Today, the life expectancy of Singaporeans is 83.1 years, one of the highest in the world. As we live longer and healthier lives, many of us may have close to 20 years in retirement, from mid-60s to our mid-80s.

Working Only 40 Years To Fund 60 Years Of Our Lives

Many of us may find ourselves having to rely on 40 years of employment income, to fund nearly 60 years of our lives. All the while, we also have to continue to pay for our daily living expenses, buy a home, start a family, put our children through university and “live life” by indulging in entertainment through family holidays, going out for meals or buying stuff that we don’t absolutely need.

After paying for these expenses, we may not have a lot left to put towards our retirement nest egg. The government tries to solve part of this problem with the CPF LIFE, an annuity scheme which takes our accumulated contributions during our working years to pay us a monthly income in our retirement for as long as we live.

Read Also: [Beginners’ Guide] Understanding CPF LIFE And Your Monthly Payouts When You Retire In Singapore

On our part, we can’t just rely on CPF LIFE to fund our retirement. We should take active steps to save more and invest our money. Our investments will earn us a yearly return, that isn’t tied to our employment, and over time, may compound to a sizeable sum that will fund our retirement.

Why We Need To Reduce Our Investment Portfolio Risk As We Get Closer To Our Retirement

The first thing we need to note is that all investments are generally risky, and we earn a return because we’re taking on this risk. The higher the risk we take, the higher the returns we expect to be paid for taking that risk.

As we invest our funds throughout our working lives, it becomes important to reduce the amount of risk that we are taking on our investments. This is because an economic crisis right before our retirement or during our retirement can wipe out our ability to lead the lives we may be building towards.

Read Also: Why Retirement Planning Is For The Young, And How Singaporeans Can Start Planning For It Today

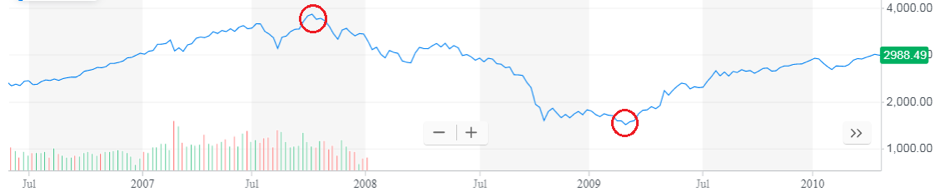

To understand the implications of an economic crisis, we can simply consider what would happen to our investments if an economic crisis, similar to the Global Financial Crisis in 2008, hits just when we are about to retire.

The chart below shows how the Straits Times Index (STI), comprising the 30 largest and most liquid stocks listed on the Singapore Exchange, fell from its high in October 2007 (3,822) to its post-Global Financial Crisis low in March 2009 (1,513). In the space of 1.5 years, the 30 strongest companies in Singapore, including DBS, OCBC, UOB, SingTel, Keppel Corp, Sembcorp Industries, City Developments, CapitaLand and many others, fell a combined 60.4%.

Imagine saving for 40 years for our retirement, and losing over 60% of it just when we need to start using it. Sure, as we can see in the chart, our investments may rebound close to its highs again within two years, but can we be sure that 1) would we still be in the market to enjoy those returns after experiencing those losses at a crucial time; and 2) the next financial crisis will see such a quick recovery period?

Even if we were still invested, we would have had to liquidate a few years of savings at drastically low prices because there wasn’t a choice – we would need to spend that money in our retirement.

This is why we need to understand the risk that we are taking on in our investments, and work towards reducing it as we near our retirement. Here are some ways we can reduce our investment risk as we near retirement.

# 1 Shifting A Larger Chunk Of Your Investments Into Bonds

This is one of the most common advice when it comes to reducing investment risks.

The logic behind doing this is to receive more stable and visible cashflows from our bond investments rather than leaving our money in stocks, which tend to be more volatile and deliver returns based on economic cycles.

Bonds pay the coupon rate that they promise regardless of how their business performs in the short-term. Of course, bonds can be very risky as well, especially if we do not know what we’re investing in.

Read Also: 5 Reasons You Need To Diversify Your Bond Investments

One way to achieve this is by incrementally shifting a percentage of our investment portfolio from stocks to bonds as we get older. This will gradually make our investment portfolio more resilient to economic cycles as we age, and by the time we are nearing retirement, we should have a larger percentage of our portfolio in bonds than stocks.

# 2 Investing In A Savings Plan Or Endowment Policy

Following along the lines of receiving more visible cashflows, we can also consider investing in savings plans or endowment policies that guarantee our capital and give us a return.

Many of the major insurance companies offer endowment policies that guarantee our capital. These plans usually require us keep our funds with them for the duration of the plan, which is usually 10 years or more. This means we need to plan ahead by shifting our investments into these plans close to 10 years before we retire.

Read Also: 6 Investments In Singapore That Provide Guaranteed Principal And Returns

From time to time, we would also see these insurance companies offer promotional shorter-term savings plans that guarantee both capital and offer a fixed rate of return.

# 3 Divesting Part Of Your Portfolio, And Topping Up Your CPF Retirement Account

A CPF Retirement Account (RA) will be opened for us when we turn 55. This account pays an interest rate of up to 6.0% per annum. Operated by the government, we can also consider it to be risk-free.

By selling off some of our riskier investments, and putting the cash into our Retirement Account, we are effectively increasing the CPF LIFE monthly payouts that we will receive once we retire. We are also solving the problem for how long our funds would last, as the CPF LIFE scheme provides a monthly payout for as long as we live.

Read Also: Retirement Planning In Singapore: What If You Live Beyond The Average Life Expectancy?

Note that our Retirement Account only pays 4.0% per annum. We are paid an extra interest of 1.0% on our first $60,000 balances and an additional extra interest of another 1.0% on our first $30,000 balances.

# 4 Buying An Annuity Plan

Annuities are able to make our retirement less risky by paying us a fixed sum of money each month. This is similar to the CPF LIFE scheme, administered by the government.

There are several different types of annuity plans offered by the different major insurance companies, and we need to understand their characteristics if we plan to buy them. For example, not all annuity plans provide a lifelong income and the income we eventually get from our annuity plans are dependent on guaranteed and non-guaranteed payouts.

Read Also: CPF LIFE Or Private Annuities Plan? Pros And Cons Of Choosing Either Options For Your Retirement

Understanding How Much You Need In Your Retirement

Perhaps the most important thing we need to understand is how much we would need in our retirement. And how, in the 40 years that we will be working, can we build up a nest egg that is able to pay for the 20 years or so that we will spend in retirement.

One easy place to start is to think of how much we would be spending each month in our retirement. While we may think we can cut back on certain things in our lives or even take on some work during our retirement years, it is usually easier said than done.

A common figure is to take 80% of your currently monthly expenses as the amount you will likely spend in your retirement. This accounts for any work-related expenses you may have, and could be slightly lower if you take away financial commitments you have to your children.

To ensure our savings can last for a longer period of time, we should try to be frugal and spend our money wisely. Any unnecessary money we spend today, we are taking away from our future-selfs who may need to spend it on an important purchase.

Read Also: Retirement Planning In Singapore: How Much Do I Need To Save And Invest To Retire At Age 55?

As we climb our career ladders and earn more money, limiting our lifestyle inflation will also help keep our monthly expenses low.

By spending a lower amount, we not only cultivate a frugal habit from young, but also have more funds to put towards growing our investments for our retirement.