This article was written in collaboration with OCBC. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, are purely for informational purposes, and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions, and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

Travelling to China is on the to-do list for many people in Singapore, whether it is for food, culture, shopping, or simply to see how fast the country has changed. According to Oxford Economics, an estimated 535,000 Singapore residents visited China in 2024, more than double the number in 2023.

For those who have never been to China before, or whose last visit was more than a decade ago, it is hard to fully imagine what China is like until you experience it firsthand. China is highly digitised, with technology embedded into everyday life. While travellers can avoid some tech conveniences, payments are one area that’s almost impossible to sidestep.

China is effectively a cashless society, with QR codes and mobile payments forming the backbone of day-to-day transactions. When I travelled to China last year, I brought cash just in case. Instead of helping, it led to awkward moments, such as when the staff couldn’t give me change, and I was sometimes compensated with extra toppings or a longer go-kart ride instead

Why Going Cashless In China Is Not As Simple As It Sounds

However, going cashless in China is not as straightforward as it might first appear for Singapore travellers. Unlike what we are used to back home, where Visa and Mastercard are widely accepted, China’s payment landscape is dominated by domestic platforms such as Weixin Pay (better known as WeChat Pay) and Alipay+. This means it is often not possible to simply use a Singapore-issued credit card to swipe or tap to pay, especially at smaller merchants.

Setting up these Chinese payment apps also comes with its own set of hurdles. In many cases, having a Chinese mobile number makes registration, verification, and day-to-day use much smoother. For those living or working in China long term, sorting this out is almost unavoidable, and the effort pays off over time.

For short-term travellers however, setting up apps and a local number can feel excessive for a brief holiday. But without mobile payments, even simple things like meals, transport, and attractions become harder.

This leaves many short-term visitors stuck in an uncomfortable middle ground. We need mobile payments to get around easily, but we do not necessarily want to download and install new payment apps just for a short trip.

How I Used The OCBC App To Pay In China

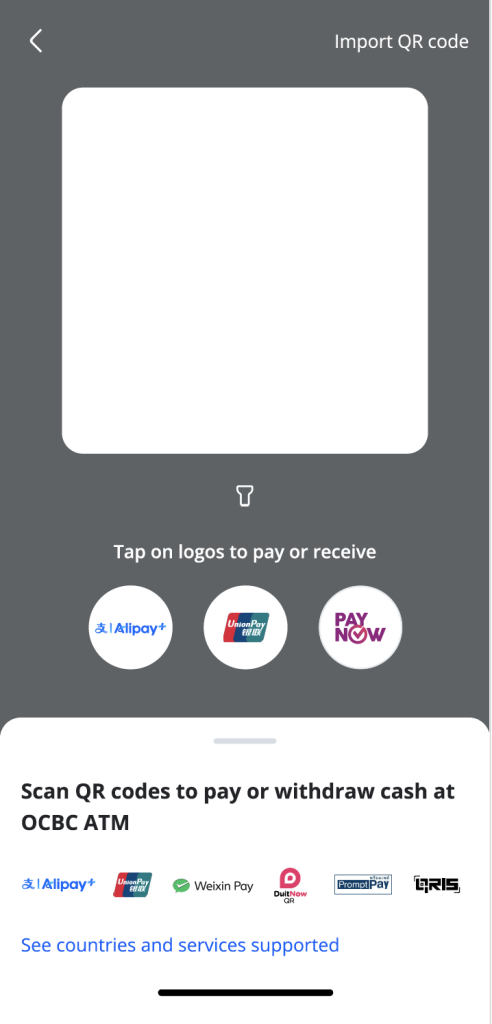

This is where the OCBC App is possibly the perfect solution. Instead of spending time figuring out how to set up new Chinese payment apps, the OCBC App already allowed me to make overseas payments seamlessly. In fact, it is the first banking app in Singapore that lets users scan and pay at virtually all merchant QR codes in China, including Alipay+, UnionPay and Weixin Pay.

Using it was straightforward. Whenever I needed to pay, I simply opened the OCBC App and selected the “Scan & Pay” option.

Once you select it, you will be able to see your QR code for Alipay+, UnionPay and others. Simply select your preferred payment mode. Present the QR code to the merchant to scan.

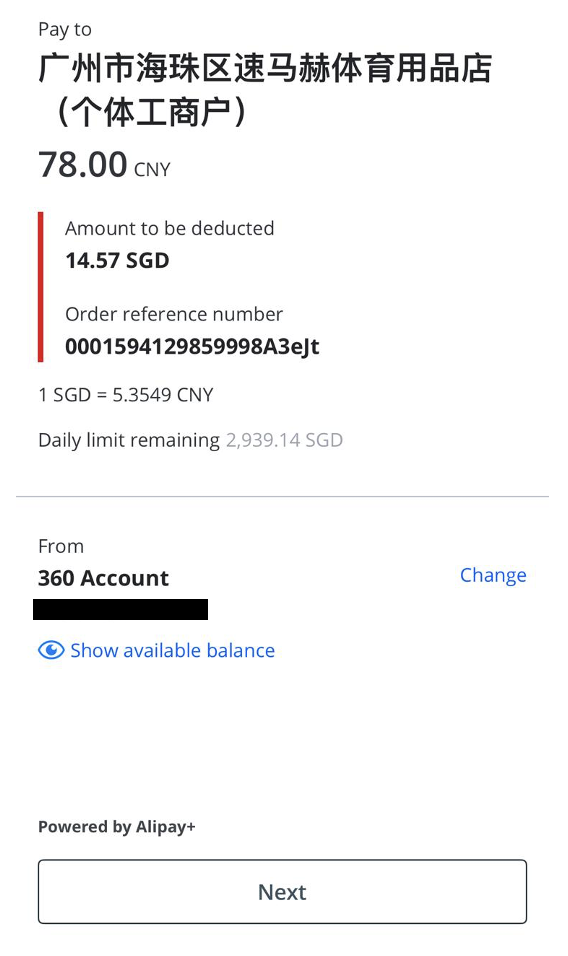

Once they scan, you will see the amount that you are supposed to pay. Before confirming payment, you can see the amount being charged in Chinese Yuan (CNY) and, more importantly, the amount being deducted in Singapore Dollar (SGD). The exchange rate you are getting is shown, and you get full transparency on the competitive rates with no hidden additional fees.

If you wish to make a payment using Weixin Pay, simply scan the merchant’s QR code to enter the amount and proceed with the transaction. This is similar to how you would make a PayNow transaction in Singapore. Likewise, you will be able to view the exchange rate in real time.

For those curious about the exchange rate, this particular transaction was made on 3 December 2025. On that day, the spot rate between the Singapore dollar and the Chinese yuan was 5.459. The bank rate applied to my transaction was 5.354. While it was not the absolute spot rate, it was close enough to be fair and transparent

While the bank rate is slightly lower than the spot rate, it is important to note that there is no additional markup or hidden cost layered on top of the transaction. This is an important distinction. Typically, if you link a non-Chinese credit card to Alipay+ or Weixin Pay, a 3% transaction fee applies for payments above RMB 200, which can quietly add up over the course of a trip.

Because this payment feature is already built into the OCBC App, there was no additional setup beyond what I already had as an OCBC customer. I did not need to download another app, register a new account, or worry about linking a Chinese mobile number. Anyone who has tried doing that before will know it often comes with additional verification steps, which is a whole separate topic in itself.

For a short-term holiday in China, having a familiar banking app double up as a payment solution removed a lot of unnecessary friction. Instead of adapting my habits to a completely different payment ecosystem, I could rely on something I already used regularly back home. That made getting around and paying for everyday expenses feel noticeably easier and significantly less stressful.

It also meant I could minimise the amount of cash I carried. Beyond convenience, this reduced the annoyance of ending the trip with leftover RMB that I would otherwise need to change back or keep for a future visit.

Photo Credit: iStock/blanscape