This article was first published by Cheerfulegg.

Buying a house is like sex: Everyone says they know a lot about it, but few people ever want to get into the specifics.

For example, your parents and financial bloggers (who are even more annoying than your parents) will tell you to “buy a house within your means!”

Okayyyyyy. That’s like saying, “Twister fries are delicious”. Everyone agrees, but what does that even mean, specifically?

The personal finance world is filled with this sort of generic “advice” that’s actually not useful to us at all. So as a first-time buyer, you might end up doing one of two things:

- Apply for every single BTO launch, and leave the eventual price you pay up to luck

- Approach a property agent who’s incentivised to convince you to buy something you can’t afford

Neither are great approaches. Because, well, IT’S THE BIGGEST PURCHASE YOU’LL MAKE IN YOUR LIFE. Why the heck would you not spend 15 minutes to work out the numbers first?

Your First House Is Not An Investment

Some people will be like, “Well, it doesn’t matter what price I pay, because it’s an investment.”

I’ve said it before and I’ll say it again: Your first house is NOT an investment.

An investment is something that you 1) put money into, 2) eventually sell and 3) get to enjoy the proceeds.

Housing may fit the first 2 criteria, but not the third. You see, when you sell your first house, you’ll still have to use the proceeds to buy another house. (Unless you don’t mind living under a bridge. If that floats your boat, I’d recommend the Esplanade one – it’s really spacious and there’s free music on weekends).

Like I alluded to in my previous post, few people “trade down”. Most people will realistically never move into a $500,000 HDB flat after selling their $1,000,000 condo. Instead, they’ll start looking at landed property and end up forking out even more money.

Therefore, it’s far better to think of your first house as an expense, rather than an investment.

It’s like buying a new shirt – Buy one that suits your lifestyle and makes you comfortable. It may not necessarily be the cheapest, but it’s something that you’ll enjoy using. Nobody ever said, “Hey, why don’t I buy this $4,000 Armani shirt? It’s an investment!” (try selling that on Carousell!)

Yet, thousands of people continue to apply this warped principle to their housing decisions every month.

Your first house is an expense – a large one.

Your First House Is More Expensive Than You Think

Let’s say that you bought a house for $500,000. 25 years later, it doubles in value and you sell it for $1 million buckeroos. Therefore, you made a 100% return. Right?

Let’s say that you bought a house for $500,000. 25 years later, it doubles in value and you sell it for $1 million buckeroos. Therefore, you made a 100% return. Right?

WRONG.

When I bought my house, I was blown away by the number of upfront costs I had to pay: Commissions, stamp duty, conveyance fees, application fees, etc. Not to mention the renovation, furniture, plumbing, and electrical costs. Then there’s all the recurring costs: Your interest payments, taxes, conservancy charges, utilities, etc.

Whew. I got tired just from writing that paragraph.

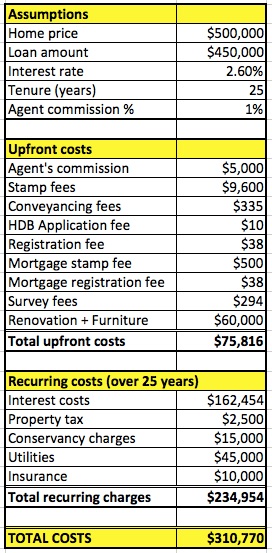

I ran the numbers for a hypothetical $500,000 house, with the following assumptions (I’ve only been a homeowner for 2 weeks, so let me know if they need to be tweaked):

- Price: $500,000

- 10% downpayment, 25 year loan at 2.6% interest rate

- Renovation + Furniture: $60,000

- Utilities: $150/month

- Property tax: $120 / year

- Conservancy charges: $50/month

- Insurance: $400 / year

*Sources: HDB, IRAS, Singapore Power, Qanvast

**Feel free to download the spreadsheet here if you wanna play around with the numbers

Adding it all up, the true costs of owning a $500K house amounts to an additional $310,770 over 25 years, or a whopping 62% of the purchase price. In other words, your “investment” has to rise by over 60% before it breaks even!

And that doesn’t even take into account the miscellaneous costs like maintenance, upgrading and the opportunity costs of the unearned interest on your CPF. D’oh!

Most people ignore these costs because it’s not sexy to think about them. It’s a lot more fun to talk about market conditions and how you’ll spend every morning sipping coffee on your balcony. (When you’re not late for work and when there’s no haze).

The 3-3-5 Rule

What if there was a way for us to objectively decide whether we can afford a particular house? It turns out, there is.

What if there was a way for us to objectively decide whether we can afford a particular house? It turns out, there is.

Vina Ip from PropertySoul.com has a great rule of thumb that she calls the 3-3-5 Rule:

- Rule 1 – 30% of property price: Your initial capital should be at least 30 percent of the property’s asking price

- Rule 2 – 1/3 of monthly salary:Your monthly mortgage payment should not exceed one-third of your monthly salary

- Rule 3 – 5 times of annual income:The purchase price of property cannot exceed five times of your annual income

Rule 1 relates to your savings – it ensures that you have enough cash to cover the upfront costs AND make a decent downpayment of at least 20%. I know that the government allows you to pay just 10%, but it’s usually prudent to pay above the minimum. That way, you manage your risk and won’t have to pay so much in interest.

Rules 2 and 3 relate to your income. They ensure that your mortgage payments are manageable, helping you guard against interest rates rises. Rule #3 also ensures that you’re not paying for a ridiculous price relative to your income.

These are just rules of thumb, but they make sense.

What I love about them is that they have nothing to do with speculative factors like “where the property market is going”. Remember: Your first house is not an investment. You shouldn’t be worrying about the “appreciation potential” or whatever B.S your agent tells you.

Two Buyers, Two Decisions

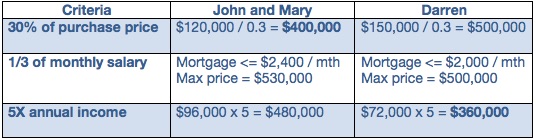

Let’s go through two quick examples, adapted from Vina’s article.

John and Mary are childhood sweethearts who’re getting married next year and want a place of their own to raise a family. They have combined savings of $120,000 (after setting aside their emergency funds) and a combined monthly salary of $8,000.

Darren is in his mid-30s, single, and wants a sweet bachelor pad where he can drink whisky without his parents nagging him to find a wife. He has savings of $150,000 and earns $6,000 a month.

Assuming they both take 25-year loans at 2.6% p.a, what’s the maximum price they should pay for their houses?

So John and Mary are constrained by their savings. As we saw earlier, they need to save enough for the crazy upfront costs, especially if they’re thinking of renovating. They don’t have enough of a savings buffer to justify getting a home above $400,000.

On the other hand, Darren has more savings, but he’s a single income earner so he’s more vulnerable to job risks. Therefore, his income constrains him to a $360,000 home.

Does this sound too conservative?

Nope, if you’re correctly viewing your housing decision as an expense, not an investment. Remember: You’re looking for an affordable place to live in. The fact that it MAY appreciate in the future is secondary.

In fact, in deciding my most recent HDB flat purchase, I made sure that the price comfortably fit all three criteria, leaving plenty of margin, just in case.

Get Specific

The key lessons I want you to take away from this are:

- Your first home is an expense, not an investment

- Get specific about the price you can afford

Things get a lot easier once you get specific. Having a concrete budget helps you to dramatically narrow down your search, and you’ll be less likely to be swayed by B.S arguments like “the market is bottoming out” or “this area is really undervalued”.

Most people aren’t willing to get this specific. After all, it’s a lot easier to fantasise about owning a dream home they can’t afford. But then again, most people don’t get rich.

What about you?

Image credits: Alan Cleaver, Henning Grap, Renee Rendler-Kaplan, Dave Dugdale