This article was contributed to us by Willie Keng, CFA, Chief Editor at Dividend Titan.

I’m surprised. This “little-known” Singapore REIT is actually the landlord to one of the biggest government agencies in the UK — the Department for Work and Pensions (DWP).

And there’s something else that got me more interested.

Government agencies make good tenants. They have huge staff, hardly move out and more importantly, they don’t default on rent. That makes…

This Singapore REIT’s Rent Collection Safe And Reliable

At GBP310 million (S$552 million) market cap, Elite Commercial REIT (SGX: MXNU) is the first Singapore REIT focusing in UK offices. Elite Commercial REIT got listed before COVID broke out in Feb 2020.

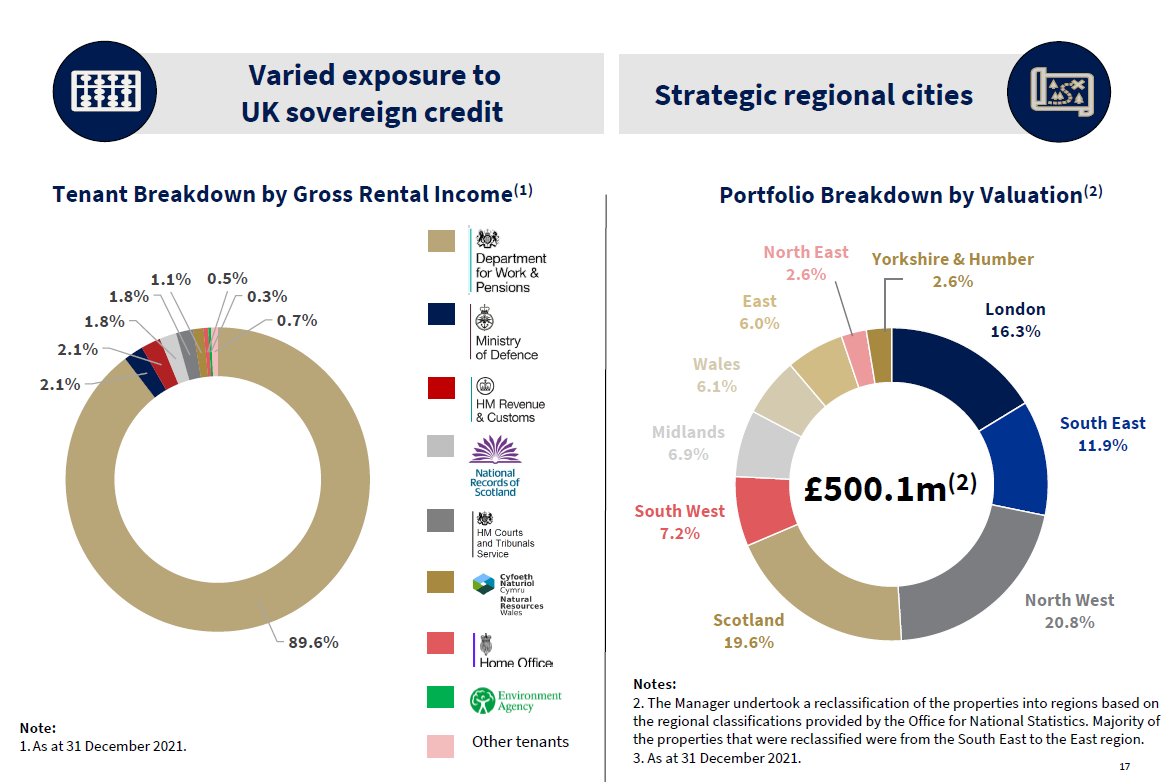

Today, this mid-sized REIT owns 155 properties — most of them leased out to government agencies.

And you know what? 97% of its assets are freehold.

In fact, 90% of Elite Commercial REIT’s revenues come from the biggest public service department in the UK — the DWP. This means 97 of this Singapore REIT’s properties are leased to the DWP.

The remaining 10% coming from other government agencies, including the Ministry of Defense, HM Revenue & Customs, National Records of Scotland and HM Courts and Tribunals Service.

Read Also: Complete Guide To Start Your REITs Investing Journey In Singapore

Source: Elite Commercial REIT 2021 Presentation

The thing is, since 1945, the UK operates as an extensive welfare state. The DWP is responsible for paying out welfare, pensions and child maintenance with over 23 million claimants.

Last year, DWP spent GBP 212 million in benefits. And has already planned for another GBP218 million of benefits this year. It’s a big responsibility.

Elite Commercial REIT has consistently collected all of its rent in advance since it got listed. And even during Brexit and COVID lockdowns. These rents are secured under leases to the Secretary of State — the central department for the UK government — for Housing, Communities and Local Government.

I cannot imagine a government agency defaulting on their rent, crisis or not.

Last year, Elite Commercial REIT has extended its leases to 2028. This strengthens rental income “visibility”.

And more crucially, 94% of the REIT’s rent agreement is pegged to UK’s CPI inflation rate. Rent review is every five years (with the next one in 2023). Management says rental will grow “between 7% to 8% per year”.

Inflation goes up. Rent goes up.

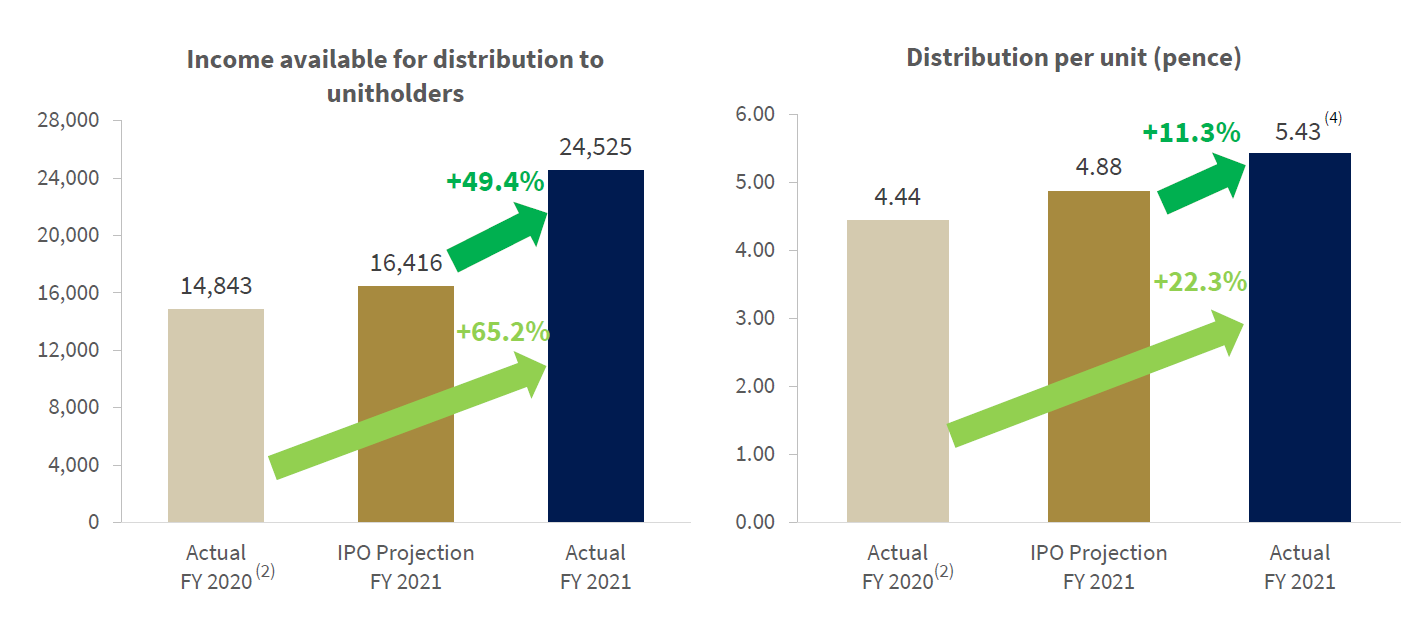

Elite Commercial REIT’s strong tenants form the bedrock of its high distribution. Last year, its distributable income grew 49% more than was projected during its IPO to S$24.5 million. This was also 65% higher than its distributable income in 2020 — mostly due to the 58 properties it bought back in March 2021.

Distributable income is what’s left for shareholders after paying for all operating costs, interest payment and taxes.

Source: Elite Commercial REIT 2021 Presentation

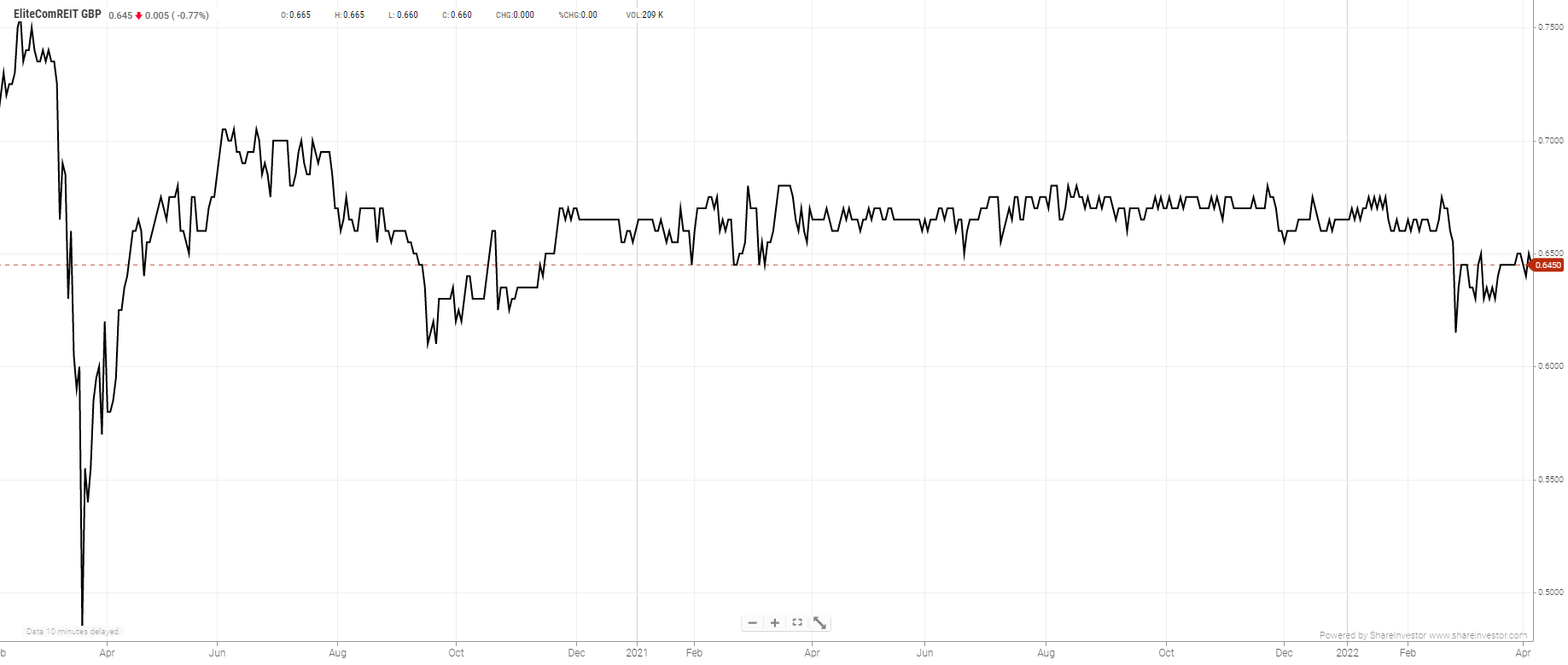

Since this Singapore REIT’s IPO, it has paid distributions of 4.44 pence per unit in 2020. Last year, it paid 5.26 pence per unit. Based on today’s shares of GBP0.64, that’s a full 8.1% dividend yield.

Source: ShareInvestor Webpro

Elite Commercial REIT’s Sponsors Definitely Aren’t Your First-Class Sponsors

Unlike Keppel, CapitaLand or Mapletree sponsors.

At first glance, I wasn’t impressed by them.

According to the company’s filings on sponsors:

Elite Partners Holdings Pte. Ltd. is the investment holding firm for Elite Partners Group, established to deliver lasting value for investors based on common interests, long-term perspectives and a disciplined approach. Backed by a team with proven expertise in private equity and REITs.

Ho Lee Group Pte. Ltd. has extensive experience across the real estate value chain, from general building construction to industrial and residential development since its inception in 1996. Ho Lee Group Pte. Ltd. was also one of the major sponsors of Viva Industrial Trust during its IPO in November 2013.

Sunway RE Capital Pte. Ltd. is a wholly-owned subsidiary of Sunway Berhad – one of Malaysia’s largest conglomerates with businesses in property development, property investment and REIT, construction, healthcare, hospitality, leisure, quarry, building materials, and trading and manufacturing.

Source: Elite Commercial REIT IPO Prospectus

What’s more is during the IPO, it was oversubscribed by 8.3 times. That’s tremendous support for a REIT with relatively unknown sponsors.

I’ve just two problems.

First, currency risk. It’s a fact GBP has weakened against the SGD over the years. For retail investors, this means…

There’s No Real Protection Against This

Well, but the way I see it, in a worst case event, even if GBP weakens by 50%, Elite Commercial REIT still pays you a 4% dividend yield (8% divide by 2). Not too bad.

The second problem is gearing. Elite Commercial REIT bought 58 properties last year. It loaded up debt, eventually raised their gearing from 34% to 42%.

Not many Singapore REITs dare to leverage so much.

Gearing ratio is total debt divide by total assets. The higher the gearing, the more leveraged the REIT. MAS limits gearing ratio to 50% for all Singapore REITs.

Look: the problem comes when Elite Commercial REIT wants to buy more properties. This means they have to massively raise more rights issue. This dilutes shareholders if the properties they buy in the future are either very expensive, or pays very low property yield.

Is 8% Dividends Worth Buying?

Of the two problems, I find currency risk to be more crucial. That’s because I can’t control how GBP moves against the SGD.

Then again, it’s rare to find a Singapore REIT that owns and operates UK’s biggest public service department as a tenant, alongside other UK government agencies. These leases are secured. And I don’t think a developed country’s government easily defaults on rent.

If you ask me, at 8% dividend yield — worst case to have its dividend yield halved — already more than compensates for the risks.

I think this is a pretty decent Singapore REIT worth buying.

Read Also: REITs Report Card 2022: How Singapore REITs Performed in 1st Quarter 2022

Willie Keng likes to daydream. Well, he’s a human being with emotions after all. But he also likes sharing insanely practical, investing tips and stock ideas. Twice a week. No fluff. Willie runs a financial blog called Dividend Titan that helps DIY investors grow their wealth safely. He’s a CFA charter holder.

Top image from Google Maps.

Bonds and Fixed Income

StashAway Income Portfolio: How You Can Earn 4.6%* Dividends From Your Investments Each Year

Branded Content

How To Build A Retirement Portfolio That Can Last A Lifetime