More than 7 in 10 Singapore Residents have bought an Integrated Shield Plan (IP) to enhance their healthcare coverage, on top of their base MediShield Life plan. Two-thirds of them have additional IP riders to boost coverage levels.

While this may give you extra peace of mind, for those paying the premiums, you will know that costs have been running up in recent years.

The usual suspects for escalating costs are over-consumption by policyholders (aka the buffet syndrome) and potentially over-charging by healthcare providers. In recent years, the government has already taken active measures to tackle this, including:

– removing the 100% coverage under IPs from 2019;

– introducing fee benchmarks since 2018;

– taking enforcement measures against a small minority of errant doctors; and

– exploring the feasibility of a new not-for-profit private hospital

Insurers that offer IP plans will also offer riders that provide even more comprehensive coverage, and charge an extra premium. Premiums for IP riders must be paid in cash only – and you cannot use MediSave to pay for it.

Riders are typically meant to reduce your out-of-pocket costs, for deductibles and co-payments. Deductibles are the fixed amount you have to pay before your insurance coverage kicks in. After paying the deductible, there is also a 10% co-payment by default.

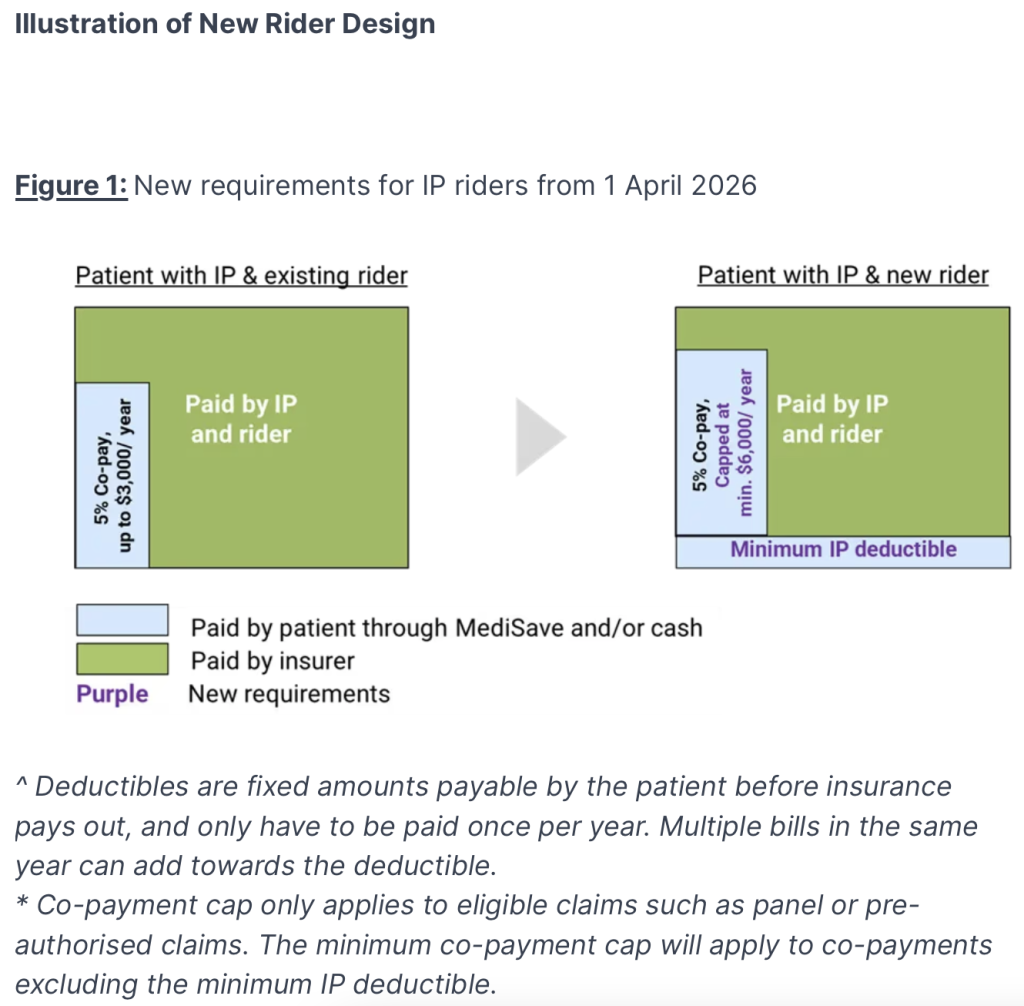

Currently, the most comprehensive IP riders typically take care of the deductible and reduce the co-payment to 5%, subject to an annual cap of $3,000. On 26 November 2025, a new set of requirements for such IP riders were announced, to continue the effort to address rising insurance premiums and healthcare costs.

These changes will come into effect from 1 April 2026, and new IP riders sold will not be allowed to fully cover the minimum IP deductibles set by MOH. This is because the deductibles are meant to instil discipline in healthcare consumption, and reducing it may negate its purpose. The minimum deductibles range from $1,500 to $3,500 per policy year, depending on ward class.

The co-payment cap, which was set at a minimum of $3,000 per year in 2018, will also be raised to $6,000 per year. This is to keep pace with the increase in bill sizes over time. This co-payment excludes the minimum IP deductible. However, there’s no change to the minimum 5% co-payment requirement.

This should lead to a lower premium, by about 30%. And this can potentially help cover the deductibles you have to pay.

Here are 4 things you need to know about how these changes may affect you.

Read Also: Complete Guide To Buying A Private Integrated Shield Plan

#1 You May Not Need To Do Anything If You’re Covered Under An IP Rider

There may be some confusion that everyone who currently owns an IP rider is immediately affected. This is not entirely true.

For those who have already have an IP rider, the new design changes may only affect you as far away as 1 April 2028. This means nothing really changes for you in the short term, and you can continue to be covered under the “more comprehensive” IP riders until 31 March 2028.

Nevertheless, you must transition to the new IP rider no later than you policy renewal after 1 April 2028.

In the interim, many insurers may allow you to transition to the new IP riders. But, you need to understand the coverage terms and costs before making a decision. While the new “less comprehensive” IP riders may cost about 30% cheaper, depending on your needs, you do not need to transit until your policy renewal after 1 April 2028.

For policyholders who do not expect to be hospitalised soon, such as those younger and healthier or not already nursing an injury, switching to new IP riders once they are offered can save you some money.

#2 You Can Still Buy A “More Comprehensive” IP Rider

The new set of changes only comes into effect by 1 April 2026. This means you can still buy a “more comprehensive” IP rider from now till 31 March 2026.

The same rules apply to you as an existing IP rider policyholder after that. You have until the next policy renewal date after 1 April 2028 to transit to an IP rider under the new design.

If you’re looking to buy an IP rider, you should not use this as an impetus to rush into buying a “more comprehensive” rider. In fact, the government is telling you to do the exact opposite, buy a less comprehensive one that is also more affordable.

#3 Continue To Be Careful When Switching Insurers

The timelines set out are deadlines when insurers must start offering new IP riders. Some insurers may wish to transit earlier, at the same time, premiums for the “more comprehensive” riders will continue to rise – perhaps unevenly across insurers.

If you’re looking to switch to a different insurer, note that your pre-existing conditions may not be covered. Similarly, even if you are switching to a higher level of coverage with your existing insurer, you need to know if any pre-existing conditions will be covered.

So, you must be careful and ask your insurance adviser.

Read Also: How Much Your MediShield Life Premiums Will Be Going Up From April 2025

#4 Minimum Deductibles & Co-Payment Features Are Not New

Finally, you should also know that the new changes are not really introducing anything new. You can view them as simply tightening the process.

As mentioned above, there is already a deductible feature on IP plans. However, the most comprehensive existing IP riders can cover the entire deductibles. This is what MOH is targeting – and wants to ensure that there is a minimum IP deductible ranging from $1,500 to $3,000 depending on ward class.

| Targeted Coverage of the Insured Person’s IP | Ward Class Utilised by Insured Person | Minimum Deductible (Lower of Target IP Coverage or Ward Class Utiltised) |

| Class A/Private | Class A/Prviate | $3,500 |

| Class B1 | Class B1 | $2,500 |

| Class B2 Class C | Class B2 Class C | $2,000 $1,500 |

| Outpatient | NA | NA |

| Day Surgery/Short Stay Wards | Non Subsidised Subsidised | $2,000 $1,500 |

Similarly, co-payment features also exist today. While the default co-payment is 10% of the bull, IP riders reduce this to 5%. The new requirements does not mandate an increase the co-payment – and it remains at a minimum of 5%.

However, the co-payment cap will be raised to a minimum of $6,000 per year, instead of $3,000 per year that was set in 2018.

Here’s how coverage under the new IP rider will look like.

Bonds and Fixed Income

StashAway Income Portfolio: How You Can Earn 4.6%* Dividends From Your Investments Each Year