This article was written in collaboration with the CPF Board. All views expressed in the article are the independent opinion of DollarsAndSense.sg

As someone who has been advocating active and prudent personal finance management, the irony of not having financial security that comes with a safe, corporate job was not lost on me when I decided to work full-time on DollarsAndSense in 2015.

Often, we take financial security for granted, until it’s no longer there. However, self-employed individuals (e.g. freelancers, entrepreneurs) understand the value of financial security. We can relate to the challenges of living a frugal lifestyle, knowing that we have no guarantees of a fixed monthly income.

Working on DollarsAndSense full-time meant facing many of the financial uncertainties commonly associated with entrepreneurship, or being self-employed. Here are some important money lessons that I’ve learnt over the past 26 months.

Accepting A Pay Cut

Whether you are quitting your full-time job to start a business or joining a different industry, accepting a pay cut is never easy to swallow.

The primary reason is we are already used to a certain lifestyle or are beholden to financial commitments that our current salaries can afford.

Besides, there is also a social stigma associated to being paid a lower salary. Regardless of the reasons, people somehow think you have moved backwards in your career and life, even if you are now doing something you truly love and are willing to take less money for it.

When I left my job in the corporate world to join DollarsAndSense, I took a 50% pay cut. Among local entrepreneurs, I was already one of the luckier few since most others I knew only took a very small allowance, if any at all, when they first started their business.

Continuing To Contribute Towards My CPF

One of the first financial decisions I had to make was deciding to continue contributing to my CPF account. As a self-employed person, only Medisave contributions were mandatory.

Rather than to contribute the minimum required, I felt that it was important for me to continue contributing to all three of my CPF accounts (Ordinary Account (OA), Special Account (SA) and Medisave Accounts (MA)) voluntarily, as per the standard CPF contribution rates that applies to most working Singaporeans.

Even though the contribution may not be a lot, I knew that money contributed today would become a substantial amount over the next 30 to 40 years due to the effect of compound interest. These were my options and thought process:

Option 1: Take a higher pay by not contributing to my own CPF. This will mean taking 100% of my salary as my take-home pay. Of course, I would have to make mandatory Medisave contributions after declaring my income in the following year.

Option 2: Continue contributing to CPF in the same way that a company would pay me if I were working elsewhere. That means taking home 80% of my salary, contributing 20% (employee’s contribution) to CPF, and having the company contribute another 17% (employer’s contribution) to CPF.

| Option 1 | Option 2 | |

| Take Home Salary | 100% | 80% |

| Employee’s Contribution | 0% | 20% |

| Employer’s Contribution | 0% | 17% |

While Option 1 would have given me more cash each month, I decided to go for Option 2 because I wanted to ensure that both my Special Account (SA) and Ordinary Account (OA) continue to receive regular contributions, and to benefit from the attractive interest rates these accounts give me.

Read Also: 4 Types Of CPF Members Who Should Make Voluntary Contributions To Their CPF Account

Very often, self-employed individuals do not make it a point to contribute to their CPF. While this gives them more cash on hand today, it may put their financial future at risk.

Source: CPF ‘R’ Chat – Starting Work

Source: CPF ‘R’ Chat – Starting Work

At age 30, an annual contribution of $1,000 to our Special Account will grow to $30,800 by age 50.

While it was tempting to receive more cash each month, I did not want a situation where I enter my 50s having very little money in my CPF accounts. There is actually one other benefit of contributing to my CPF. As a self-employed person, I get tax relief from making voluntary contributions to all 3 of my CPF accounts. This allows me to have a little more cash on hand due to less tax liability. In addition to that, if I make a cash top-up to my SA (and/or the SA/RA of my loved ones) under the Retirement Sum Topping-Up Scheme, I can enjoy a dollar-for-dollar tax relief of up to $14,000* per annum. CPF members.

NOT Investing Our Savings

Being married and having a child, any financial decisions I make doesn’t just affect me, but my family as well.

Prior to joining DollarsAndSense, my wife and I were able to survive on a single income. We made this a point, as we wanted to protect ourselves against the possibility of either one of us losing our jobs. This also meant we had the option for one of us to stop working for a period of time, without affecting our standard of living.

Since entrepreneurship was already a risky proposition, we decided on a more conservative approach towards accumulating savings, rather than to invest for higher returns.

There is no hard and fast rule to this, but, personally, we felt more comfortable knowing we had savings to fall back on if things didn’t work out.

Instead of building an emergency fund of six to nine months of average monthly expenditure, we aimed to maintain at least 12 months of it. The bulk of our savings is kept in a savings account paying high interest as well as in liquid government bonds.

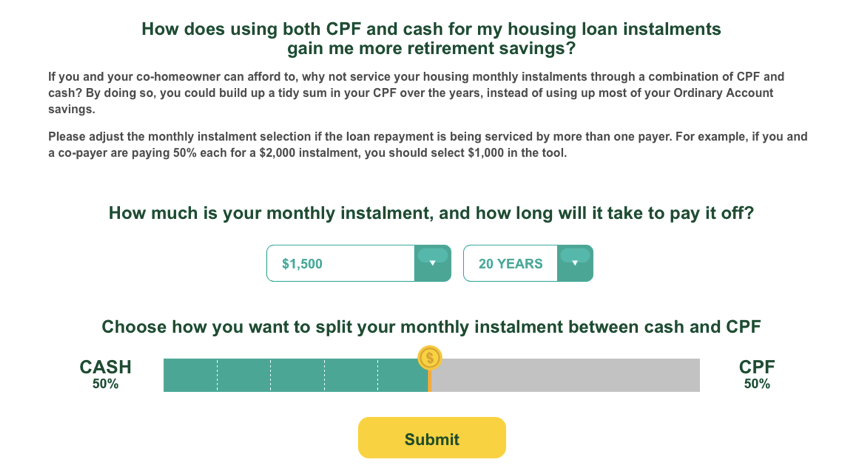

Paying For Our HDB Flat

When we got the keys to our Build-To-Order (BTO) flat in 2014, we made a conscious decision not to fully use our CPF Ordinary Account (CPFOA) for the monthly mortgage.

Unlike cash on hand, money in our CPFOA earns us an interest of up to 3.5% per annum. By not using the money, we were able to earn a reasonable risk-free return. To keep things simple, we only used monies from my CPFOA with the remaining monthly mortgage being serviced using cash.

Here’s an example that we computed from the CPF Big ‘R’ Chat microsite, illustrating how much more we can earn by not fully using our CPF balances on mortgage repayments.

Source: CPF ‘R’ Chat – Buying A Home

Source: CPF ‘R’ Chat – Buying A Home

Read Also: Why Singaporeans Should Stop Using Their CPF Money To Pay Their HDB Home Mortgage

Retirement Planning – Transferring Funds From CPFOA To CPFSA

Whether you are a freelancer working on various projects, or an entrepreneur looking to build a new product, it’s easy to be caught up in the hustle and bustle of life and to ignore planning for your retirement.

After getting married, my wife and I made it a point to do something for our retirement each year. In both 2015 and 2016, we did an annual transfer of $10,000 of unused CPFOA funds to our CPFSA in order to enjoy higher interest returns.

Here’s the amount we will be able to earn each year just by doing these transfers.

Source: CPF ‘R’ Chat – Planning Ahead

Source: CPF ‘R’ Chat – Planning Ahead

$26,600 – this is the amount we will have in 25 years by making a one-time transfer of $10,000 from our CPFOA to our CPFSA today. It is also approximately $8,060 more than we would have if we had left the money in our CPFOA.

There have been various discussions about the pros and cons of transferring OA funds to SA. Not everyone agrees with the approach, and some financial writers do not recommend it, since the transfer is irreversible.

Personally, I think the most important consideration is your own specific preferences. If you understand the various conditions for transferring funds from your OA to your SA, and believe it’s suitable for you, you can go ahead to take advantage of the higher interests provided by the SA. The key here is to understand how such decisions can impact your long-term financial plans, and the trade-off for every decision that you make.

Make Better Financial Decisions By Managing Your Cash Flow

Many people focus on earning a higher salary, or getting better returns from their investments. There is absolutely nothing wrong with this, however, they are not always within our control.

On the other hand, managing our cash flow by not spending beyond our means and allocating our monies efficiently by transferring and saving them in the right places can improve our long-term returns.

If you wish to know more about how you can make better CPF decisions in different stages of your life, check out the CPF Big “R” Chat microsite. Whether you are a self-employed individual or someone who works for a fixed and stable income, there are tools you can use to better optimise the funds in your CPF accounts, and how you can plan for your future retirement today.

Alternatively, if you want to talk to someone over CPF related decisions that you have, you can consider heading down to the upcoming CPF Retirement Planning Roadshow on 4 & 5 November at Compass One.

*Up to $7,000 per calendar year and capped at the current Full Retirement Sum (FRS). Cash top-ups beyond the current FRS will not be eligible for tax relief. In total, you can enjoy tax relief of up to $14,000 per calendar year if you make cash top-ups for yourself and your loved ones. The overall personal income tax relief cap of $80,000 applies for cash top-ups to CPF accounts. Terms and conditions apply.

Bonds and Fixed Income

StashAway Income Portfolio: How You Can Earn 4.6%* Dividends From Your Investments Each Year