the whole of 2024, which came at the tail-end of the year.

Source: CBOE

This is likely a result of simmering geopolitical tensions, armed conflicts in various regions, and the two most powerful economies spiralling into a trade war.

At the same time, those seeking reprieve in the safest short-term fixed income, will find that Singapore’s T-bills yields have slid. The latest 6-month T-bill cut-off yield in January 2026 was just 1.39% p.a., less than half the nearly 3% p.a. cut-off yield investors could get last year. With the US Federal Reserve (Fed) cutting interest rates in early December – there could be further dips in T-bill rates.

Investors have to ask themselves some important questions, especially as markets become more volatile, to ensure your portfolio stays resilient – no matter the economic landscape shifts.

#1 How Long Do I Want To Invest My Money?

Your investment horizon, i.e. when you will need your money, fundamentally shapes the risks you can afford to take. If you are investing for long-term goals decades away, short-term volatility may be less relevant. On the other hand, if you need your funds in the next 1 to 3 years, near-term volatility becomes a far bigger consideration.

For investors with long investment horizons, time can be your biggest ally. Instead of trying to catch the market bottoms or avoiding risk assets entirely, you may be better off staying invested and continuing to invest regularly. This follows an age-old investing advice that emphasises time-in-the-market over timing the market.

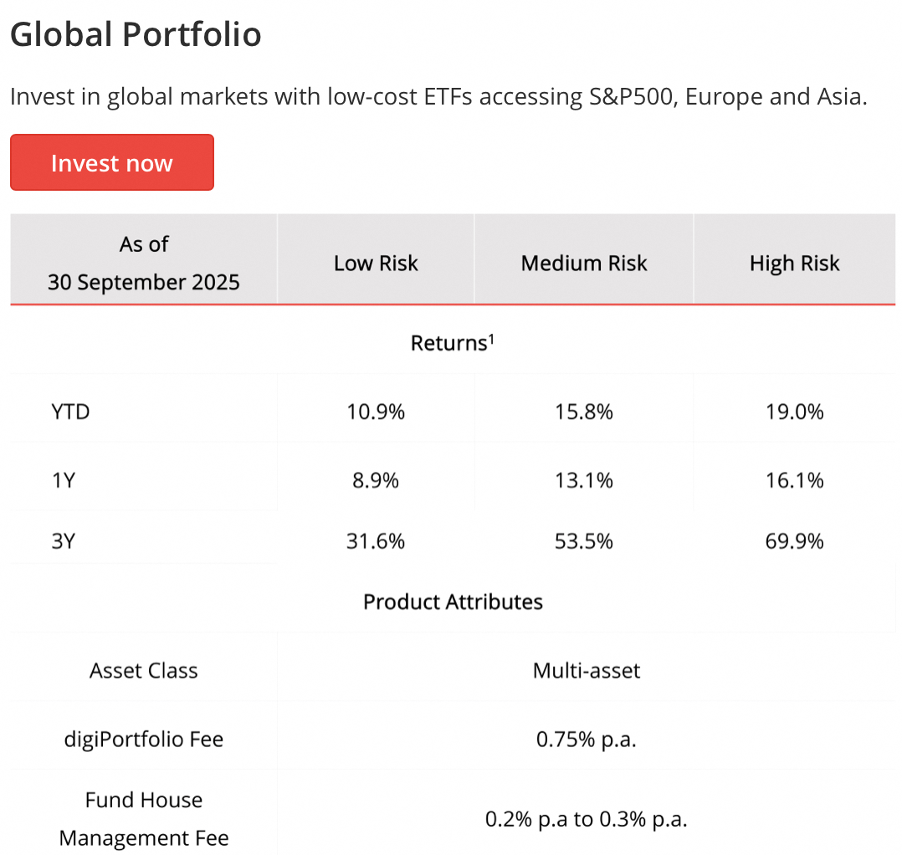

Those looking for some direction can rely on a curated list of strong and diversified funds by the DBS Chief Investment Office (CIO).

For example, you can start with a broadly diversified portfolio, which gives you exposure across the S&P 500, Europe and Asia. DBS’ Chief Investment Office has put together a Global Portfolio of ETFs with 3 different Risk Levels that investors can start investing in from as little as S$1,000.

As you can see below, taking more risk tends to deliver better returns over the longer term. However, you need to understand that it also comes with higher risks.

What’s really useful is that DBS has transparently depicted the fees that investors will incur at both the fund level and the fees that DBS charges. This goes a long way to ensuring you do not overpay for fees.

Source: DBS CIO Insights Funds

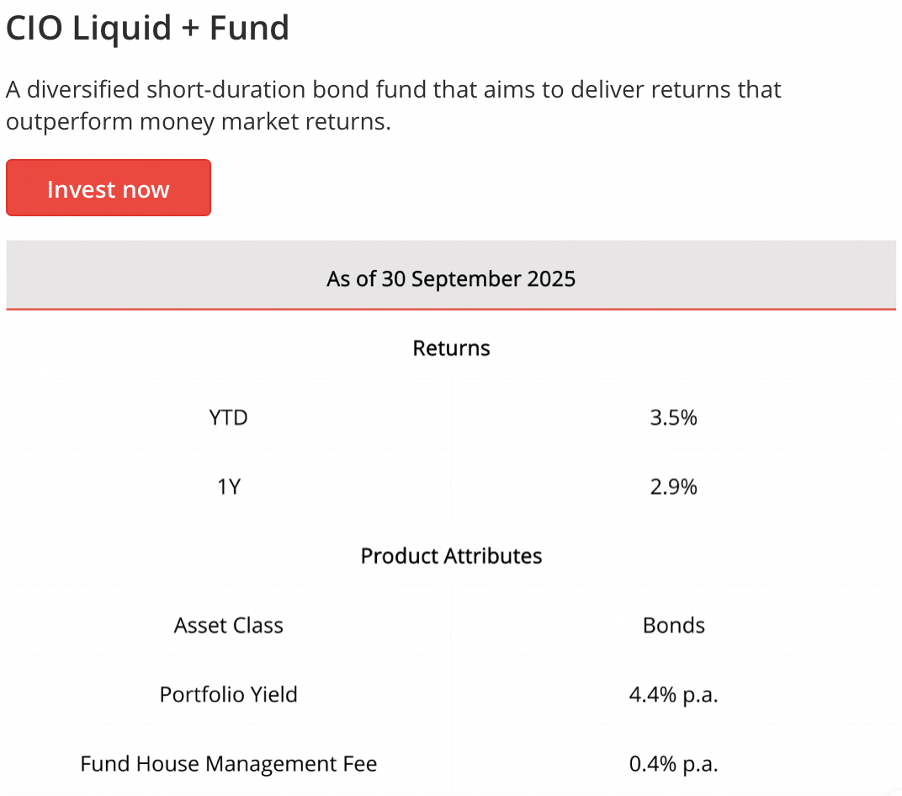

Investors with a shorter horizon may prefer to be more conservative, with higher allocation to lower-volatility investments such as fixed or stable income investments.

Such investors can consider a fund such as the CIO Liquid+ Fund, which gives you exposure to a mix of government and corporate bonds. This allows you to earn a better yield compared to keeping cash or buying T-bills, while still benefiting from high liquidity and mitigating single credit exposure.

Source: DBS CIO Insights Funds

You can rest assured that when you need your money, funds can be withdrawn quickly and you can expect a return that is higher than what money market funds provide.

#2 How Much Risk Can I Really Afford To Take?

Many investors overestimate their comfort with risk. That is, until the markets test your resolve in a sharp crash. By that time, though, it is too late to reconsider your risk appetite.

One simple question you can ask yourself is: if the market dropped 20% to 30% in the next few months, would you be ok with that? This is not a hypothetical question. The broad stock markets have fallen around 25% on at least three occasions in the past five years: 1) over 23% crash following US President Donald Trump announcing large import tariffs in April 2025; 2) over 27% in early 2022 amid rising interest rates and inflation fears; and 3) during the pandemic-led crash in early 2020.

Your answer here should guide how much of your portfolio you place into higher-volatility equities vs lower-volatility or income-generating assets.

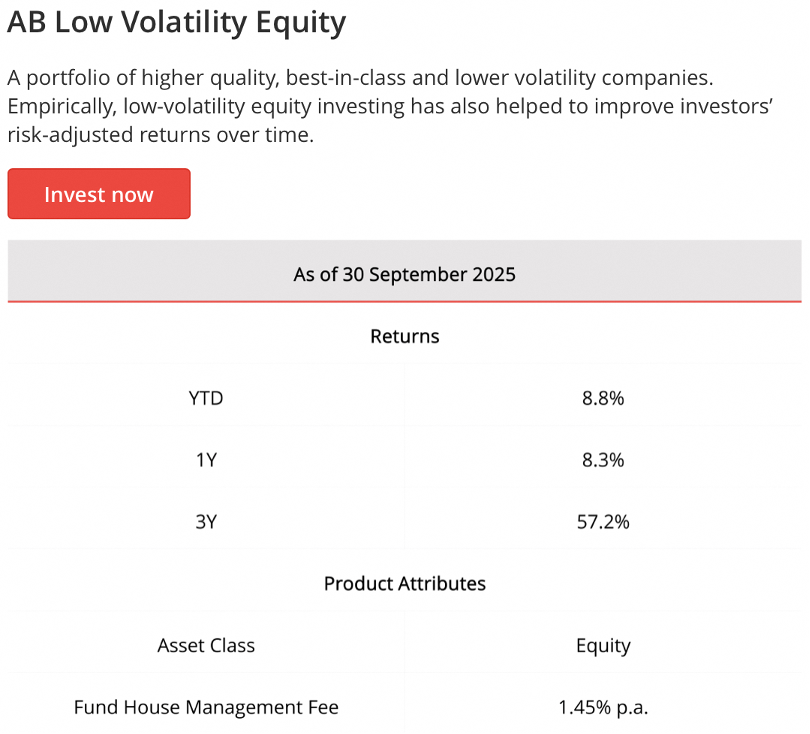

For example, if you prefer lower volatility but have a relatively long investment horizon, a fund such as the AB Low Volatility Equity may be appealing. You gain exposure to high-quality, established companies selected for their relative stability – helping smooth out equity volatility while still offering growth potential.

Source: DBS CIO Insights Funds

Alternatively, you may prefer to invest in a portfolio that gives you regular income. This way, even if the market dips, you have the stability of a regular income while waiting for the recovery.

In the interim, you can continue to spend the income if you need it or choose to reinvest it at more attractive valuations.

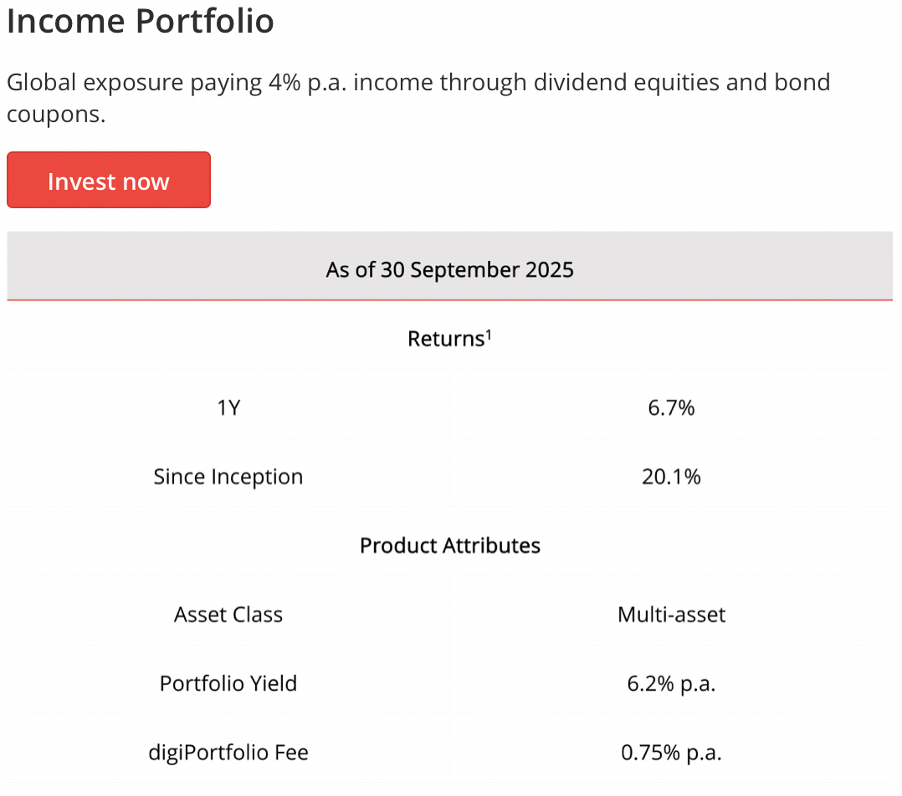

Referring again to DBS CIO Insights Funds, you can invest in Income Portfolio. As you can see, the fund has delivered a 1-year return of 6.7% – and most of it would have been in the form of dividends from its equity holdings and bond coupons. Typically, companies that are able to pay a regular income even during market downturns tend to be more defensive.

Source: DBS CIO Insights Funds

#3 Can My Existing Portfolio Weather A Market Crash?

Volatility is not just about price fluctuations, but also whether your portfolio is can survive a sharp market crash without derailing your overall financial plan.

If your portfolio is over-concentrated in equities, a single downturn could wipe out years of gains. On the other hand, a portfolio made up entirely of fixed income would not have given you the upside that a bull market can deliver.

You need to decide how much allocation you want to fixed income assets, stable income and low volatility assets, and global equities. Depending on the market cycle, certain exposure will hold up better during downturns, while others that struggle in a crash will outperform in a bull run.

Using a “core-satellite” approach, where you invest in a core of diversified, defensive or income-producing assets, plus satellites of smaller, more speculative exposure. This is also a strategy emphasised by the DBS CIO when building well-rounded portfolios. The core offers resilience, while the satellite allows for upside.

Taken together in a portfolio, investments in a short-duration bond fund like the DBS CIO Liquid+ Fund may serve as one part of your “core” holding – offering better returns than cash or T-bills, with relatively low volatility.

This may be supplemented with other “core” holdings, such as the AB Low Volatility Equity Fund – which may comprise more defensive equities that will still hold up well in downturns.

In your satellite portfolio, typically a much smaller component of your overall portfolio, you can afford to be more speculative – investing in trends you believe in.

For example, you may wish to gain exposure to gold. Apart from being a traditionally safe haven asset – to invest in during times of higher market uncertainty – gold has also done tremendously well in recent years.

Source: DBS CIO Insights Funds

You may also choose to go beyond the DBS CIO Insights Funds ecosystem to build your satellite portfolio, and you can explore ETFs and even single-counter investments. For instance, through DBS Vickers, you can invest in 7 stock markets, including in Singapore, US, Hong Kong, UK, Australia and Japan.

#4 What Will I Do In A Market Downturn?

Having a well-defined plan ahead of time, rather than reacting emotionally, is one of the most important hallmarks of disciplined investing.

Will you buy more when markets fall (i.e. “buy the dip”)? Or will you rebalance to assets which have fallen the most? Or, will you simply stay the course – investing the same way?

For long-term investors, downturns may offer opportunities to accumulate high quality assets at more attractive prices. For more experienced investors, you may even consider tweaking your asset allocations.

If you’re unsure, having the assurance of professionally managed portfolios can help – especially for those who don’t have time or ability to monitor markets. You can fall back on the experience of the DBS Chief Investment Office, which puts it quite aptly, “smart investing is about making decisions for the long run, not a quick fix”.

The DBS CIO Insights Funds are curated based on macroeconomic outlook, valuations, and momentum – combining top-down and bottom-up factors, including growth, inflation, earnings, credit spreads, fund flows, volatility, and other catalysts. This reduces the pressure on individual investors to react to every headline.

Your Portfolio Should Be Personal

Markets may trend higher in the long-term but they rarely move up in a straight line. Periods of volatility can stretch weeks, months or even years, as history has shown.

Given that the markets are becoming more volatile, you can turn price swings into opportunities – buying quality assets when prices are lower. You can gain access to all the DBS CIO Insights Funds covered earlier, and more, via the digiWealth tab on your DBS digibank app.

With DBS digiWealth, long-term investors can add the flagship Global Portfolio, which has achieved an annualised return of 10% to 15% over the past year. Those seeking steadier cash flows can lean on the Income Fund, paying a 6.2% yield while you wait for markets to recover. You can incorporate gold into your portfolio, which has historically cushioned against large market drawdowns.

Moreover, using DBS’ digiWealth, you can gain a bird’s eye view across your entire finances, from savings to investments and even your protection and loans in one place.

Investing with one of the most recognisable banking names in Singapore can also help different parts of your finances work harder. For example, investments on digiWealth is counted towards getting even higher returns (of up to 4.1% p.a.) on savings in your DBS Multiplier Account.

Those who need a better understanding of how your overall finances can work in greater harmony can leverage on DBS Wealth Planning Managers to provide more personalise guidance.

Combined with professionally managed and research-driven DBS CIO Insights Funds, you can also invest in them with a relatively small sum – ranging from S$100 to S$1,000 a month.

For many retail investors, this offers a more convenient and less stressful way to build a diversified and resilient portfolio. What’s more, with the S$68 digiPortfolio bonus credits promotion on CIO Insights Funds running throughout 2026, starting your investment journey with DBS digiWealth can be even more rewarding now. T&Cs apply, subject to changes.

Alternatively, learn more about the DBS CIO Insights Funds here

Disclaimer

The article herein is published by DollarsAndSense and is for general information only and should not be relied upon as financial advice. This article may not be reproduced, reposted or communicated to any other person without the prior written permission from DollarsAndSense.

This information does not take into account the specific investment objectives, financial situation or needs of any particular person. Before entering into any transaction involving any product mentioned in this information, where applicable, you should seek advice from a financial adviser regarding its suitability for your own objectives and circumstances. If you choose not to do so, you should make an independent assessment and do your own due diligence on the product.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

The information herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.

DBS Bank, its related companies, their directors and/ or employees may have positions or other interests in, and may effect transactions in the product(s) mentioned in this article. DBS Bank may have alliances or other contractual agreements with the provider(s) of the product(s) to market or sell its product(s). Where DBS Bank’s related company is the product provider, such related company may be receiving fees from investors. In addition, DBS Bank, its related companies, their directors and/ or employees may also perform or seek to perform broking, investment banking and other banking or financial services for these product providers.

All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment.

Any past performance, prediction, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment.

Bonds and Fixed Income

StashAway Income Portfolio: How You Can Earn 4.6%* Dividends From Your Investments Each Year