Healthcare financing is one of the most urgent challenges facing Singapore today. With medical costs climbing at rates well above general inflation, households are under pressure to balance affordability with adequate protection. On 7 April, the Global Asia Insurance Partnership (GAIP) released a study on sustainable private health insurance in Asia. It highlighted the risks of unchecked inflation and offered insights into how various countries can adapt amid inflation and affordability concerns.

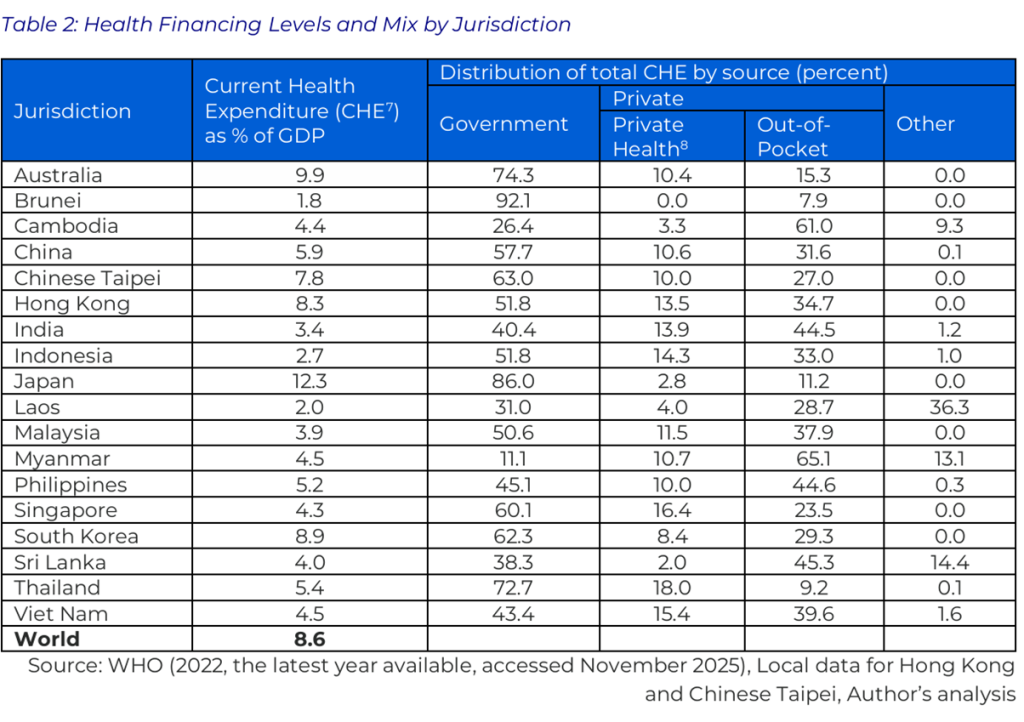

The study found that Singaporeans are paying about 23.5% of our current health expenditure out of pocket, with the government paying about 60%, and private health insurance, funded through premiums, paying about 16.4%.

This means that in Singapore, the burden of healthcare expenditure is relatively balanced across government spending, private health insurance and out-of-pocket payments.

Rising Medical Cost Inflation

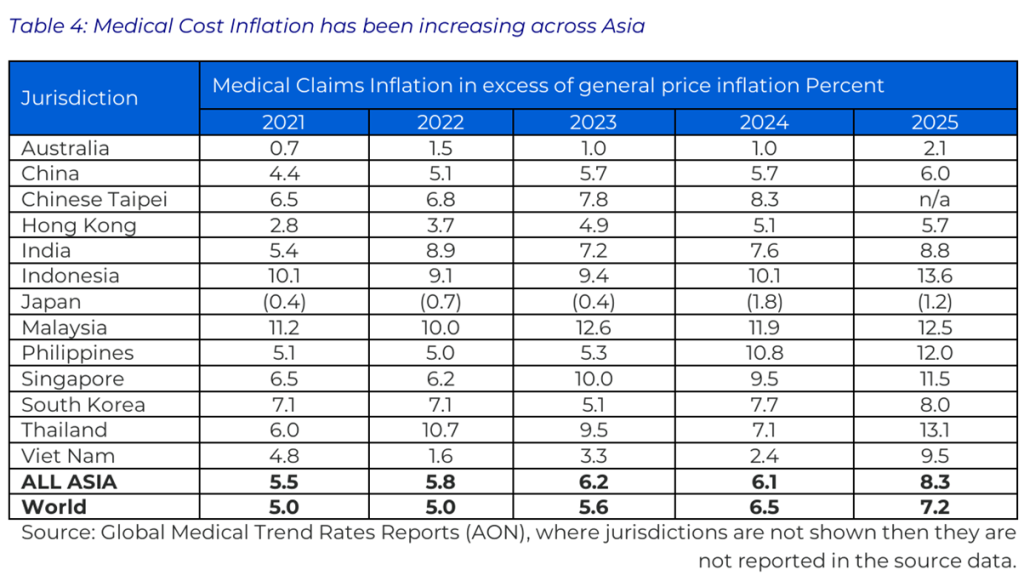

According to the study, medical cost inflation is outpacing wage growth and general price increases, creating a looming financing crisis across Asia. In Singapore, medical cost inflation has been increasing significantly between 2021 and 2025.

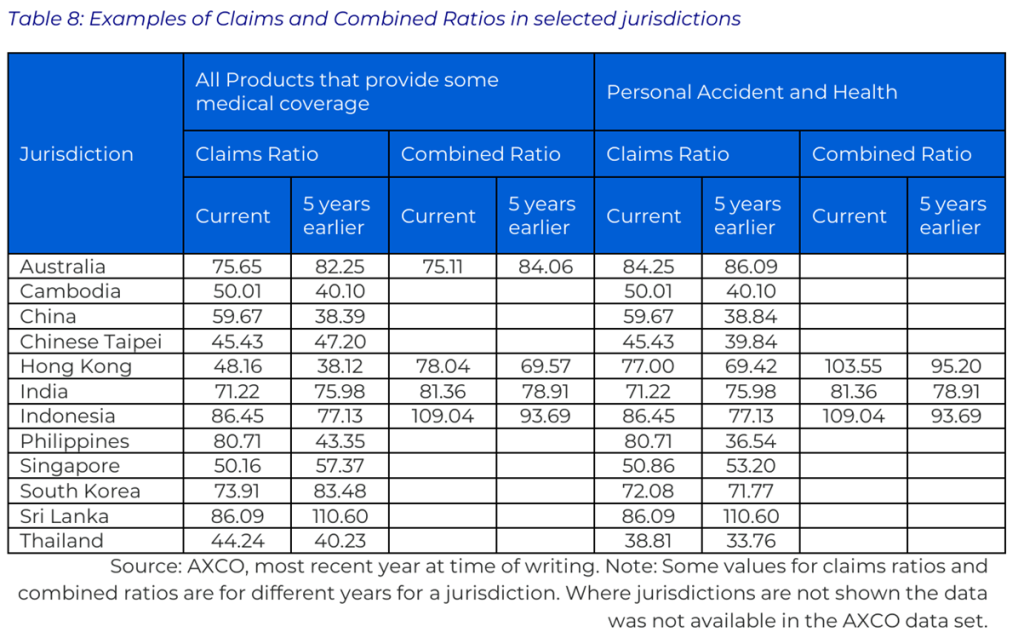

Medical cost inflation puts pressure on the system. As claim costs increase, health insurance can only remain sustainable if premiums increase consistently with the claims. Fortunately, despite Singapore’s high medical cost inflation, our claims ratio are relatively low, and are lower than they were 5 years earlier, in fact. Claims ratios above 80% are considered problematic, while ours are one of the lowest in the region at 50.16.

But this does not mean that no action is needed. Eventually, even in Singapore, we can expect Integrated Shield Plan premiums to rise, particularly for private hospital coverage. Households must prepare for higher costs and evaluate whether private hospital benefits are truly necessary, or if government hospital coverage provides sufficient protection.

The Health Protection Gap

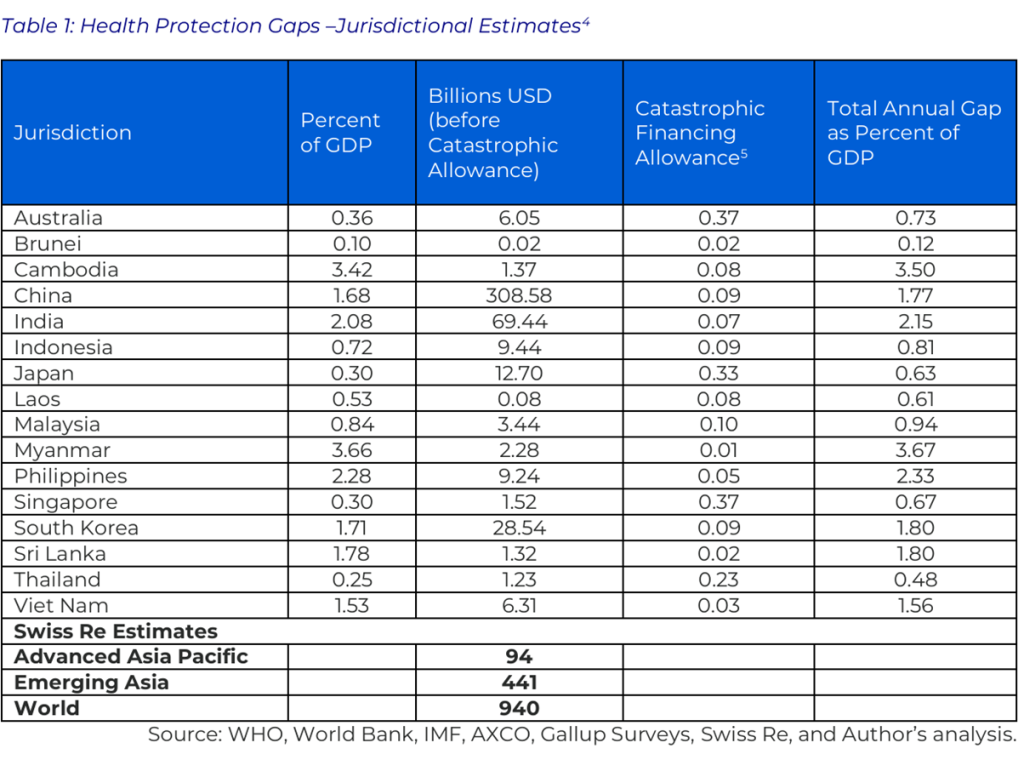

Singapore’s health protection gap, measured at 0.67% of GDP, about US$1.52 billion, is relatively small compared to other countries in the region but still significant.

This gap represents unmet healthcare needs and financial risks for households. Closing it requires expanding private insurance coverage while keeping premiums affordable. For families, this means regularly reviewing insurance portfolios to ensure they are not underinsured.

MediShield Life and Integrated Shield Plans

In Singapore, MediShield Life provides universal basic coverage for large hospital bills, while Integrated Shield Plans offer additional protection, especially for private hospital stays and specialist care. The sustainability of this system depends on balancing premiums, benefits, and risk-sharing. If premiums rise unchecked, households may be priced out. However, if they are capped too tightly, insurers may struggle to remain viable. For Singaporeans, the practical approach is to treat MediShield Life as the foundation and carefully assess whether private hospital coverage is worth the added expense.

Read Also: How Much Your MediShield Life Premiums Will Be Going Up From April 2025

Aligning Incentives Through Partnerships

The study emphasised that governments, insurers, and healthcare providers must align incentives to keep healthcare affordable. Co-insurance and deductibles can discourage overuse of services, while negotiated service costs can rein in hospital charges. Preventive health programs are also highlighted to reduce long-term claims.

The study also acknowledges the changes made in Singapore to help with the balance and stability of the healthcare system here, including increasing the claim limits, coverage and premiums of MediShield Life. This effectively shifts the higher costs from private Integrated Shield insurance plans back to the basic healthcare system.

For Singaporeans, this means expecting more emphasis on healthy living and preventive care in insurance design, with insurers likely to reward participation in wellness programs. One example of such an initiative is Healthier SG, which rewards taking proactive steps to manage health and prevent the onset of chronic diseases.

What This Means for Singapore Households

For everyday Singaporeans, these findings translate into practical steps. Rising premiums are inevitable, so households must weigh the trade-offs between public and private hospital coverage. MediShield Life remains a reliable safety net, but it does not cover everything. Policy changes may alter the landscape, making it important to stay updated on announcements from the Ministry of Health and CPF. Preventive health will increasingly be rewarded, offering both financial and personal benefits. And digital tools will make it easier to compare costs and coverage, empowering consumers to make smarter choices.

According to the study, sustainable health financing in Singapore will depend not only on government policy and insurer strategies but also on the decisions households make. By staying informed, reviewing coverage regularly, and embracing preventive health, Singaporeans can navigate rising costs while ensuring their families remain protected.