In Singapore, many households are fortunate to employ a migrant domestic worker. But employing a helper also comes with responsibilities. One of them is buying insurance.

If you hire a migrant domestic worker, insurance is not optional. It is mandatory under the law. Yet there is a difference between knowing you must buy insurance and knowing whether the coverage you have is actually sufficient.

In reality, many employers treat this as an administrative task. They renew the policy each year, often choosing the cheapest option available, and move on. That is understandable. However, the insurance requirements set by the Ministry of Manpower (MOM) have changed quite significantly in recent years. That makes it worth revisiting whether the minimum coverage still makes sense for your household.

Here is a closer look at what the minimum coverage provides and whether it might be worth considering a more comprehensive plan.

What The Minimum Coverage Actually Includes

Under the Employment of Foreign Manpower Act, employers must purchase two types of insurance for their migrant domestic worker: medical insurance and personal accident insurance.

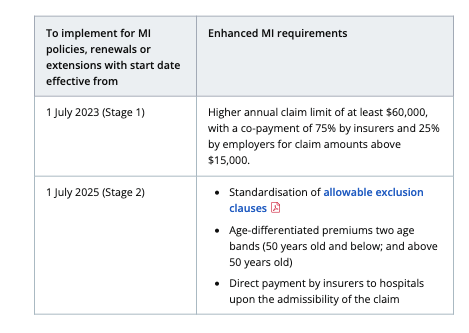

Since 1 July 2023, the minimum medical insurance coverage has increased substantially. Previously, policies only needed to cover $15,000 a year. That has now been raised to $60,000 per year, covering inpatient hospital treatment and day surgery.

Source: MOM

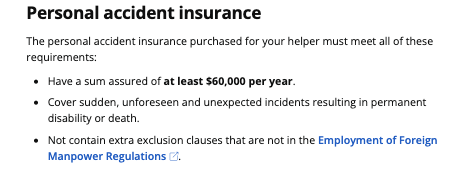

Employers must also purchase personal accident insurance of at least $60,000, payable to the helper or her beneficiaries in the event of death or permanent disability.

Source: MOM

This change was not just a routine update. The previous $15,000 limit was increasingly inadequate, as more than 5% of hospital bills already exceeded that amount, leaving employers to cover the shortfall themselves. With healthcare costs continuing to rise in Singapore, the gap was only likely to widen.

The revised $60,000 limit is estimated to cover more than 99% of expected hospitalisation and surgical costs, significantly reducing the risk of employers facing high out-of-pocket costs.

However, there is an important detail many employers overlook. A co-payment structure now applies for larger claims.

For medical bills below $15,000, the insurer covers the full amount. But once the bill exceeds $15,000, the insurer covers 75% of the remaining amount, while the employer pays the other 25%, up to the $60,000 annual cap. In a worst-case scenario where the full $60,000 is used, the employer could still end up paying up to $11,250 out of pocket.

That may not sound enormous, but it is a cost that many households might not expect when they assume the insurance will cover everything.

Read More: 6 Courses To Upgrade Skills Of Migrant Domestic Workers

What Changed In July 2025

Insurance requirements for migrant domestic workers were enhanced again on 1 July 2025. These changes apply to all new, renewed or extended policies.

One of the most important updates is the introduction of a standardised list of exclusions. Previously, insurers could apply their own exclusions, which sometimes led to unpleasant surprises when claims were rejected. Now, insurers are only allowed to exclude treatments listed by MOM. This creates greater transparency and helps employers better understand what their policy covers.

Another change is that premiums are now age-differentiated. Policies are generally split into two bands: helpers aged 50 and below, and those aged 50 and above. Since most migrant domestic workers are younger, premiums should remain relatively affordable for most households.

Perhaps the most practical improvement is the introduction of direct billing. In the past, employers typically had to pay hospital bills upfront and then submit claims for reimbursement. Under the updated framework, insurers will now pay hospitals directly for the claimable portion. This removes the need for employers to temporarily shoulder large medical bills while waiting for reimbursement.

Why Some Employers Choose More Than The Minimum

The minimum insurance requirements exist to ensure every migrant domestic worker has a baseline level of protection. But minimum coverage is exactly what it is, the minimum. And this may not necessarily be sufficient for all.

One key gap is outpatient treatment.

The mandatory insurance only covers hospitalisation and day surgery. If your helper falls ill and needs to visit a GP, attend follow-up consultations, or undergo physiotherapy after an injury, those costs will typically be borne by the employer unless the policy includes outpatient benefits.

While each visit might only cost tens or hundreds of dollars, repeated treatments can add up over time.

Another situation to consider is long-term hospitalisation. If your helper is unable to work while recovering, you may still be required to pay her salary and the monthly foreign worker levy. Some enhanced plans offer wage and levy compensation, helping to offset these ongoing expenses.

There is also the scenario where your helper becomes medically unfit to continue working. In such cases, employers often need to hire a replacement. That usually involves paying agency fees and administrative costs again. Certain insurance plans include replacement coverage, which can help reduce these financial pressures.

Finally, there are repatriation costs to think about. If a helper needs to be sent home due to serious illness or death, the cost of arranging travel and related logistics can add up quickly. More comprehensive insurance plans often include coverage for repatriation, whereas basic policies may offer limited protection.

How To Decide If It Is Worth It

Deciding whether to buy more than the minimum coverage is not about being overly cautious. It is essentially the same thought process you would apply when buying insurance for yourself.

You are assessing how much risk you are comfortable taking on.

For example, consider your helper’s age and health history. Older helpers are statistically more likely to require medical care. If your helper is above 50, the gap between the minimum insurance coverage and actual healthcare costs may be wider than expected.

You should also think about your household finances. If an unexpected $10,000 medical bill would significantly strain your budget, a more comprehensive plan could act as an important financial buffer.

On the other hand, if your household has sufficient savings to comfortably absorb such costs, the minimum coverage may still be a reasonable choice.

Regardless of which option you choose, it is important to read the policy exclusions carefully. Even with MOM’s standardised exclusion list, policies are not identical. Understanding exactly what your insurance covers before you need to make a claim can prevent unpleasant surprises later.

Minimum Protection Versus Peace Of Mind

The mandatory insurance requirements exist to ensure every migrant domestic worker has a basic level of protection while working in Singapore. The improvements introduced over the past few years such as higher coverage limits, standardised exclusions and direct hospital billing have strengthened this safety net.

However, there are still areas where the minimum coverage falls short. Outpatient treatment, wage compensation during long recoveries, repatriation costs and replacement expenses are all potential financial risks that employers may need to consider.

Ultimately, the question is not just whether the minimum requirement is enough. It is whether you are comfortable bearing the remaining risks yourself.

Read Also: How Much Does It Cost To Hire A Maid In Singapore?

Photo Credit: Raymond Quek/DollarsAndSense

Advertiser Message

Thinking Of Switching Brokers Or Consolidating Your Holdings?

Tiger Brokers is currently running a transfer-in campaign where eligible clients can receive an iPhone 17 Pro Max* when they transfer in their assets.

For SGX investors, there is also a CDP Transfer promotion with 0* commissions on Singapore stocks.

Find out more here. *T&Cs apply.

Bonds and Fixed Income

StashAway Income Portfolio: How You Can Earn 4.6%* Dividends From Your Investments Each Year