Like most Asian children, I’ve been giving my parents $200 each every month. This is usually done through monthly bank transfers, but recently I made a change by giving my parents their allowance through CPF cash top-ups instead.

But money in the CPF is untouchable!

It took me a while to convince my parents about the merits of this move. But there are multiple benefits that eventually got me off my lazy butt to make this change.

Why contribute to their CPF?

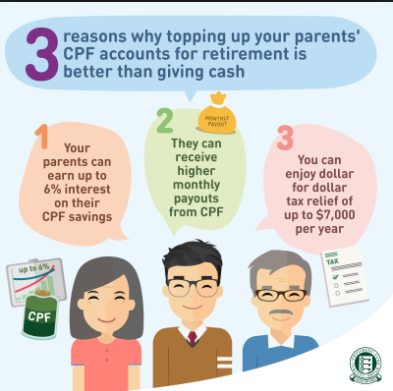

While some reasons are already listed in the graphic above, the main reasons that drove me to make this change were:

1. Tax reliefs

For each $10k rise in annual income, you also have to pay twice of your usual taxes.

When I was on my pathetic $2,500 salary in my first job, I only had to pay $200 in yearly income tax.

However, once your annual earnings hit $40k, that rises to $550 in taxes. Earning $50k means you’ll have to pay more than double of that i.e. $1,250. An additional $10k income raise also increases your tax by another 56% ($1,950). And for those who are lucky enough to earn $100k a year, prepare to pay $5,650 back to the government.

A legal way of hacking the tax system is to do voluntary cash contributions to your CPF account, or that of your parents / siblings / spouse / in-laws / grandparents. If you’re giving your parents anything less than $600, this hack makes a lot of sense because you’ll get exact tax relief i.e. dollar-to-dollar matching up to a maximum of $7,000 of taxable income. That’s like an added reward for being fillial!

2. You’re helping your parents to grow and protect their money

If your parents haven’t yet met the full retirement sum, every dollar you put in their Retirement Account earns up to 5% per annum in interest. This is far better than if you put the money in their bank accounts, which typically pay less than 1% per annum.

With scams (especially those targeted at the elderly) on the rise, I’ve been worried that my parents will become the next victim, and lose their hard-earned money to these scammers.

By putting the money in their CPF, it ensures that their funds are locked up and they cannot withdraw it to fall prey to a bogus investment scheme or some other scam. Their principal sum are protected while concurrently drawing a higher interest rates.

Furthermore, with CPF LIFE, your parents will receive fixed monthly payouts for the rest of their lives. This will ensure that they continue to receive “pocket money” to pay for their regular living expenses in retirement. I don’t have to worry that they will run out of cash one day.

3. CPF top-ups are infinitely more convenient than bank transfers or cash

Instead of having to remember to deposit money into my parents’ respective bank accounts each month, I can now simply transfer an entire year’s worth of “pocket money” for them in one go and let CPF dispense that to them via monthly payouts.

Doing it once instead of 12 times a year saves so much time and effort!

How to give your parents money through CPF?

The steps to do this are fairly simple:

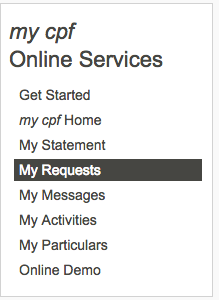

Step 1: Log into your CPF using your SingPass and click on “My Requests”.

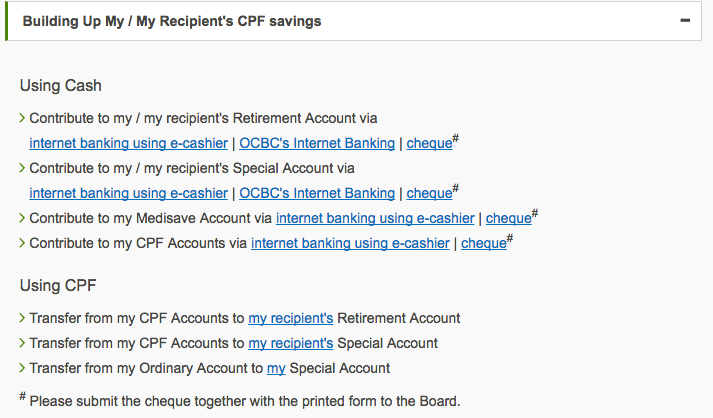

Step 2: Choose the below option and expand the field. Choose either e-cashier payment or OCBC Internet banking.

(Cheque is far more troublesome because you have to fill up a form)

Step 3: Choose whether you’re topping up RA, SA, etc.

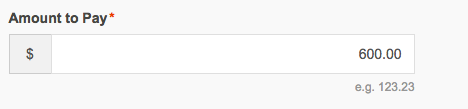

Step 4: Key in your parents’ NRIC number and relationship to you. Key in the amount you wish to transfer.

Step 5: Pay via e-cashier OR OCBC internet banking.

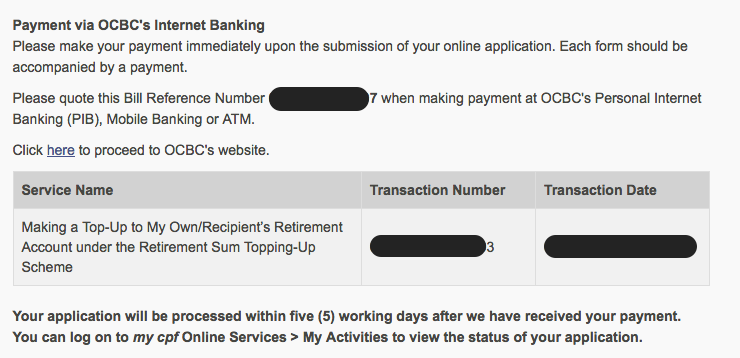

In case you’re confused by which transaction number to quote in your bill payment, please select the FIRST ONE i.e. the Bill Reference Number (not the one in the table!) I got confused by this when I first did the transfer initially, and had to test this to make sure I got it right.

If the $7000 tax rebate from this hack isn’t enough to bring your income tax down to the corresponding lower bracket, you can also consider donating to charity for further tax deductions. Donating $1,200 will result in an additional $3000 tax-deductible income for the year (2.5 times).

Remember that although your taxes won’t be due until April, you’ll have to finish these actions by 31 December to qualify for the following year rebate.

You can download the IRAS tax calculator here and estimate how much you’ll need to pay next year, and then see how much you’ll need to bring the final tax figure down to a sum that you’re comfortable with paying. Good luck!

With love,

Budget Babe

Budget Babe is an ordinary lady striving to achieve financial freedom in Singapore before the age of 45. She writes in order to empower fellow Singaporeans on taking charge of their own lives and finances, and to eventually break free from the competitive rat race.