When we retire, we can rely on CPF LIFE to provide us with a monthly payout – for as long as we live – so we never run out of money in our old age. This is what makes CPF LIFE such a unique, powerful and important retirement planning tool for Singaporeans and PRs.

Compared to investments, which can be risky and have unpredictable or uneven returns, CPF LIFE is administered by the government. This makes it virtually risk-free. In addition, while building up towards our CPF LIFE payouts, we earn a minimum of 4.0% (and up to 5.0%) per annum on our Special Account savings and 4.0% (and up to 6.0%) per annum on our Retirement Account savings.

Read Also: [Beginners’ Guide] Understanding CPF LIFE And Your Monthly Payouts When You Retire In Singapore

How Much Do We Need In Retirement?

An average retiree in Singapore who sets aside the Full Retirement Sum (FRS) of $220,400 at age 55 will receive about $1,780 a month from age 65 onwards via CPF LIFE. This compares favourably with the Average Monthly Household Expenditure for households comprising solely non-employed persons aged 65 years and over, which averages $1,384 per household member, or $2,349 per household.

In this article, we explore how much CPF savings we will need in order to receive $3,000 from CPF LIFE during our retirement. While the median take-home salary is $4,860 in 2024, we arbitrarily deducted $1,860 off this figure, given that we no longer need to contribute to CPF (about 20% of wages), and are unlikely to have to account for work-related expenses and other loans such as car, home and income tax during our retirement years.

How Much Do We Need In Our CPF LIFE To Get $3,000 Each Month?

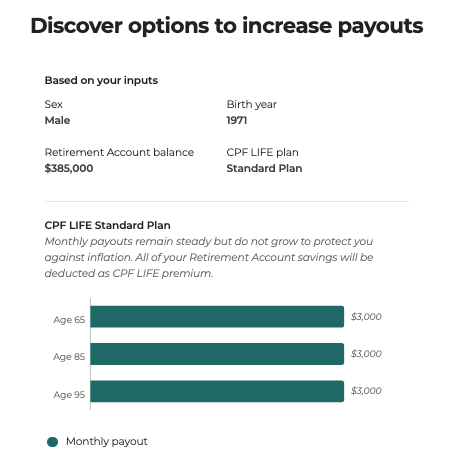

We can try to use the CPF LIFE estimator – a calculator tool by CPF Board – to estimate how much we’re going to need in our CPF Retirement Account (RA) to get a monthly payout of $3,000.

| CPF LIFE | How Much We Need In Our Retirement Account At 55 | Withdrawal Age |

| Standard Plan | $385,000 | 65 |

| Standard Plan | $285,000 | 70 |

* There are also Basic Plan and Escalating Plan that we can aim for.

For someone aged 65 today, they would have needed $385,000 in their Retirement Account (RA) at age 55 to receive a $3,000 CPF LIFE monthly payout. If this same person delays CPF LIFE payouts until they turn 70, they would have only required $285,000 in the Retirement Account at 55.

Given that the FRS is currently $220,400 (as of 2026) at age 55 and will provide about $1,780 a month from age 65 onward via CPF LIFE, the FRS is insufficient to achieve $3,000 a month. However, the Enhanced Retirement Sum (ERS), currently $440,800 for 2026, set aside at age 55, will provide a CPF LIFE payout of $3,440 from age 65 onward.

Thus, for Singaporeans hoping to achieve passive income of at least $3,000 a month in retirement, aiming for the ERS should be your objective to build a stable retirement nest egg.

Saving Beyond The Enhanced Retirement Sum (ERS) In Our Special Account

To work towards that, we can top up our Special Account (SA) via the Retirement Sum Topping-Up (RSTU) Scheme as early as possible. This will help us build additional funds in our CPF accounts.

This pot of money will continue to compound at 4.0% to 6.0% per annum, and we will also receive tax relief each year as we make regular RSTU top-ups.

We can withdraw any excess above the Full Retirement Sum from our CPF OA and SA when we turn 55. While we can withdraw these balances, we don’t have to. We can simply let it continue compounding within the CPF system until we actually retire and start receiving CPF LIFE monthly payouts.

This might seem like a lot of money, but there are many case studies on how we can accumulate $1 million in our CPF accounts by 65. We just need the long-term discipline to save towards our target amount.

Read Also: 1 Million At 65 Using CPF? Here’s The Math Behind The 1M65 Concept

Drawing Down Money From Our Special Account (SA) After 65

For anyone turning 55 this year, they would need about $164,600 more in their Retirement Account at age 55, after accounting for the $220,400 Full Retirement Sum. In total, they would need $385,000 in their RA at age 55 to withdraw $3,000 a month from age 65 onwards.

Read Also: How Much Can You Withdraw From Your CPF Account At Age 55?

Replicating This For Our Own Retirement Needs When We Turn 65

Obviously, the figures stated in the article are for those who turned 65 this year. The figures used will not be applicable to anyone who wants to put these plans into effect today. Nevertheless, the aim is to show how we can go about achieving this – even if it won’t be easy.

If we work toward meeting our target by the time we retire, we can start withdrawing a level more in line with that year’s median salary, rather than the average retiree’s spending.

One great way to kickstart this journey towards saving more money in our Special Account is to read these articles on:

- Hitting $1 million in our CPF account by age 65 (1M65)

- Supercharging this to hit $1 million in our CPF account by age 45 (1M45) (real life example of someone who’s done it)

- (for lack of better word) Turbocharging this to hit $4 million in our CPF account by age 65 (4M65)

- Making your baby a millionaire

Read Also: Here’s What Your CPF Full Retirement Sum Might Look Like When You’re 55

Cover Image by Raymond Quek