The start of a new year is always a good time to plan our finances. While many of us set savings and investment goals, one area that often gets overlooked is budgeting for healthcare expenses.

Healthcare spending can cover many things, from GP and dental visits to insurance premiums, and the amount varies depending on how frequently we use healthcare services and the policies we hold.

However, there is one area where costs are more predictable: the premiums we pay for national insurance schemes such as MediShield Life and CareShield Life, both of which can be paid using our MediSave savings.

In this article, we look at how much MediSave a healthy adult would typically use each year. For this article, we will assume a 40-year-old male with no underlying health issues. For simplicity, we will also assume that he enjoys no government subsidies or premium rebates.

#1 MediShield Life Premiums

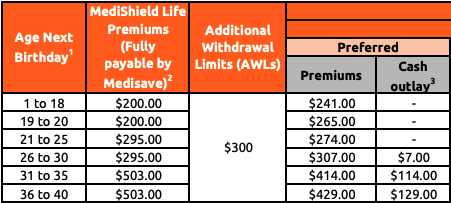

MediShield Life premiums are fixed by age, with younger individuals paying lower premiums and older individuals paying higher premiums. For example, those aged 20 and below pay $200 a year in premiums, while those aged 90 and above pay $2,826 a year.

For a 40-year-old, premiums are $503 a year.

Source: CPF

#2 Private Integrated Shield Plan

According to the Ministry of Health (MOH), seven in ten Singaporeans choose to purchase Integrated Shield Plans (IPs) offered by private insurers. These IPs provide additional coverage for treatment at private hospitals or unsubsidised wards in public hospitals, such as Class A and B1 wards. Premiums for IPs can be partially paid using MediSave, subject to annual limits.

For a fair lifetime comparison, MOH publishes the lifetime premiums of these IPs. Lifetime premiums are a helpful way to assess overall cost since different insurers charge different premiums across age groups. For example, one insurer may offer lower premiums for those under 40, while another may be cheaper for policyholders above 40.

Source: MOH

For this exercise, we will focus only on annual premiums. Assuming we choose the insurer with the median cost (Income, Enhanced IncomeShield Preferred), the premium for a 40-year-old is $429.

Source: Income

Since MediSave only allows up to $300 to be used under the Additional Withdrawal Limits (AWLs), the policyholder will need to pay the remaining $129 in cash.

This amount also excludes riders, as their premiums must be paid in full in cash.

Read Also: Guide To Buying A Private Integrated Shield Plan

#3 CareShield Life Premiums

CareShield Life was introduced in October 2020 and added a significant new protection pillar to Singaporeans’ health insurance portfolios. As a compulsory disability insurance scheme, CareShield Life sits alongside MediShield Life, which serves as our compulsory, basic national health insurance policy.

MediSave fully covers CareShield Life premiums. It is worth noting that annual premiums are payable until age 67, and the premium amount increases each year to support higher payouts.

For a 40-year-old male, the premium is about $254 a year, fully payable using MediSave. Do note that with government subsidies, your actual payment will likely be lower.

Read Also: Higher CareShield Life Premiums From 2026: Why This Is Necessary As Singapore’s Population Ages

#4 CareShield Life Supplement Premiums

CareShield Life supplements are plans that enhance the coverage you receive on top of the basic CareShield Life plan. These may include higher monthly payouts and lower eligibility criteria.

MediSave savings can be used to purchase any MediSave-approved supplement plan offered by private insurers, up to a limit of $600 per insured person per calendar year.

Premiums for CareShield Life supplements vary by coverage level. However, in general, you can expect to use most, if not all, of this $600 annual limit.

In total, a 40-year-old male can expect to pay the following from his MediSave each year.

| MediShield Life Premiums | $503/year |

| Private Integrated Shield Plan | $300/year (AWLs limit) |

| CareShield Life Premiums | ~ $254/year |

| CareShield Life Supplement Premiums | $600/year |

| Total | $1,657 |

It is also fair to say that this amount will increase over time, as we grow older and as medical costs continue to rise due to inflation. Also, if we require any treatment or screening during the year, this may also be deducted from our MediSave.

If we have dependants, such as elderly parents or children, their medical premiums for MediShield Life, private Integrated Shield Plans, and CareShield Life and its supplement plans may also be deducted from our MediSave. This means the total amount we actually use could be significantly higher than just our individual premiums alone.

This is why contributing to our MediSave, whether through our employment income or voluntary top-ups (which also provide tax relief), is important. The government also contributes periodically by topping up our MediSave.

Ultimately, understanding how much of our MediSave may be used each year helps us plan better, not just for today, but for our long-term healthcare needs as well. While most of us may not think much about these deductions, they form a meaningful part of our overall financial planning, giving us peace of mind when it comes to healthcare.