When you start working, choosing the best savings account is one of the first financial decisions that you should make. A good savings account should help you earn high interest with minimal inconvenience. In this declining interest rate environment, even the best savings account would not earn you significant interest, so don’t rely on savings alone to grow your money.

Read Also: Best Savings Accounts In Singapore – If You Don’t Want To Keep Jumping Through Hoops

Why Do I Need To Choose A Best Savings Accounts? Don’t We All Already Have One?

Chances are that you already have at least one savings account under your name. So why do you need another one?

For the most part, those who have yet to start work will likely be using a basic account that doesn’t provide many benefits. As a working adult, you now have the opportunity to choose a much better savings account that gives you higher interest rates. But what savings accounts would be for you as a working adult?

Do note that some of these best savings accounts that we have shortlisted require a higher minimum average balance, after which a monthly fall-below fee (of $2 or more) may be charged. So, you want to ensure that you can set aside at least the minimum balance each month.

Read More:

- OCBC 360, OCBC

- One Account, UOB

- BOC SmartSaver, Bank Of China

- Bonus$aver Account, Standard Chartered

- DBS Multiplier Account, DBS

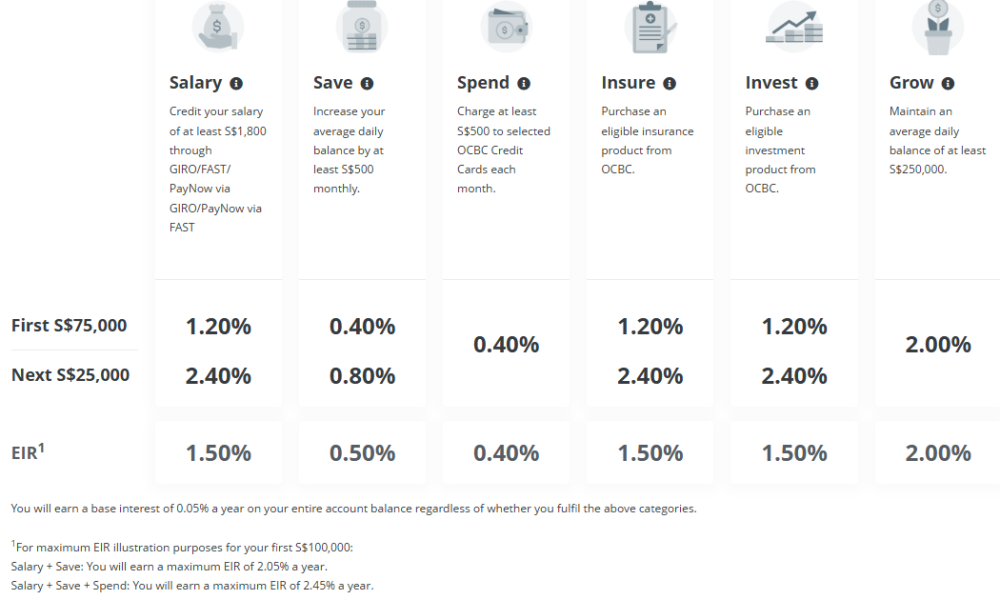

OCBC 360, OCBC

The OCBC 360 is one of the best savings accounts among working adults in Singapore. It has been around for a long time and offers a decent interest rate to its customers.

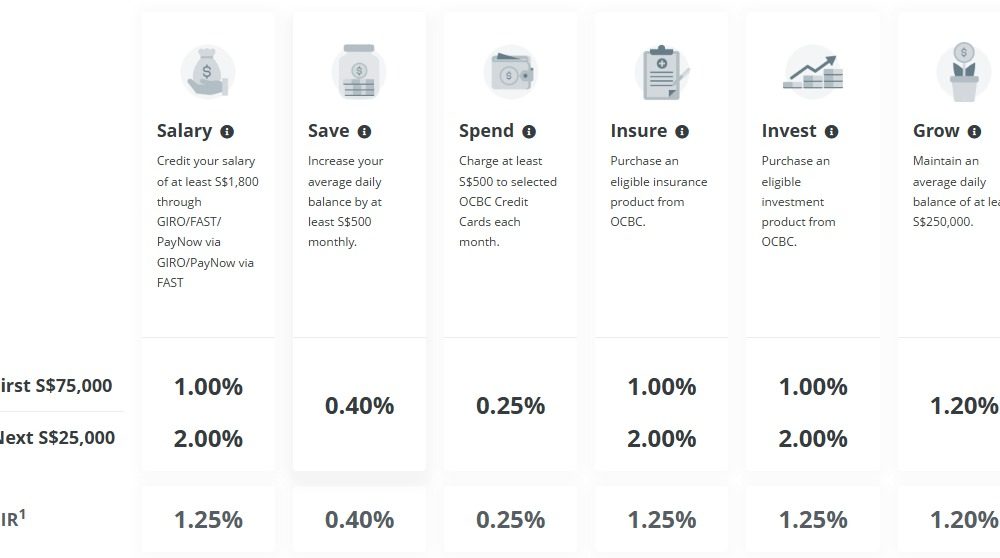

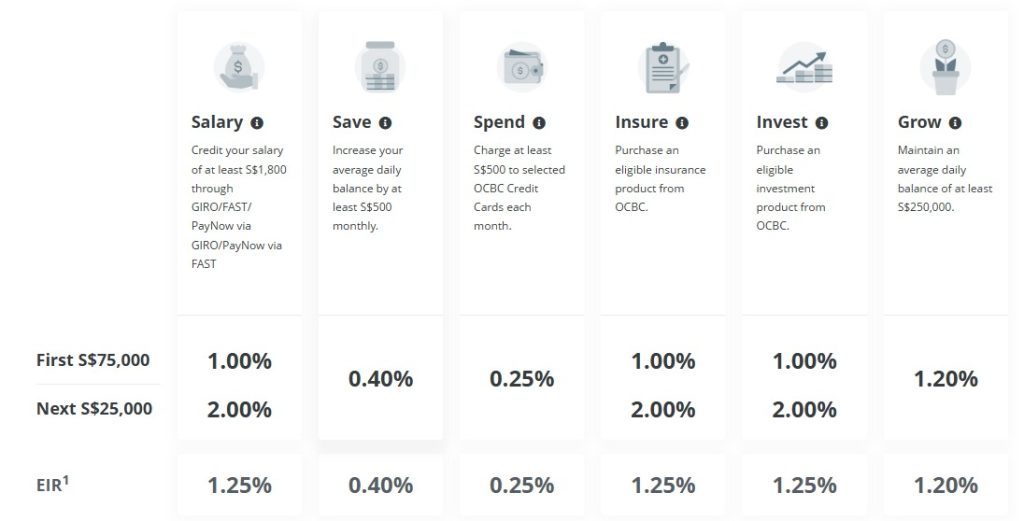

After raising the interest rates in the previous years, OCBC has started to gradually lower the interest rates on its widely popular OCBC 360 savings in line with the broader market trend. Here are the current rates for the first $100,000 of your savings.

- Monthly crediting of salary (min $1,800) through GIRO – 1.00% p.a (first $75,000), 2.00% p.a (next $25,000)[EIR: 1.25%]

- Increase your account balance by at least $500 compared to the previous month – 0.40% p.a (first $100,000)[EIR: 0.40%]

- Charge at least $500 to your OCBC 365 Credit Card each month – 0.25% p.a (first $100,000)[EIR: 0.25%]

- Purchase an eligible insurance product from OCBC – 1.00% p.a (first $75,000), 2.00% p.a (next $25,000)[EIR: 1.25%]

- Purchase an eligible investment product from OCBC – 1.00% p.a (first $75,000), 2.00% p.a (next $25,000)[EIR: 1.25%]

- Grow: Maintain at least $250,000 of the average daily balance in your account and earn 1.20% p.a.

Put simply, if you have savings of up to $75,000, the effective interest rate that you earn will be lower than if you have $100,000. You will enjoy the best interest rates if you have savings of up to $100,000.

Realistic Interest Rate ($75,000 or less): 1.65% (Maximum Interest Rate: 3.65%, excluding Grow)

Realistic Interest Rate ($100,000): 1.90% (Maximum Interest Rate: 4.40%, excluding Grow)

Inclusive of the base interest rate of 0.05%, we put the realistic interest rate at 1.65% for those who have savings of up to $75,000 and a realistic interest rate of 1.90% for those who have savings of $100,000 because we don’t think it makes sense for a person to buy an insurance or investment product, to earn bonus interest for a period of 12 months. Even if you happen to purchase these products, note that the bonus interest rate won’t be paid perpetually.

One thing we like about the OCBC 360 Account is that bonus interest in each area can be earned independently. This means you do not need to complete any particular area to be eligible for the bonus interests in other areas.

Who Should Apply: Young working adults who just received their first paycheque can consider getting an OCBC 360 account and crediting their salary to it. By doing so, they immediately enjoy at least 1.0% p.a. interest on their savings, on top of the base interest rate of 0.05%. They can easily earn another 0.25% just by spending $500 a month on selected OCBC credit cards each month.

If you have savings of between $75,000 and $100,000, the OCBC 360 account offers a higher effective interest rate.

Read Also: OCBC 360 Account – Here’s How You Can Maximise The Interest You Earn On This Savings Account

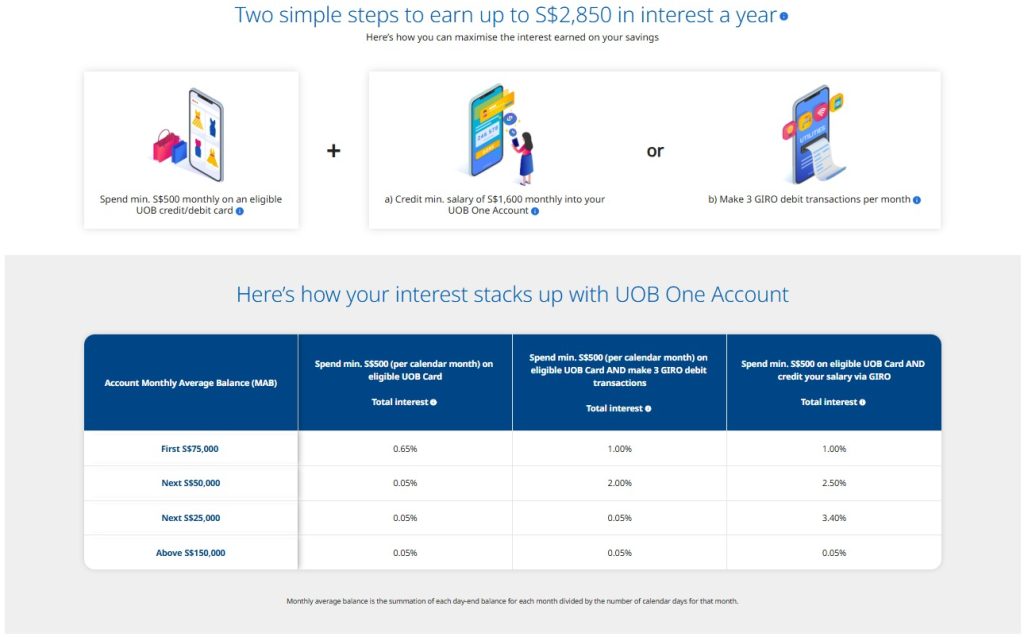

One Account, UOB

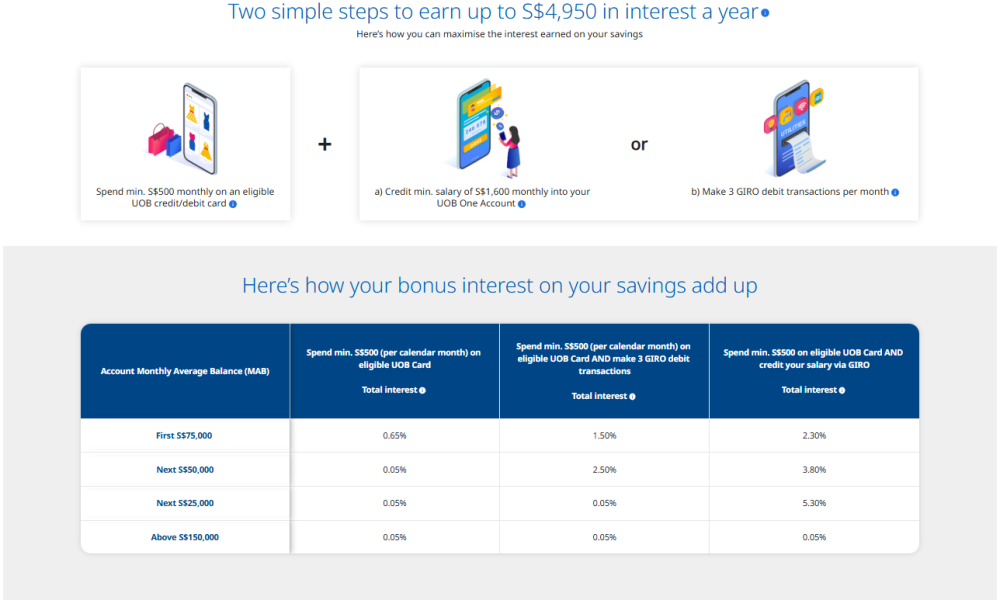

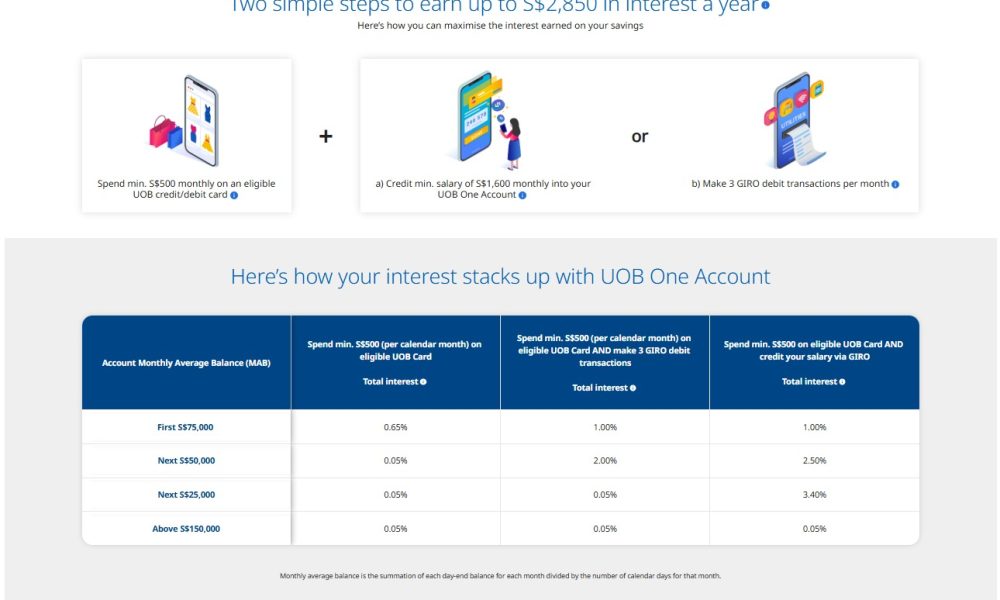

For the past few years, the UOB One Account has been the main competitor to OCBC 360 as one of the best savings accounts in Singapore. The interest rates are somewhat similar, though the UOB One Account works slightly differently. We will let the table below do the explaining.

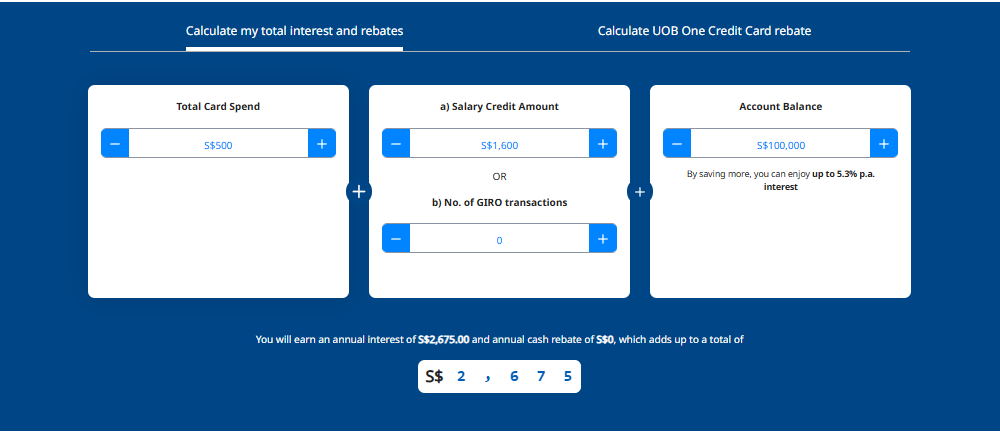

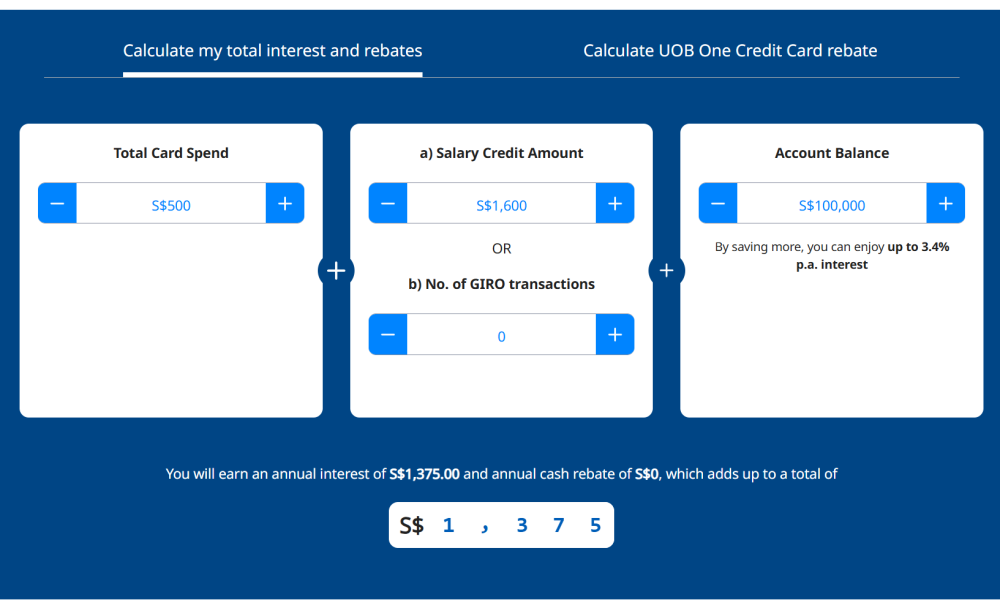

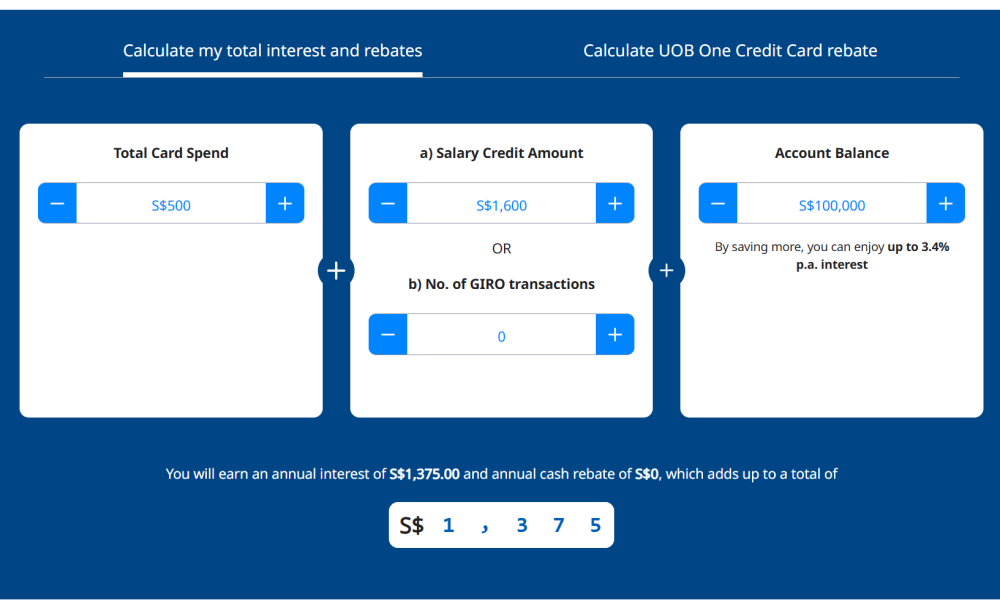

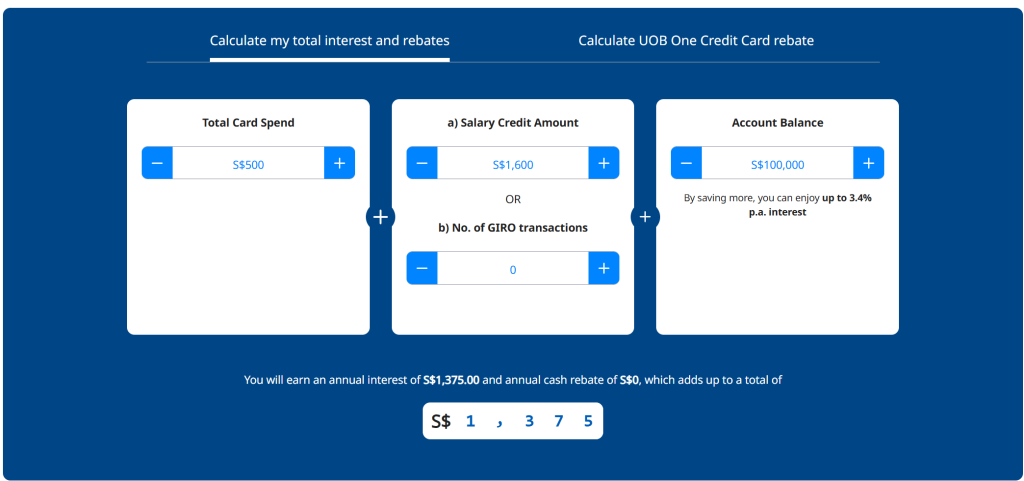

An individual with savings of $100,000 who can meet the criteria of 1) minimum spending of $500 plus 2) credit his salary (minimum $1,600), stands to earn an effective interest rate (EIR) of 1.37% (interest of $1,375). This excludes the cash rebates the individual gets on their UOB credit card.

Minimum Credit Card Spending + 3 GIRO Transactions

In lieu of a salary credit of at least $1,600 per month, the individual can also choose to make 3 GIRO debit transactions each month. Assuming savings of $100,000, he will get an EIR of about 1.25%.

This also means that the bonus interest you enjoy is higher when you credit your salary (minimum of $1,600 monthly) than by making 3 GIRO debit transactions monthly. Also, bonus interest payable for the 3 GIRO transactions option is up to the first $125,000 of your deposits, while bonus interest for salary credit is up to the first $150,000 of the deposits. Thus, if you have savings of up to $150,000, choose to credit your salary instead.

Best Case Scenario For UOB One Account

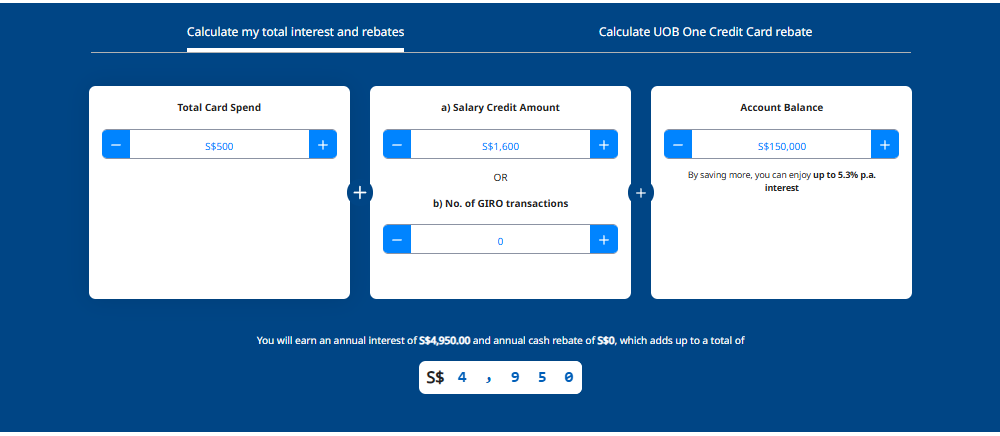

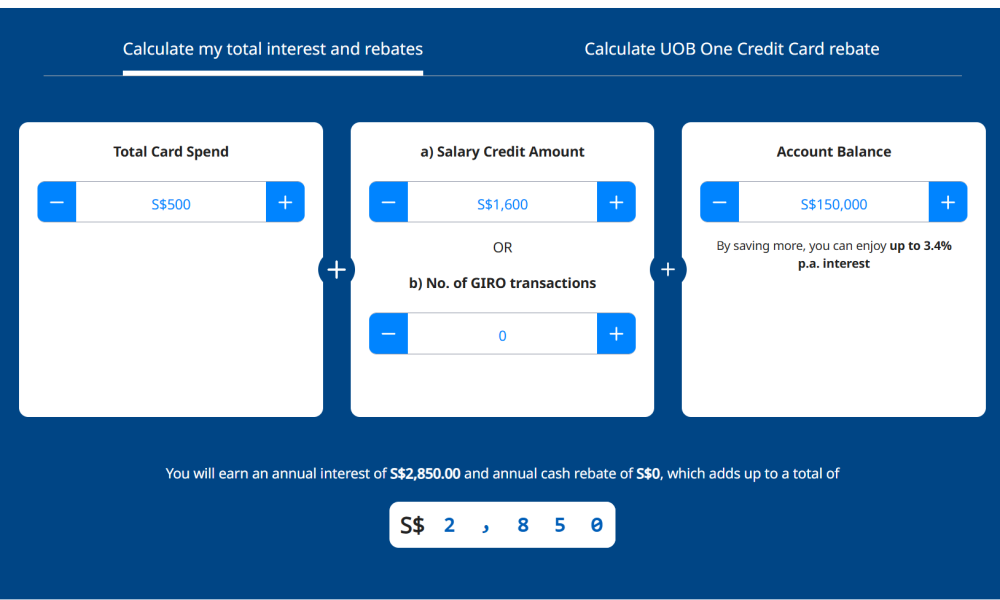

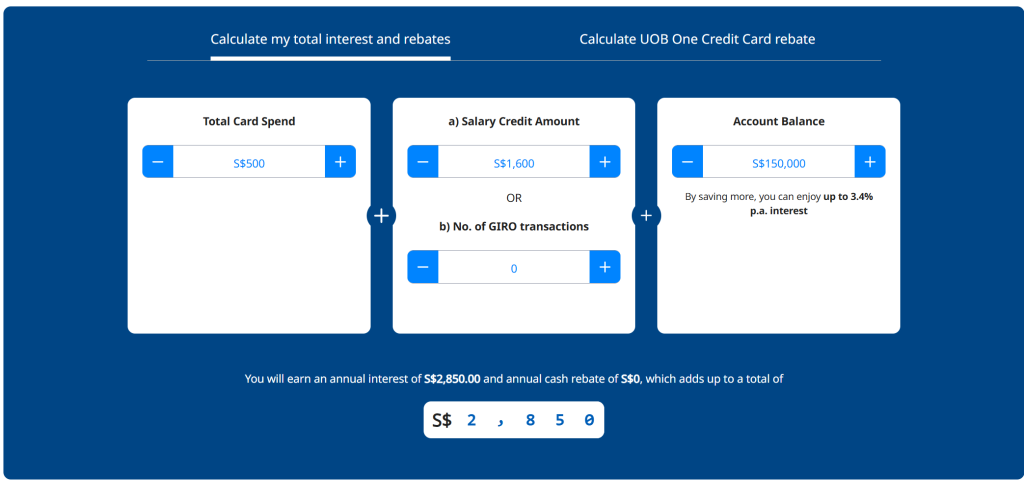

The best case scenario for the UOB One Account is to have 1) $150,000 in savings, 2) Spend a minimum of $500 each month on an eligible UOB Card (e.g UOB One Card) and 3) credit your salary of at least $1,600 a month.

With this, you earn $2,850 a year in interest (or $237.50 a month), which translates to an EIR of 1.90% p.a.

A few things to note.

Firstly, to qualify for bonus interest, you have to achieve a minimum spend of at least $500 on your UOB One Card (which by itself, is a great card to own anyway based on the reviews from our readers) and/or other selected UOB cards. Once you have done that, you would have met the first criteria for bonus interest.

Who Should Apply: Assuming you have $150,000, the UOB One account gives an effective interest rate of 1.90%, which is decent.

In return, you only need to spend $500 on the UOB One card and credit your salary (minimum: $1,600 per month). Compared to the OCBC 360, fewer actions are required, yet you earn a higher interest.

The catch is that you must spend $500 on the UOB One Card or any other eligible UOB card to qualify for any bonus interest. Otherwise, you don’t get any interest, even if you fulfill the other requirements. Also, you want to have about $100,000 to $150,000 in savings. For instance, if you only have $15,000 in savings, then your effective interest rate will be about 1.0%.

Read Also: The Battle For High Interest: Why I Chose To Switch To The UOB One Account

BOC SmartSaver, Bank Of China

According to BOC, we can earn up to 4.60% on the first $100,000 of our account, and up to 0.60% for account balances above $100,000 to $1,000,000. Here’s how it works.

Here are some of their perks. Here is the bonus interest you can earn on the first $100,000 of your savings.

- Crediting of salary (min: $3,000) – 0.50% p.a.

- Credit card spend (min: $750) – 0.60% p.a. If credit card spend is $2,500 or more, the interest rate is 0.90% p.a.

- Pay 3 bill payments (min $30 each) – 0.10% p.a.

- Bonus Interest – If you fulfill at least one of the requirements above, you will receive 0.50% p.a. on funds above $100,000, subject to a maximum of $1,000,000.

There is also a Wealth Bonus Interest of 3.0% p.a. for 12 consecutive months for those who have purchased an eligible product. However, we don’t think it makes sense to deliberately buy an eligible product to earn the bonus interest.

Source: BOC

Realistic Interest Rate: With a prevailing interest rate of 0.10% on the entire account balance, most people can easily expect to earn at least 1.30% p.a. based on the usual criteria being met (e.g. crediting of salary, spending $750 on credit cards, and making at least 3 GIRO bill payments). For higher earners who can spend at least $2,500 on their BOC credit cards, and perform at least 3 bill payments of at least $30 each month via GIRO or BOC Internet Banking/BOC Mobile Banking Bill, can reasonably achieve an interest rate of 1.60% .

Who Should Apply: While 1.30% on the first $100,000 is attractive for meeting the minimum requirements the BOC SmartSaver becomes a strong contender if you have savings between $100,000 to $1 million, offering an additional 0.60% interest on the excess amount.

Read Also: We Said BOC Had The Best Savings Accounts In Singapore… And Got Punk’d

Bonus$aver Account, Standard Chartered

Another savings account that cannot be ignored when discussing the best savings accounts for working adults in Singapore is the Standard Chartered Bonus$aver Account.

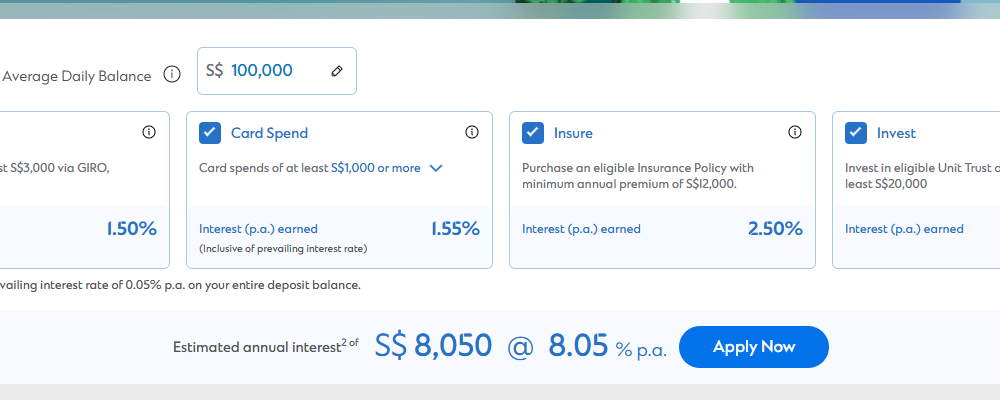

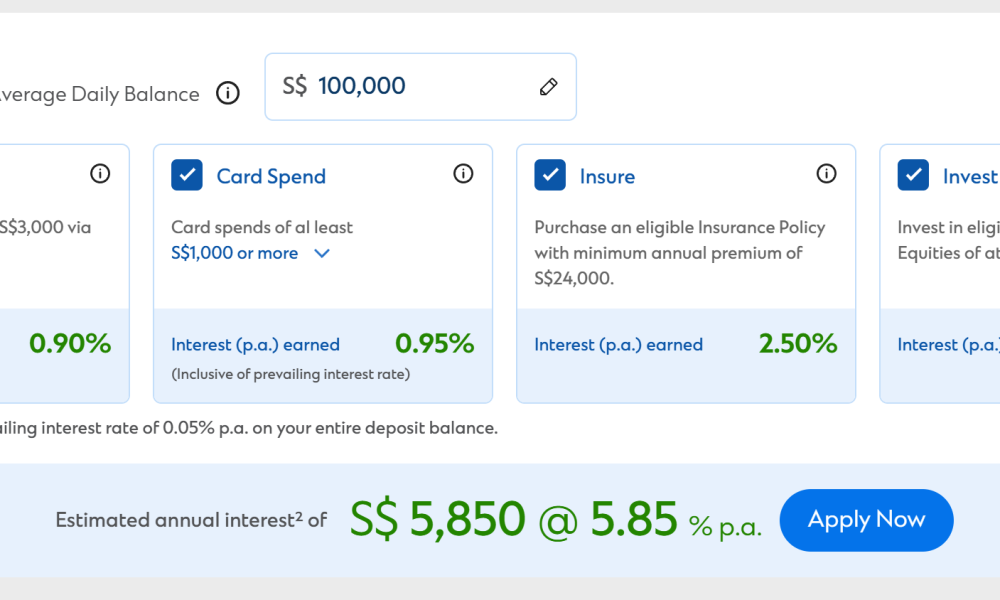

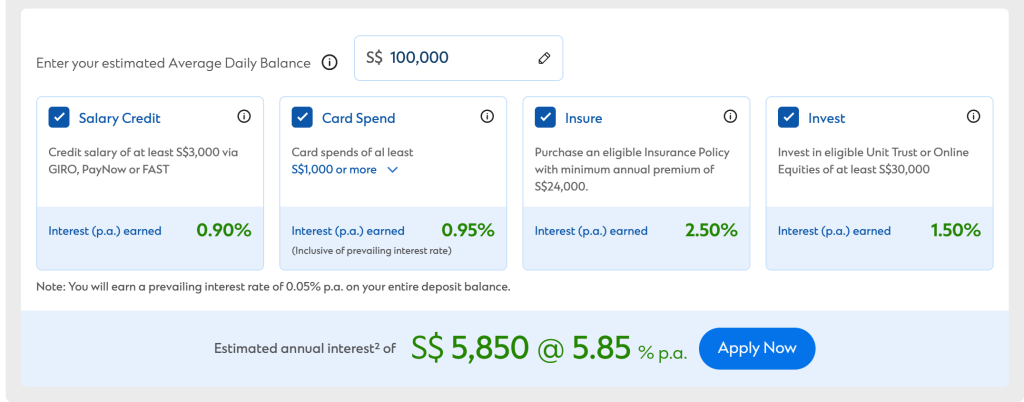

On paper, the Standard Chartered Bonus$aver Account gives an impressive effective interest rate of 5.85% p.a.

* The 0.95% interest rate shown on card spend from the screenshot above includes the prevailing interest rate.

# 1 Card Spend – up to 0.95% – inclusive of prevailing interest)

If you meet the minimum card spend, you will earn bonus interest on the first $100,000 of your deposit balance.

If you have $100,000 and charge a minimum of $1,000 each month on your Bonus$saver card linked to a Bonus$saver account on qualifying retail transactions, you can earn an interest of 0.95% p.a.

# 2 Salary Credit – 0.90%

By crediting a monthly take-home salary of S$3,000 into your Bonus$aver account, you will earn a bonus interest rate of 0.90% p.a.

# 3 Invest & Insure (1.50% & 2.50% respectively, total of 4.0%)

If you have invested in an eligible unit trust (minimum subscription sum: S$30,000) or purchased an eligible insurance policy (minimum annual premium: S$24,000) through Standard Chartered, you will earn an additional interest rate of 1.5% and 2.5% p.a. respectively. This means you can potentially earn up to 4.0% if you invest and insure with Standard Chartered.

In total, you can earn Card Spend (up to 0.95%) + Salary Credit (0.90%) + Invest (1.50%) + Insure (2.50%) = 5.85% p.a. from the Bonus$aver account.

Do note that the bonus interest above applies to your first S$100,000 deposit balance.

Realistic Interest Rate: If you spend a minimum of $1,000 on your Bonus$aver card and credit your monthly salary (minimum $3,000) you will earn a basic interest of 1.85%.

We don’t think investing or insuring in a product specifically to earn the additional 4.0% annually makes sense.

Who Should Apply: The main thing for the Bonus$Saver account is that your salary credit needs to be a minimum of $3,000 per month. You can apply here if you wish to enjoy attractive perks.

DBS Multiplier Account, DBS

The DBS Multiplier account could be considered one of the best savings accounts, but it works differently from the other savings accounts mentioned in this article.

Rather than give account holders bonus interest based on each of the requirements that they meet, bonus interest is given based on the total eligible transactions completed each month. Bonus interests can be earned on the first $100,000 of savings.

To start, you need to credit your income. Then, you need to transact in one or more categories.

For example, if your take-home salary is $3,500 and you make a credit card spend of $500. You would qualify for the Income + 1 category with a total eligible transaction value of $4,000. This earns you 1.8%

If your income is $10,000 a month, you spend $3,000 on a credit card, and you have a home loan instalment of $2,000 a month, you would qualify for the Income + 2 categories with a total eligible transaction value of $15,000. This earns you 2.2%.

In other words, you need to use the Multiplier account for 1) monthly crediting of income (no minimum amount and this can be your salary credit, dividend credit, annuities like CPF LIFE) and 2) do at least one of the following

– Credit card/PayLah! retail spend with DBS/POSB

– Home loan instalment with DBS/POSB

– Insurance with DBS/POSB

– Investments with DBS/POSB

There are no minimums for each category, but to receive bonus interest, your total monthly eligible transactions must total $500 or more.

The DBS Multiplier account gives you an interest rate based on two factors. 1) The volume of your total eligible transactions each month and 2) the number of categories where you make an eligible transaction each month

In a best-case scenario, if I have total eligible transactions of more than $30,000 a month (e.g. $20,000 salary, $5,000 credit card spend, $5,000 home loan repayment and make an investment through DBS), I can earn an EIR of 4.10%.

Who Should Apply: Those who can’t meet the minimum salary or credit card spending requirement for other savings accounts can consider using the DBS Multiplier account since it does not impose any minimum requirement in each of these areas.

Alternate Track For DBS Multiplier Users: PayLah! Retail Spend

The above outlines the most common (and advertised) way to earn bonus interest using DBS Multiplier. An alternate track based on PayLah! Retail spending has been added, presumably for younger individuals without a credit card, insurance, home loan, or investment with DBS. Here’s how it works:

Simply make any Credit Card/PayLah! Retail spend (no minimum amount) and you enjoy 1.50% p.a if you are a customer below the age of 29.

Read Also: I Just Graduated From University. Here’s Why I Decided To Use The DBS Multiplier Account