This article is written in collaboration with Lion Global Investors. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, and is purely for informational purposes and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions and readers are encouraged to do their own due diligence. You can view our full editorial policy.

For centuries, gold has carried a certain mystique. Ancient civilisations prized it not just for beauty, but for what it represented: permanence, power and wealth. The Egyptian pharaohs famously adorned themselves with gold, confident that its value would outlast lifetimes. They were right.

Today, most of us no longer store our wealth in gold coins or bars. Instead, our net worth resides in asset classes such as stocks, bonds, real estate and cash savings. If we do own gold, whether in the form of jewellery or gold coins, it likely represents just a small portion of our total assets.

Yet here is the paradox. Even though gold is no longer central to modern money systems, its value has never been higher. In 2025, gold prices rose by more than 60%, pushing through multiple historic milestones along the way. Prices crossed the US$3,000 per ounce mark for the first time in March 2025, and by 31 December 2025, gold was trading above the US$4,000 level.

Source: https://goldprice.org/spot-gold.html as at 9 Jan 2026

The question here is, if gold is no longer widely used as money, why then, does it still perform so well?

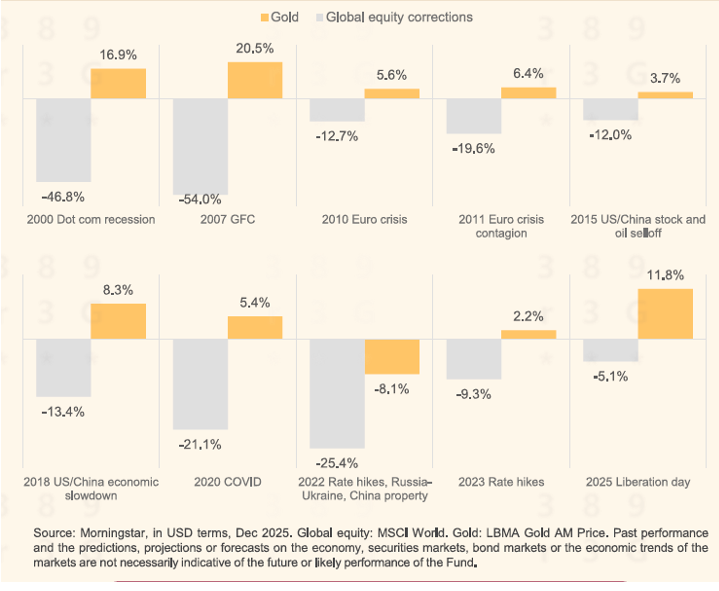

How Gold Prices Tend To Move During Crises

While gold no longer functions as a currency in daily life, it plays a quieter but equally important role in our investment portfolios.

The easiest way to think about the role of gold is that it acts as insurance for our wealth. This means it could be used as a hedge against market volatility, rising inflation and currency weakness. When stock-heavy portfolios suffer sharp swings, gold often moves differently, helping to cushion overall portfolio performance during turbulent times.

As seen in the table below, gold prices tend to perform well during periods of crises when the performance of global equity declines. For example, during the Global Financial Crisis in 2007, gold prices soared by about 20% while equities took a huge beating, declining by more than 50%. More recently in 2025 during Liberation Day (2 April 2025), global equity saw a decline of 5% while gold prices when up by around 12% during the same period.

This matters more than many people realise. Today, many investors are heavily exposed to equities through the stocks, ETFs, and unit trusts we invest in. This also means our portfolios can be significantly affected when equity markets decline. By holding some gold, we may help cushion the impact during such periods, as gold can act as a buffer against losses.

Of course, this does not mean gold prices will always rise. However, its defensive nature means it can play an important stabilising role in a portfolio, even in a world dominated by global equities and increasingly complex financial products.

Central Banks Are Buying Gold

Besides investors buying it as a hedge for their portfolios, another powerful force supporting gold prices today comes directly from central banks themselves.

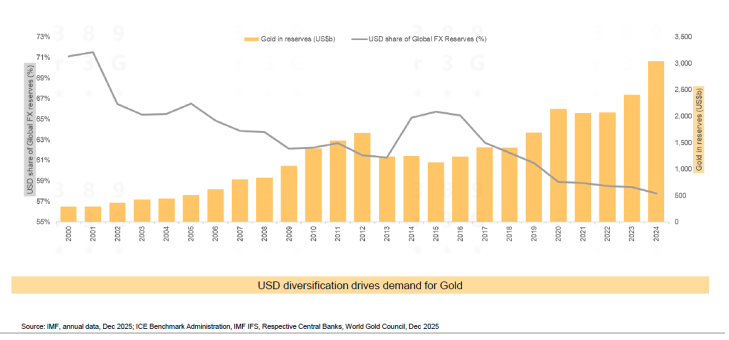

Over the past two decades, gold has steadily increased its share of global reserves. At the same time, the share of the US dollar in global reserves has declined from about 71% to roughly 58%. The value of gold held by central banks has increased more than ninefold since 2000.

This shift reflects diversification of reserves for governments around the world. Gold fits the role of diversifier perfectly. Gold is no one’s liability, is finite, cannot be printed, and holds value across market cycles.

When central banks themselves are buying gold to diversify away from the USD, they create long-term demand for gold. This supports prices and reinforces gold’s role as a strategic reserve asset, in addition to being a hedge for investment portfolios.

A Long-Term Store Of Value

Last but not least is gold’s ability to serve as a long-term store of value.

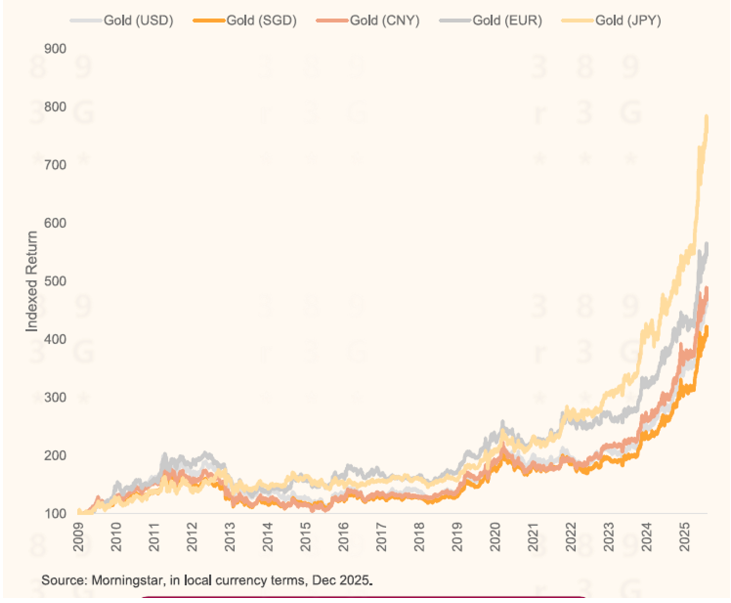

Unlike fiat currencies, which lose purchasing power over time due to inflation, gold has historically preserved its real value across decades. While cash left idle gradually buys less each year, gold has remained resilient, appreciating not only against the US dollar but also against many developed-market and Asian currencies.

This enduring safe-haven status is why gold is widely viewed as a hedge against weakening fiat currencies. In periods of economic uncertainty, policy shifts or financial crises, investors globally have turned to gold to safeguard wealth. Its role as both a safe haven and currency hedge helps preserve long-term purchasing power even as markets fluctuate.

For investors focused on long-term wealth preservation, gold complements their existing assets like equities, helping stabilise portfolios and to protect our wealth over time.

How Retail Investors Can Invest In Physical Gold

Despite its benefits, buying gold, especially physical gold, can be challenging for retail investors, particularly if the portfolio isn’t in the six- or seven-figure range. Since gold typically forms only a small allocation in a diversified portfolio, smaller investors may only require a few thousand dollars’ worth of exposure. At that level, it becomes difficult to acquire gold efficiently. Storage, security, insurance and logistics add unnecessary cost and hassle, overseas purchases introduce currency risk and complexity, and some gold products have opaque pricing or wide spreads that erode returns.

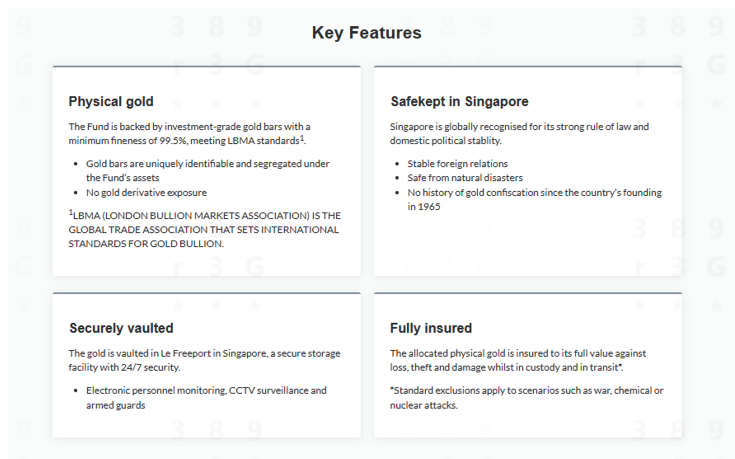

This is where the LionGlobal Singapore Physical Gold Fund can help. Backed by fully insured allocated investment-grade gold bars that are securely stored in Singapore, it provides investors with convenient and cost-efficient access to physical gold.

The LionGlobal Singapore Physical Gold Fund Is Designed For Retail Investors

Accessibility is a key advantage. The fund requires a minimum initial investment of S$1,000 or US$1,000, with subsequent investments from just S$100 or US$100. This makes it practical for investors who want to start small and build their gold exposure gradually. For instance, someone with a S$20,000 portfolio allocating 5% to gold can invest S$1,000 today, then top up progressively as their portfolio grows.

For even greater accessibility, the Maribank share class allows investors to start with as little as S$1 for both initial and subsequent investments via Mari Invest Gold available on Maribank Singapore App. This opens the door for those who prefer a micro-investing approach.

For investors who want exposure to gold without taking on additional currency risk, the SGD Hedged class helps stabilise returns in SGD terms so as to avoid FX risk impacting the gold investment.

The LionGlobal Singapore Physical Gold Fund suits investors who want the reassurance of allocated investment-grade physical gold that’s fully insured and professionally stored in Singapore, without needing to deal with the complexities of buying, holding and safeguarding bullion themselves.

Through the fund, investors can participate in gold price movements without worrying about storage, transport or safety. As Singapore’s first physical gold fund, it reinforces the country’s position as a trusted hub for gold investment, providing confidence to both local and international investors.

Source: Lion Global Investors, 12 Jan 2026

To be clear, gold does not generate dividends or rental income. Its purpose is to support portfolio resilience, helping investors manage uncertainty, smoothen volatility and preserve long-term value. In an increasingly interconnected world where shocks spread quickly, that role is becoming more relevant, not less.

The LionGlobal Singapore Physical Gold Fund makes this traditionally hard-to-access asset practical, transparent and manageable for retail investors. For those seeking portfolio protection without the hassle of owning physical gold directly, it offers a straightforward and timely solution. Sometimes, the oldest assets can have a strong place in modern portfolios—and gold remains one of them.

Ready to learn more or start investing?

Visit Lion Global Investors’ website for full details on the LionGlobal Singapore Physical Gold Fund, or buy conveniently through our distribution partners.

OCBC: https://go.ocbc.com/LGIgold

Great Eastern: https://www.greateasternlife.com/

Singlife: https://singlife.com/en

GROW with Singlife: https://grow.singlife.com/

Maribank: https://www.maribank.sg/product/mari-invest/gold

Bank of Singapore: https://www.bankofsingapore.com/Homepage.html

iFAST: https://secure.ifastnetwork.com/ifastverve/home/index.tpl

POEMS: https://www.poems.com.sg/fund-finder/lionglobal-physical-gold-fund-sgd-573002/

CapBridge: https://www.capbridge.sg/

Disclaimer – Lion Global Investors Limited

This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. It is for information only, and is not a recommendation, offer or solicitation for the purchase or sale of any capital markets products or investments and does not have regard to your specific investment objectives, financial situation, tax position or needs.

You should read the prospectus and Product Highlights Sheet of the LionGlobal New Wealth Series II – LionGlobal Singapore Physical Gold Fund (the “Fund”) which are available and may be obtained from Lion Global Investors Limited (“LGI”) or any of its distributors, for further details including the risk factors and consider if the Fund is suitable for you and seek such advice from a financial adviser if necessary, before deciding whether to invest in the Fund. Applications for units in the Fund must be made on forms accompanying the prospectus.

An investment in a precious metals fund carries risks of a different nature from other types of collective investment schemes which invest in transferable securities and a precious metals fund may not be suitable for persons who are adverse to such risks.

An investment in a precious metals fund is not intended to be a complete investment programme for any investor. As a prospective investor, you should carefully consider whether an investment in a precious metals fund is suitable for you, taking into account, your investment objectives, risk appetite and the potential price movements of precious metals. You are responsible for your own investment choices.

Investments in the Fund are not obligations of, deposits in, guaranteed or insured by LGI or any of its affiliates and are subject to investment risks including the possible loss of the principal amount invested. The performance of the Fund is not guaranteed and the value of units in the Fund and the income accruing to the units, if any, may rise or fall. Past performance, payout yields and payments as well as any predictions, projections, or forecasts are not necessarily indicative of the future or likely performance, payout yields and payments of the Fund. Any extraordinary performance may be due to exceptional circumstances which may not be sustainable. Any dividend distributions, which may be either out of income and/or capital, are not guaranteed and subject to LGI’s discretion. Any such dividend distributions will reduce the available capital for reinvestment and may result in an immediate decrease in the net asset value of the Fund. There can be no assurance that any of the allocations or holdings presented will remain in the Fund at the time this information is presented. Any information (which includes opinions, estimates, graphs, charts, formulae or devices) is subject to change or correction at any time without notice and is not to be relied on as advice. You are advised to conduct your own independent assessment and investigation of the relevance, accuracy, adequacy and reliability of any information or contained herein and seek professional advice on them. No warranty is given and no liability is accepted for any loss arising directly or indirectly as a result of you acting on such information. The Fund may, where permitted by the prospectus, invest in financial derivative instruments for hedging purposes or for the purpose of efficient portfolio management. The Fund’s net asset value may have higher volatility due to its narrower investment focus (primarily in Gold (as defined in the prospectus)), when compared to funds with more diversified portfolios.

LGI, its related companies, their directors and/or employees may hold units of the Fund and be engaged in purchasing or selling units of the Fund for themselves or their clients.

This publication is issued in Singapore ©Lion Global Investors® Limited (UEN/ Registration No. 198601745D). All rights reserved. LGIis a Singapore incorporated company, and is not related to any corporation or trading entity that is domiciled in Europe or the United States (other than entities owned by its holding companies).

Disclaimer – ICE Benchmark Administration Limited

THE LBMA GOLD PRICE, WHICH IS ADMINISTERED AND PUBLISHED BY ICE BENCHMARK ADMINISTRATION LIMITED (IBA), SERVES AS, OR AS PART OF, AN INPUT OR UNDERLYING REFERENCE FOR LIONGLOBAL SINGAPORE PHYSICAL GOLD FUND.

LBMA GOLD PRICE IS A TRADE MARK OF PRECIOUS METALS PRICES LIMITED, AND IS LICENSED TO IBA AS THE ADMINISTRATOR OF THE LBMA GOLD PRICE. ICE BENCHMARK ADMINSTRATION IS A TRADE MARK OF IBA AND/OR ITS AFFILIATES. THE LBMA GOLD PRICE AM, AND THE TRADE MARKS LBMA GOLD PRICE AND ICE BENCHMARK ADMINISTRATION, ARE USED BY LION GLOBAL INVESTORS LIMITED WITH PERMISSION UNDER LICENCE BY IBA.

IBA AND ITS AFFILIATES MAKE NO CLAIM, PREDICATION, WARRANTY OR REPRESENTATION WHATSOEVER, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED FROM ANY USE OF THE LBMA GOLD PRICE, OR THE APPROPRIATENESS OR SUITABILITY OF THE LBMA GOLD PRICE FOR ANY PARTICULAR PURPOSE TO WHICH IT MIGHT BE PUT, INCLUDING WITH RESPECT TO LIONGLOBAL SINGAPORE PHYSICAL GOLD FUND. TO THE FULLEST EXTENT PERMITTED BY APPLICABLE LAW, ALL IMPLIED TERMS, CONDITIONS AND WARRANTIES, INCLUDING, WITHOUT LIMITATION, AS TO QUALITY, MERCHANTABILITY, FITNESS FOR PURPOSE, TITLE OR NON-INFRINGEMENT, IN RELATION TO THE LBMA GOLD PRICE, ARE HEREBY EXCLUDED AND NONE OF IBA OR ANY OF ITS AFFILIATES WILL BE LIABLE IN CONTRACT OR TORT (INCLUDING NEGLIGENCE), FOR BREACH OF STATUTORY DUTY OR NUISANCE, FOR MISREPRESENTATION, OR UNDER ANTITRUST LAWS OR OTHERWISE, IN RESPECT OF ANY INACCURACIES, ERRORS, OMISSIONS, DELAYS, FAILURES, CESSATIONS OR CHANGES (MATERIAL OR OTHERWISE) IN THE LBMA GOLD PRICE, OR FOR ANY DAMAGE, EXPENSE OR OTHER LOSS (WHETHER DIRECT OR INDIRECT) YOU MAY SUFFER ARISING OUT OF OR IN CONNECTION WITH THE LBMA GOLD PRICE OR ANY RELIANCE YOU MAY PLACE UPON IT.