Bonuses are often the largest lump-sum payment people receive in a year. For many, there’s a sense of urgency that something needs to be done with the money – whether it is rewarding yourself through a luxury purchase or investing to grow wealth.

While this instinct is understandable, rushed decisions usually increase the risk of making suboptimal moves. Taking time to plan more carefully may lead to better financial outcomes over the long term.

The challenge, however, is that taking the time to decide comes with a perceived opportunity cost. Leaving your money in a savings account earning 0.05% p.a. makes it feel like the clock is ticking from the moment your bonus lands in your bank account. The longer you need to make a prudent investment decision, the more it feels like you’re “losing” money.

Read Also: How Parents Can Start Building A University Education Fund For Your Young Children

How Money Market Funds Fit Into Your Investing Strategy

In today’s environment of low-cost brokerages with comprehensive investment solutions, there’s an in-between solution. Money market funds (MMFs) allow you to put your money to work immediately, while having the time and flexibility to make better long-term investment decisions.

Broadly, money market funds invest in short-term debt issued by creditworthy governments, banks and large multinational companies. By spreading exposure across many such instruments, the money market fund aims to provide steady returns while keeping your capital relatively stable.

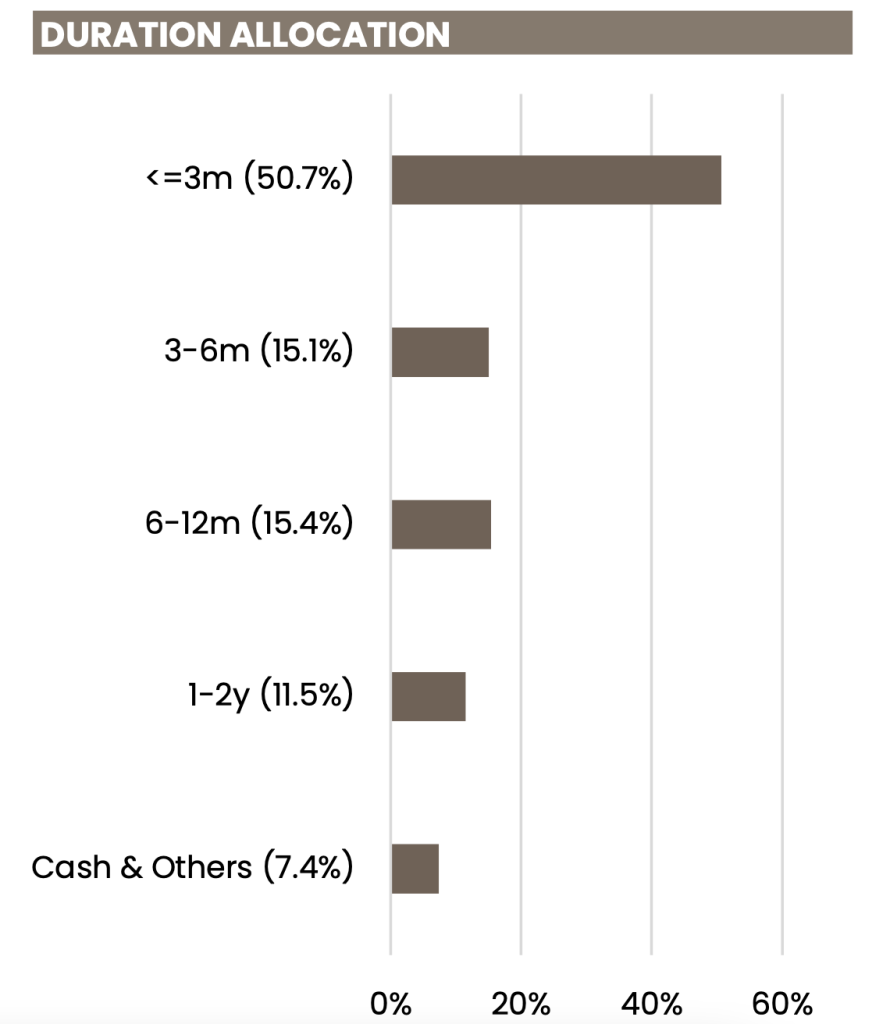

These debt securities typically mature in about a year. For example, the Maybank Money Market Fund Class A (Acc) SGD has a weighted duration of 0.42 years, or about 5 months. Nevertheless, you can also see that while its overall portfolio duration low, it also owns some debt securities that will mature in 1 to 2 years.

Source: Maybank Money Market Fund

The Maybank Money Market Fund is also designed to have a lower risk profile, investing in short-term debt securities with a weighted credit rating of AA. Its top holdings include the Monetary Authority of Singapore (MAS), the Export-Import Bank of Korea, and HDB.

In the past year, it has delivered a competitive return of 1.98%, which is higher than the current Singapore Government 6-month T-bill – paying 1.39% p.a.

Why Parking Your Bonus In Money Market Funds Makes Sense (Instead Of Investing Immediately)

When you receive a lump sum bonus, you should have more freedom to choose how you want to use it. After all, bonuses are one-off payments and typically not relied upon in your monthly household budget.

There’s no harm in spending some of it, but from a financial planning perspective, it makes sense to invest most of it for the long-term.

That said, forcing yourself to invest immediately, simply because the money is in your bank account, can lead to poor outcomes. You may still be deciding how the bonus fits into your broader financial goals, or just awaiting greater clarity on market conditions.

Placing your bonus into a money market fund first gives you breathing room. Your money starts earning a reasonable return, while you plan your next financial move. Investment Platforms like uSMART provide access to money market funds, such as the Maybank Money Market Fund, used in the example above.

When you are ready to deploy your cash into longer-term investments, you can liquidate the fund by the next business day (T+1), without feeling that you have missed out in the meantime.

This same logic applies beyond bonuses. Money market funds can also be useful for other excess cash you may have, such as emergency funds, savings for upcoming expenses like a renovation or holiday, or when you’ve liquidated an investment and are considering your next step.

In all of these cases, accessibility matters just as much as earning a reasonable return. From this perspective, money market funds are not an alternative to investing, but a complementary tool that helps you invest more thoughtfully.

Another practical benefit is for investors who plan to deploy your excess cash over several months through dollar-cost averaging (DCA) rather than all at once. You can continue to keep the bulk of your funds in the money market fund, and periodically liquidate smaller portions to invest according to your long-term investment plan.

Why It’s Worth Considering uSMART To Park Your Excess Cash

Money market funds can help you bridge the gap between intention and action, giving you the opportunity to move forward without incurring the full opportunity cost of waiting (and considering your next financial moves).

Like many other brokerages, uSMART offers access to high-quality money market funds without sales charges or lock-in periods.

What makes it particularly compelling right now is uSMART’s current Money Market Fund promotion. The promotion offers an extremely attractive headline return of up to 8.88% p.a. for 30 days, which meaningfully boosts your short-term returns.

Learn more about uSMART’s Maybank Money Market Fund promotion

As you may know, money market funds do not generate anywhere close to 8.88% p.a. in the current interest rate environment. In this promotion, uSMART tops up the difference between the promotional rate of 8.88% p.a. and the actual return of the underlying Maybank Money Market Fund.

This promotion lasts from 1 January 2026 to 31 March 2026, for new customers and existing customers with no prior deposits only. This makes the “parking” phase feel like a good investment decision.

Instead of being resigned to an opportunity cost where you earn 0 returns while making a financial decision, you can now be rewarded!

For users who value guidance or reassurance, be it with the money market fund investment or what to do next with your excess cash, uSMART offers an option to meet their Relationship Manager at one of its two branches at Robinson Road or Somerset.

This in-person consultation allows investors to better understand how uSMART’s comprehensive solutions can fit into your overall financial plan.

Read Also: From Online To Offline: Why Online Brokerages Are Making A Comeback To Open Physical Shops

Disclaimer

This advertisement has not been reviewed by the Monetary Authority of Singapore. The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. This advertisement does not constitute a recommendation, an offer or solicitation to buy or sell the investment product or participate in any featured strategy mentioned. Past performance is not indicative of future results. Any diagrams charts, or graphics shown are for illustration purposes only and do not represent actual or future performance.

While we take all reasonable efforts to ensure the accuracy and completeness of the information, uSMART Securities (Singapore) Pte Ltd accepts no liability whatsoever with respect to the use of this document or its contents. Investors should conduct independent research and seek advice to determine whether an investment is suitable for their individual circumstances.

This article contains affiliate links. DollarsAndSense may receive a share of the revenue from your sign-ups. You can refer to our editorial policy here.