This article was written in collaboration with Singlife. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, are purely for informational purposes, and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions, and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

As parents, our main goal is to ensure our children live healthy and fulfilling lives. Unfortunately, critical illnesses like cancer are on the rise, especially among younger people. According to the latest Singapore Cancer Registry report, the number of women under 30 diagnosed with cancer has increased about 2.5 times over the past 10 years. Leukaemia and lymphoma are some of the most common childhood cancers in Singapore.

Globally, childhood cancer is more common than most parents realise. According to the World Health Organisation (WHO), about 1 in every 500 children aged 0 to 19 will develop cancer. While this figure may seem small, the emotional, logistical and financial impacts on individual families can be overwhelming. For parents, the impact goes beyond medical treatment. It can mean taking extended time off work, juggling care for other children, and making difficult decisions under emotional stress.

One positive news is that childhood cancer survival rates exceed 80% in high-income countries, thanks to strong public health programmes and timely, high-quality clinical services with multidisciplinary approaches.

Nevertheless, the road to recovery often involves prolonged hospital visits, regular treatments, and additional care and support. This is why having critical illness coverage for your child can make financial sense – helping to ease the cost burden and provide financial support if you need to take time off to care for them.

Read Also: Why I Decided To Insure Myself With A Multipay Critical Illness Plan After Becoming A Parent

How Critical Illness Plans Work

Getting a critical illness plan for your child means receiving a sum of money should they be diagnosed with one of the critical illnesses the plan covers. These include major cancers, severe bacterial meningitis, and end stage kidney failure.

Many basic critical illness plans only provide coverage for the most severe conditions, usually only at the later stages of the disease. For example, a basic critical illness plan may only cover end stage lung disease, and not the severe asthma which led to it.

This is why comprehensive critical illness coverage, which also covers the early and intermediate stages of the critical illness, is beneficial. That said, another aspect of critical illnesses is the possibility of them recurring. Someone with lymphoma may recover, but relapse after a few years.

That is why a multipay critical illness plan can be important. Unlike traditional critical illness plans, which terminate after one claim, leaving no further protection and likely inability to buy adequate protection given the medical history, a multipay critical illness plan ensures continued protection after diagnosis. This means no matter how early your child’s critical illness is detected, they will have comprehensive coverage should the critical illness recur.

For example, the Singlife Multipay Critical Illness II plan provides multiple payouts for different stages of 135 critical illnesses and medical conditions, with a total payout of up to 900% of the sum assured.

For parents, this continued protection matters. A relapse or a new diagnosis years later can be just as disruptive, especially as children grow older, schooling commitments increase, and family finances may already be stretched.

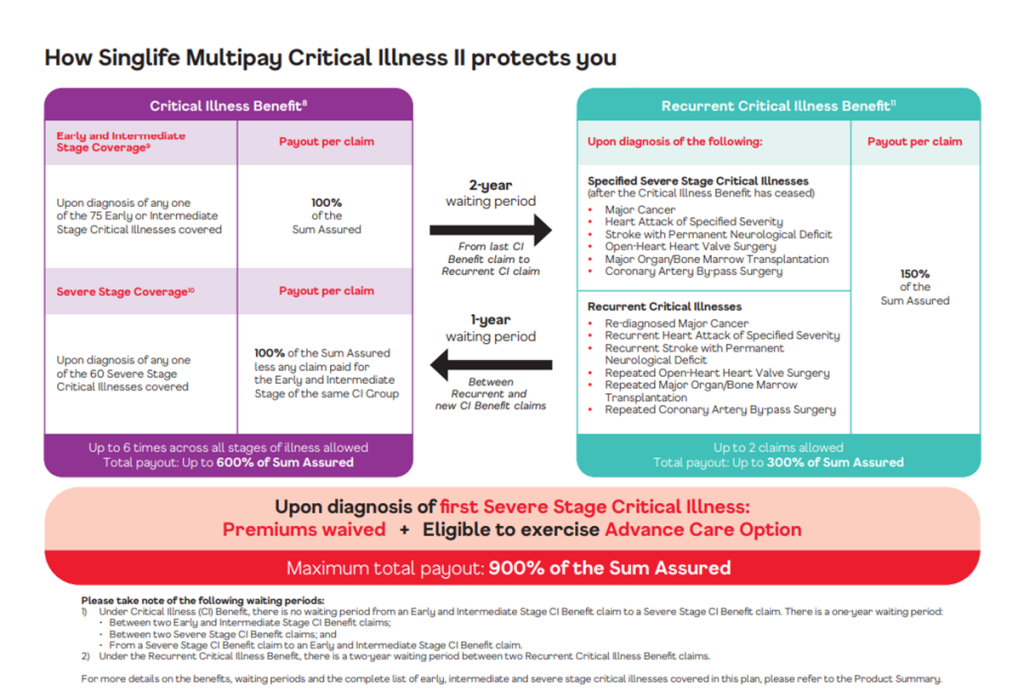

The plan’s coverage provides three key benefits:

Early or Intermediate Stage Critical Illness: Upon diagnosis of any of the 75 Early or Intermediate Stage Critical Illnesses covered, the plan provides a payout of 100% of the Sum Assured per claim.

Severe Stage Critical Illness: Upon diagnosis of any of the 60 Severe Stage Critical Illnesses covered, the plan offers a payout of 100% of the Sum Assured, minus any claims already paid for the same critical illness group at the early or intermediate stages. Following the first severe stage diagnosis, future premiums are waived, and you may opt for the Advance Care Option, which provides additional payout to support longer-term care needs.

The maximum payout under the Critical Illness Benefit (covering both early/intermediate and severe stages) is 600% of the Sum Assured.

Recurrent Critical Illness: Should there be a diagnosis of any of the 6 specified severe stage critical illnesses, or any of the 6 recurrent critical illnesses, the plan pays out 150% of the Sum Assured per claim, up to 2 claims. This results in a maximum payout of 300% of the Sum Assured, assuming the Advance Care Option is not exercised.

In total, policyholders may receive payouts up to 900% of the Sum Assured, offering substantial financial support during challenging times.

Source: Singlife

The Singlife Multipay Critical Illness II plan also offers extra coverage for special conditions, equivalent to 20% of your sum assured (capped at S$25,000), in the following situations:

– When a borderline malignant tumour or benign tumour (with suspected malignancy) requires surgical removal;

– When you require an Intensive Care Unit (ICU) stay of 4 days or more in a single hospital admission;

– When you are diagnosed with one of the 34 conditions under the Special Benefit (payout is per condition).

Critical Illness Coverage Should Start As Early As Possible

The earlier a critical illness is diagnosed, the higher the chance of a full recovery. For critical illnesses like cancer, this is even more crucial as treatments are less aggressive the earlier a tumour is detected. This is because they tend to be smaller and have not yet spread to other parts of the body.

Early detection also leads to higher survival rates. For example, breast cancer survival rates in Singapore are over 90% when caught at the earliest stages. Furthermore, because the treatments are less aggressive at the earlier stages, they cost less, and recovery times are shorter.

This is where early-stage critical illness coverage becomes important. With the Singlife Multipay Critical Illness II plan, an early or intermediate stage diagnosis triggers a payout, giving families timely financial support when treatment and care begin, rather than only at the most sever stage of illness.

Starting coverage early also allows you to secure long-term protection for your child while they are young and healthy. The Singlife Multipay Critical Illness II plan offers coverage of up to age 99, enabling your child to remain on the same plan into adulthood, without the need to reapply or undergo new health assessments later in life.

In the unfortunate scenario that they are diagnosed with a critical illness, the coverage can provide a crucial financial safety net for your family, helping to pay for treatments and additional care, especially if one of you has to leave work for a period of time as well. Beyond treatment costs, having financial support can give parents flexibility – whether that means spending more time with their child during recovery, seeking additional care options, or reducing financial stress during an already difficult period.

At the same time, there is also a waiver of premiums upon diagnosis of the first severe stage critical illness after 300% of the Sum Assured is paid under the Critical Illness Benefit. Once this happens, you and your child do not have to make premium payments but continue to remain covered under the Singlife Multipay Critical Illness II plan. This can offer an invaluable peace of mind for your family.

T&Cs apply. This policy is underwritten by Singapore Life Ltd. This material is published for general information only and does not have regard to the specific investment objectives, financial situation and particular needs of any specific person. Any views, thoughts, and opinions expressed do not reflect the views, opinions, policies, or position of Singapore Life Ltd or its related corporation (where applicable) (collectively, the “Singlife Group”). The Singlife Group does not endorse any views, thoughts, or opinions expressed here and is not responsible for the contents here. You should read the Product Summary and seek advice from a financial adviser representative before making a commitment to purchase the product. As this product has no savings or investment feature, there is no cash value if the policy ends or if the policy is terminated prematurely. Buying a health insurance policy that is not suitable for you may impact your ability to finance your future healthcare needs. This advertisement has not been reviewed by the Monetary Authority of Singapore. Protected up to specified limits by SDIC. Information is accurate as at 6 Jan 2026.