When it comes to financial planning and buying insurance in Singapore, there are many areas to think about. One of the important questions that we have to answer is the type of hospitalisation plan we need.

Though this appears to be a broadly simple question, knowing the details of what it means is important. Many Singaporeans may not be fully aware of the coverage that they have and even how much they are paying for the coverage they are receiving. This could lead to them either being over-insured or under-insured.

In this article, we will explain the basics of what Singaporeans need to know when upgrading your existing MediShield Life to an Integrated Shield Plan. We will also pose you some questions that you should ask yourself, or a financial planner you are working with, before making your decision.

MediShield Life And Private Integrated Shield Plan, What Are The Differences?

All Singaporeans and PRs are automatically covered under MediShield Life, Singapore’s basic health insurance plan. Coverage is provided regardless of age or pre-existing conditions.

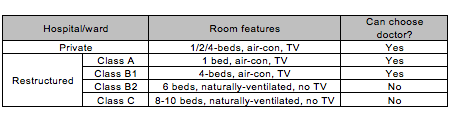

You may refer to the table below for a general comparison of hospitals and wards:

Coverage for MediShield Life is pegged to the treatment cost in Class B2 and C wards in public hospital. A patient who seeks treatment in these wards would have his or her bill largely covered by MediShield Life, less the deductible and the co-insurance component. The co-payment (i.e. deductible and co-insurance) amount can be paid using Medisave and/or cash.

For those without an IP, if the patient seeks treatment at higher-class A and B1 wards in public hospitals or at private hospitals, the payout under MediShield Life would cover only fraction of the total bill. That means the patient would need to pay a bigger balance sum using his or her own Medisave Account or cash.

Due to the hefty costs patients may incur in higher-class public hospital wards or at private hospitals, many Singaporeans prefer upgrading their MediShield Life to an Integrated Shield Plan. According to a report by the Straits Times, about six in 10 people in Singapore have an Integrated Shield Plan.

Such a plan allows them to enjoy further coverage at A/B1 class wards or at private hospital without worrying about a large bill wiping out their Medisave or cash savings.

Before you upgrade to an Integrated Shield Plan, here are some questions that you should consider asking yourself first.

#1 What Type Of Coverage Do You Want?

A simple question to ask yourself before you buy any products or services is whether you are paying for something that you will be using.

The same logic extends to buying an Integrated Shield Plan. An Integrated Shield Plan provides you with further coverage for treatment in private hospitals and Class A and B1 wards in public hospitals. You should aim to buy the type of coverage you would use if you ever require hospitalisation.

For example, Income, one of the Integrated Shield Plan insurers, offers its Enhanced IncomeShield that provides policyholders with higher tier coverage. Premium rates depend on the level of coverage that you purchase.

Income’s Enhanced IncomeShield Premium for Singapore Citizens or Permanent Resident – Age 21 to 30

| Type Of Coverage | Annual Premiums |

| Up To Class B1 | $57 ($62 for Permanent Resident) |

| Up To Class A | $71 |

| Up To Private Hospital | $234 |

Source: Income

You should pay for the coverage you want. If you don’t see yourself using a private hospital in the event that you are hospitalised, then opting for a Class A or B1 coverage at public hospital is good enough. If you want private hospitalisation coverage, then you should purchase a plan with higher coverage.

At the end of the day, it’s a matter of balancing between what you want against how much premiums you are able to afford.

#2 How Much Will You Be Paying In The Future?

Premiums for your Integrated Shield Plan will also increase as you age. This is similar to how MediShield Life works.

One mistake people make when buying insurance is that they only take into consideration their cost today while disregarding affordability down the road. Policyholders should always take into consideration future costs when buying an insurance policy.

Do not just buy a policy today because you can afford it today. Consider how much it will cost you as you become older. Be mindful that as you become older, the likelihood of being hospitalised also increases so terminating your Integrated Shield Plan coverage when you become older isn’t really a great idea. Instead, you should consider the premiums in the long-term before you purchase a policy. While there is option to downgrade your IP plan later for more affordable premiums, you will not be refunded the price difference in premiums previously.

#3 How Much Of The Premiums Is Payable Through Medisave?

When buying an Integrated Shield Plan, you can opt to pay your annual premiums using your Medisave. That’s what most people would do.

The amount you can use from Medisave each year to pay for your premium depends on your age.

| Age | Additional Withdrawal Limits (AWLs) |

| 1 – 40 | $300 |

| 41 – 70 | $600 |

| 71 & Above | $900 |

For some Integrated Shield Plans, such as the Enhanced IncomeShield, premiums are kept affordable such that policyholders do not need to provide any cash outlay till they are 51 and above. That’s because Income offers one of the most affordable premiums in Singapore. You can check out their rates in this link.

#4 What’s The Claim Limit (If Any) For Your Shield Plan

You may want to note that for MediShield Life and some Integrated Shield Plans, there are claim limits set in place for specific treatments. It may be good to know what these specific limits are before you commit to a plan so that you are not caught by surprise only after seeking treatment.

For MediShield Life, there is a maximum claim limit of $100,000 per policy year. That means in the event of some catastrophic incident, there is chance that the hospital bill may exceed the claim limit. It’s improbable but not impossible.

If you purchase an Integrated Shield Plan, the limit will be a lot higher. For example, the Enhanced IncomeShield Preferred Plan provides a claim limit of up to $1,000,000 per policy year.

Thus, knowing your policy year claim limit is important because you do not want to exceed your limit without being aware of it.

#5 Do You Need A Rider?

Similar to MediShield Life, coverage provided at higher-class wards does not mean those hospitalisation bills incurred are fully paid for. All integrated shield plans still include deductibles and co-insurance.

If you want complete coverage so that you do not have to pay for deductibles and co-insurance, you have the option of purchasing a separate rider. This additional rider component may cost a few hundred dollars or more each year and must be paid in cash.

Rider Premiums for Enhanced IncomeShield Preferred Plan (Private Hospital Coverage)–

Age 19 to 30

| Rider | Annual Premiums |

| Assist Rider | $190 |

| Plus Rider | $306 |

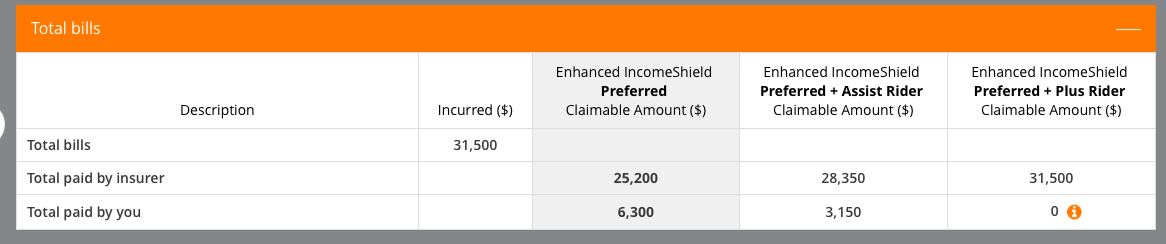

Here’s an example of how your actual bills may differ depending on whether or not you have a rider.

Source:

Source:

As seen above, without any rider, a private hospital bill of $31,500 would translate into a final bill of $6,300 for the patient after deductibles of $3,500 and the co-insurance payment of $2,800 (10% of $28,000).

Policyholders can choose to buy a rider if they do not want to worry about the deductibles and co-insurance cost components.

Choose A Suitable Plan For Your Needs Today

Though an Integrated Shield Plan is one of the simplest forms of insurance to buy in Singapore, you can see that there are still many considerations to think about.

If you want to better understand how they impact you and your preferences, Income has set up a website to provide you a step-by-step guide on the type of Shield Plan that would suit you best.

Source:

Source:

In addition, the web portal also tells you if there are any gaps in your coverage that you may have missed out.

If you are the type of person who needs to understand for yourself what your healthcare needs entail, to find out if you are over-insured or under-insured.

If you are the type of person who needs to understand for yourself what your healthcare needs entail, to find out if you are over-insured or under-insured.

This article was written in collaboration with Income. All views expressed in the article is the independent opinion of DollarsAndSense.sg

Bonds and Fixed Income

StashAway Income Portfolio: How You Can Earn 4.6%* Dividends From Your Investments Each Year