This article was written in collaboration with SGX. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, are purely for informational purposes, and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions, and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

For many working professionals in Singapore, the Supplementary Retirement Scheme (SRS) isn’t the main focus when it comes to building retirement savings. This is because unlike CPF contributions, which are compulsory for Singapore Citizens and Permanent Residents, participation in the SRS is entirely optional. This optionality also means it is frequently overlooked.

The main appeal of the SRS lies in its tax benefits. Contributions of up to $15,300 a year for Singapore Citizens and Permanent Residents, and $35,700 for foreigners, qualify for dollar-for-dollar tax relief. For someone in the 11.5 per cent personal income tax bracket (income between $80,000 and $120,000 a year), a $10,000 SRS contribution translates into immediate tax savings of $1,150. For higher-income earners, the savings can be even higher.

However, many contributors underestimate the cost of leaving SRS funds idle. Cash parked in an SRS account earns just 0.05% per annum. This is far lower than CPF balances, which earn a base interest rate of between 2.5 and 4% per annum (p,a,), or even relatively low-risk options like Singapore Savings Bonds, which currently offer around 2% p.a.

Over time, inflation does the real damage. Even at a modest long-term inflation rate of 2% a year, the purchasing power of uninvested SRS savings steadily erodes. Over a 20- to 30-year horizon, this compounding effect can significantly reduce what looks like a healthy balance on paper.

This is why investing SRS funds matters. The tax relief enjoyed today is only half the equation. The other half is ensuring these savings grow meaningfully over time. By investing SRS monies, we give our retirement savings a chance to outpace inflation and compound steadily, turning short-term tax savings into long-term financial security.

In this sense, the SRS is not just a tax tool, but a retirement planning tool. It only works as intended when the money inside it is put to work.

Why ETFs Are A Simple Way To Invest Our SRS

One of the most straightforward ways to invest our SRS savings is through exchange-traded funds (ETFs) listed on the Singapore Exchange (SGX). For many investors, ETFs offer a practical balance of simplicity, diversification and cost efficiency.

With a single trade, an ETF provides instant diversification across dozens or even hundreds of stocks or bonds, reducing reliance on any single investment. This makes ETFs well-suited for long-term retirement investing, where steady compounding matters more than stock picking.

Unlike mutual funds that are not exchange-listed, ETFs trade on stock exchanges, giving investors real-time price visibility and certainty when making allocation decisions. In today’s fast-moving and often volatile markets, the value of your investment can fluctuate within a single day. This is where the tradable nature of ETFs becomes a key advantage—allowing you to react quickly and manage your portfolio with greater flexibility.

ETFs also support a passive and fuss-free approach. Most ETFs track an index, removing the need to monitor individual companies or time market cycles. For busy professionals, this simplicity is both convenient and sustainable.

Cost is another advantage. ETFs typically charge lower fees than actively managed unit trusts and can be bought and sold on the SGX like shares. With low minimum investment amounts, SRS funds can also be deployed gradually.

Taken together, ETFs provide a practical and efficient way to put SRS savings to work, without turning retirement planning into a second job.

Types Of ETFs We Can Invest In Through Our SRS Savings

For those of us who want to build a retirement portfolio through ETFs, the good news is that we can use our SRS savings to invest in various types of ETFs that are listed on the SGX.

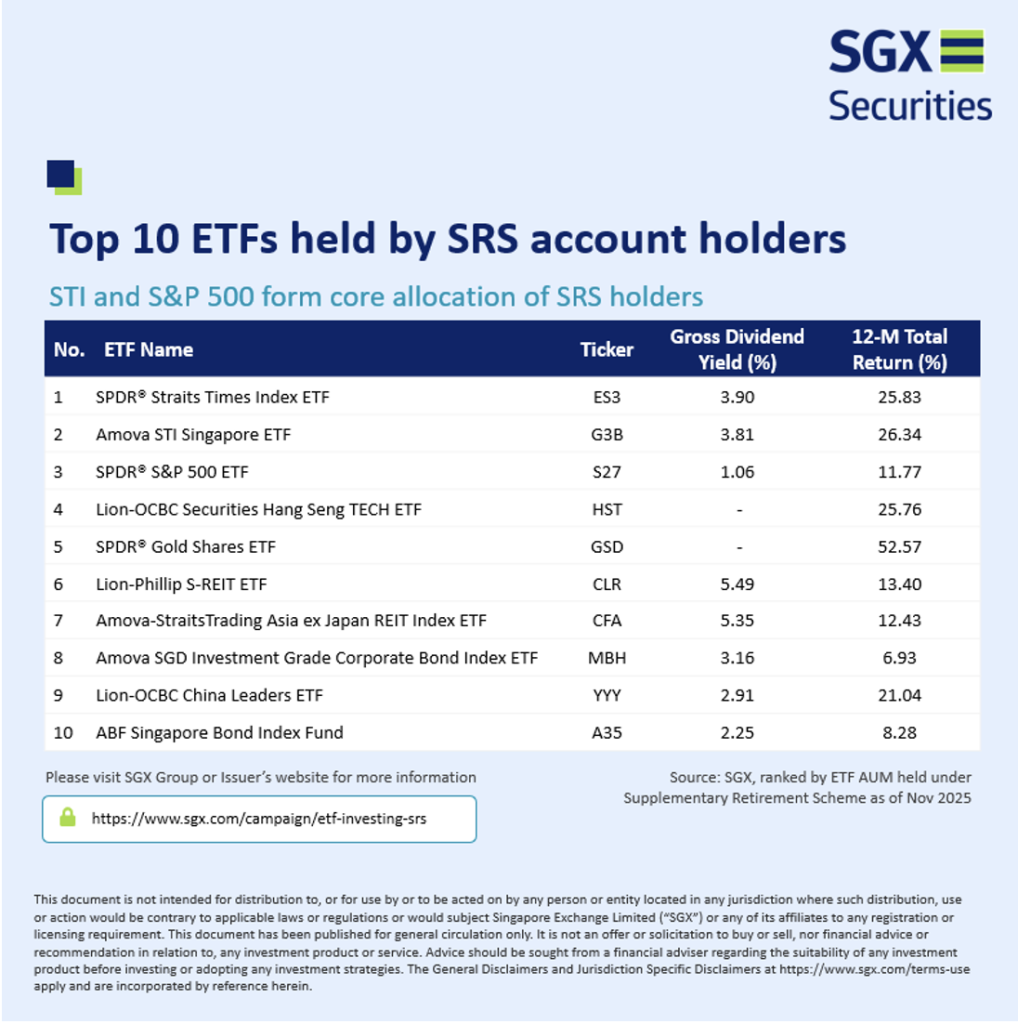

Local & Foreign Equities: At the core of many retirement portfolios are equity ETFs. Investors who prefer local exposure can consider Singapore-focused ETFs such as the SPDR Straits Times Index ETF (ES3) or the Amova Singapore STI ETF (G3B), both of which track the performance of the Straits Times Index. These ETFs provide exposure to Singapore’s largest listed companies across banking, telecommunications and industrial sectors.

For those who want overseas diversification, SRS funds can also be used to invest in ETFs that track foreign markets. Examples include the SPDR S&P 500 ETF (S27), which offers exposure to the 500 largest companies in the United States, and the Lion-OCBC Securities Hang Seng Tech ETF (HST), which focuses on major technology companies listed in Hong Kong.

Real Estate Investment Trust (REIT ETFs): Beyond equities, REIT ETFs are another popular option among SRS investors. The Lion-Phillip S-REIT ETF (CLR), for instance, provides exposure to a diversified basket of Singapore-listed real estate investment trusts. REIT ETFs appeal particularly to investors seeking regular income, as REITs are required to distribute most of their taxable income. Over time, these distributions can help supplement retirement cash flow, although they may fluctuate with interest rates and property market conditions.

Bond ETFs: For investors who prioritise stability and lower volatility, bond ETFs can play an important role. Options such as the ABF Singapore Bond Index Fund (A35), Amova SGD Investment Grade Corporate Bond Index ETF (MBH) and LionGlobal Short Duration Bond Active ETF (SBO) offer exposure to Singapore government bonds or high-quality corporate bonds.

While expected returns from bonds are generally lower than equities over the long term, they help smooth portfolio fluctuations and become increasingly relevant as investors approach retirement and capital preservation matters more.

Gold ETF: Some investors also use SRS funds to gain exposure to alternative assets such as gold. Gold ETFs like the SPDR Gold Shares (GSD) provide a way to invest in gold without holding physical bullion. Gold does not generate income, but it can serve as a long-term store of value and a hedge during periods of market stress or high inflation, helping to diversify an overall retirement portfolio. The World Gold Council (WGC), through its extensive research, suggests that a strategic gold allocation of 2% to 10% significantly benefits diversified portfolios by improving risk-adjusted returns, acting as a diversifier, and providing stability during uncertainty.

Here are the top ETFs held by SRS investors (as of November 2025).

Source: SGX

Building An ETF Retirement Portfolio

An ETF-based SRS portfolio is about combining different asset classes in line with our age, risk tolerance and time horizon. The same ETFs can be arranged very differently for someone in their 30s compared to an investor nearing retirement.

Younger investors with decades to go can afford to tilt more heavily towards equity ETFs, capturing long-term growth despite short-term volatility. REIT ETFs can add income, while bond ETFs usually play a smaller stabilising role at this stage.

As retirement draws closer, the focus shifts towards capital preservation. Bond and income-oriented ETFs typically take up a larger share to smooth returns and reduce the impact of market swings, with a modest allocation to gold ETFs helping to diversify during periods of uncertainty.

Ultimately, the goal is not to find the “best” ETF, but to build a balanced mix of growth, income, and defensive assets that can compound steadily and remain aligned with evolving retirement needs.

Understanding SRS Withdrawal Rules

Before investing through the SRS, it is important to understand the withdrawal rules, as they shape how these savings should be used. Early withdrawals made before the statutory retirement age are fully taxable and subject to a 5 per cent penalty, making them expensive and counterproductive.

Once the applicable retirement age is reached, withdrawals become far more tax-efficient. They can be spread over up to 10 years, with only 50 per cent of each withdrawal treated as taxable income. With careful planning, many retirees pay little or no tax. For instance, withdrawing $40,000 a year from a $400,000 SRS balance results in just $20,000 of taxable income annually, which falls within Singapore’s tax-free threshold if there is no other income.

These rules make it clear that the SRS is meant for long-term retirement planning, not short-term access. Used strategically alongside our cash investments and CPF savings, it can form a meaningful nest egg for our retirement.

Read Also: Withdrawing Your SRS Savings: Here’s Why You Need To Be Tactical About Withdrawals After Investing

For a quick summary, here are the key takeaways at a glance:

Photo Credit: iStock/Dilok Klaisataporn