The HDB monthly household income ceiling is sometimes seen as a casual benchmark for how rich someone and their household is. If we exceed the income ceiling, we are seen as an upper-middle-class family in Singapore, fortunate (or unfortunate) as we no longer qualify to apply for public housing. Some would say that it’s a “good problem” to have if you exceed the HDB monthly household income ceiling.

Last reviewed in 2019, the HDB monthly household income ceiling is currently at $14,000 for families buying a new flat.

The $14,000 income ceiling also becomes the reference for other income ceiling criteria

- Executive Condominiums (ECs) have a $16,000 income ceiling. This is usually $2,000 more than the HDB income ceiling.

- CPF Housing Grant For Resale Flats has an income ceiling of $14,000.

- HDB housing loans also use the same income ceiling of $14,000.

- For singles buying a new2-room Flexi flat on their own, the income ceiling is $7,000. This is half of the income ceiling (currently $14,000)

- In the future when Prime Location Public Housing (PLH) flats are sold in the resale market, they can only be sold to buyers who do not exceed the income ceiling (currently $14,000)

The point here is that the $14,000 income ceiling is pretty significant as it doesn’t just affect first-time/second-time families looking to buy a BTO flat, but also other property policies that utilise the income ceiling to implement their policies.

How Much Have Wages Increased Since 2019?

A lot has changed since 2019. Beyond just the pandemic, Singaporeans have seen, for better or worse, our wages and cost of living increasing.

For example, median income from work, including employer CPF contributions, has risen from $4,563 in 2019 to $5,070 in 2022. For 2025, the figure stands at $5,775. At a gross level, this means median income has increased by 26% since 2019, when the HDB income ceiling was last reviewed.

If we look at the median salary for fresh graduates, the increment is just as significant. In 2019, the median salary for fresh graduates from Singapore’s four autonomous universities was $3,600. As of 2024, it’s $4,500, an increase of about 25%.

Another relevant reference point would be the median household income. In 2019, the median household market income among resident employed households (meaning households with at least one employed person) was $9,232 (inclusive of employer CPF contribution). As of 2025, it’s $12,446, an increase of about 34%.

The statistics above suggest that since 2019, income has increased by between 25% and 34%, depending on what you look at. But we were also curious to understand how many more households in Singapore have breached the $14,000 level since 2019.

The Number Of Households With Income Exceeding $14,000 Have Increased Since 2019

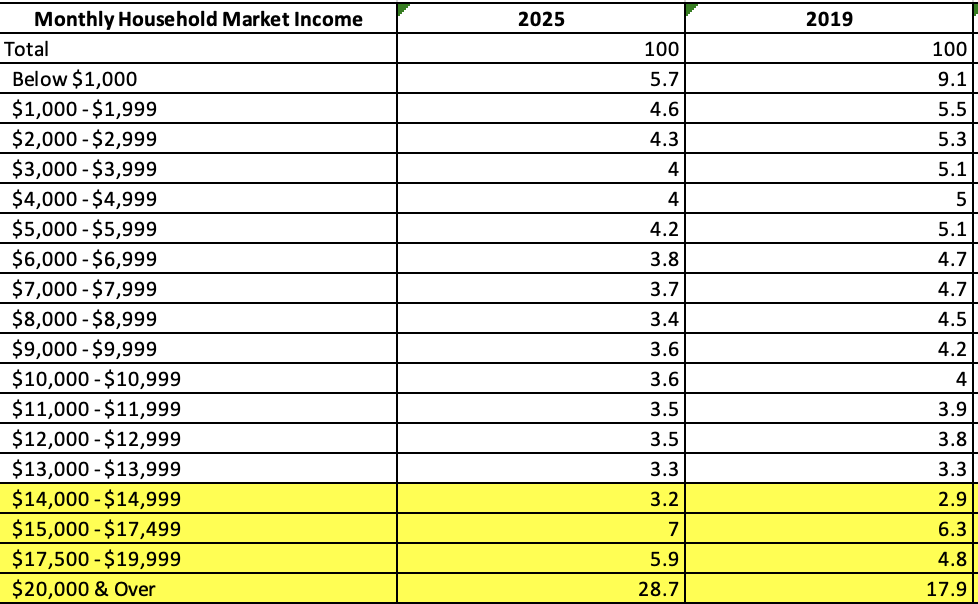

Using data from Singstats, we see that about 31.9% of resident households have a monthly household market income of $14,000 or more in 2019. As of 2025, this has increased to 44.8%, an increment of about 12.9% in seven years.

A point worth noting. Monthly Household Market Income, as Singstats now reports, includes both employment and non-employment income. So this includes income from non-employment sources, such as rental income, investments, and annuities, which do not count against the HDB income ceiling of $14,000. The HDB income ceiling only considers employment income.

The statistics above should come as no surprise. After all, with salaries increasing each year, whether due to higher productivity and/or wage inflation, it’s only logical that more Singapore households are now enjoying a household income that exceeds $14,000 a month.

As a side note, the average household size has declined from 3.16 in 2019 to 3.06 in 2025. This means not only that there are more households earning $14,000 or more in 2025 than in 2019, but this is achieved with fewer persons per household.

The Cost Of Resale Flats Have Also Increased Since 2019

The other impact is on households choosing to buy an HDB resale flat, especially if they are unable to qualify for a BTO flat and are priced out of the private property market.

In 4Q2019, the resale price index was 131.5. As of 4Q2025, it’s 203.6, an increase of about 54% in seven years.

Using the 4Q2019 median price for an HDB resale flat, we see that a 4-room flat in Punggol would cost $463,900. Assuming a household with a combined monthly income of $14,500 that is not eligible for an HDB BTO flat, the household would pay about 2.66 years of its annual income for the flat.

As of 4Q2025, a 4-room resale flat in Punggol has a median price of $683,500, an increase of about 47%. This is in line with the resale price index, and you would see similar observations across other HDB estates. It also means that, with a combined monthly income of $14,500 today, the household would be paying a price of 3.92 years of the household’s annual income for the flat.

Also note that even as a first-timer, the household will not receive any government grant as they exceed the $14,000 household income ceiling. So they are suffering a triple whammy – 1) unable to apply for a BTO flat, 2) ineligible for an HDB resale grant and 3) have to cope with a higher HDB resale price. And there are more such households today.

The bottom line here is that as wages and housing prices continue to rise, the proportion of families covered by the $14,000 household income ceiling will decrease. Those who exceed the income ceiling will also need to pay higher prices on the resale and private property market.

One possible alternative is to consider whether the income ceiling should be adjusted more regularly, especially when wages and housing prices are rising quickly. For example, should the income ceiling be set such that about 80% of households (in line with the HDB ownership proportion) will fall within the income ceiling and only 20% will exceed it?

Time would tell, but one thing that looks certain is that fewer families will fall within the $14,000 household income ceiling in the future.

Top photo by Moo Kar Ming, DollarsAndSense

This article was first written in 2023, and we have updated it with the latest statistics