This article was written in collaboration with Tiger Brokers (Singapore). All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, are purely for informational purposes, and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions, and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

The Supplementary Retirement Scheme (SRS) is one of the key ways we can plan for our retirement in Singapore. Unlike CPF, which is compulsory for Singaporeans and PRs, SRS is voluntary and open not just to locals, but also to foreigners working in Singapore who do not receive CPF contributions. This makes it a flexible tool for working adults in Singapore who want to set aside money for their future.

One of the main benefits of contributing to SRS is the tax savings we enjoy.

For example, assuming no tax relief, someone earning $120,000 a year will pay a personal income tax of $7,750 for YA2025. By contributing $10,000 to their SRS account, they can reduce their income tax to $6,800, saving them $950.

| Scenario | Chargeable Income | Income Tax Payable (YA2025) | Tax Saved |

| No SRS Contribution | $120,000 | $7,750 | – |

| With $10,000 SRS Contribution | $110,000 | $6,600 | $1,150 |

Based on the above scenario, if we think of it in investment terms, that’s like getting an immediate return of 11.5% since they are saving $1,150 (in tax) for a $10,000 SRS top-up.

However, making SRS contributions is only the first step. Simply leaving our SRS savings untouched in the SRS account would do little for our retirement, given that it earns only a nominal interest rate of 0.05%. To truly benefit from the scheme, we need to not only enjoy tax savings, but also invest our SRS funds so that our savings can grow and generate higher long-term returns.

What Can We Invest Our SRS Savings In?

The good thing about SRS is that it does not lock us into just one type of product. Instead, we can invest in a wide range of investment options depending on our goals, risk appetite and investment horizon.

Some of the products we can invest our SRS funds in include:

- Fixed deposits

- Unit trusts and mutual funds

- Singapore Government Securities (e.g. SGS bonds, T-bills) and other retail bonds listed on the SGX.

- Stocks, REITs and ETFs listed on SGX

For many everyday investors who want to grow their savings, investing in asset classes such as stocks, REITs, and ETFs is one way to grow their retirement savings. This is particularly true if we are self-directed investors who want to make our own investments. Investing through the SGX is easily accessible, and allows us to take part in the long-term growth of companies and markets.

To invest our SRS savings in SGX counters, we need a brokerage account that supports SRS investing. One such example will be the Tiger Brokers Cash Boost Account. Available through the TIGER TRADE App or on desktop, this is a trading limit account that is created specifically for investors in Singapore. The Cash Boost Account allows us to fund our investments not only with cash but also with our SRS (and CPF) savings.

How The Cash Boost Account Works

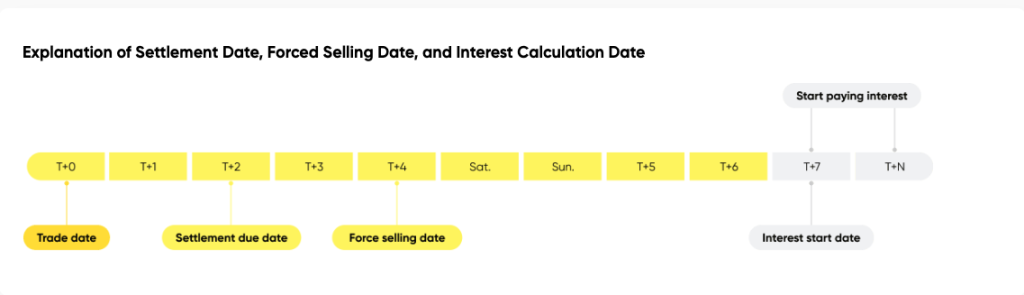

Similar to most online brokerage accounts, trading through the Cash Boost Account is straightforward. We can buy and sell stocks, ETFs and REITs, just as we normally would. The key difference lies in how settlement works.

Under a typical brokerage setup, we would need to fund our trading account first before buying anything. For example, when we purchase a stock, the money is deducted from our trading account to pay for the investment.

The Cash Boost Account works slightly differently. Clients can make their investment first and settle the payment 1–2 days later, depending on the market’s settlement requirements. If we sell the shares before the settlement date, we pay the difference between our buy and sell trades.

This flexibility allows us to observe the price movement, and then decide whether to hold the shares long term or exit the position.

| Scenario | What Happens | When Payment Is Required |

| Buy → Sell before settlement date | Buy → Hold shares past the settlement date | Payment to be made if there is a negative price difference. |

| Buy → Hold shares past settlement date | We keep the shares in our portfolio. | Full payment required before forced-liquidation date. |

This means we receive (or pay) the difference between our buy and sell prices. So, if the share price rises, we earn a profit. If it falls, we will need to cover the shortfall. Brokerage fees will also be included in the transaction.

Cash Boost Account Can Be Used For Both Long & Short-Term Positions

Of course, like most regular trading accounts, we also have the option to hold the stocks for the long term rather than closing the position.

To do this, we make a full cash payment before the forced-liquidation date.

Cash Boost Account settlement timeline for Singapore & Hong Kong markets

*Please be aware that any outstanding shortfall is subject to interest charges as follows:

– US/CN Market: Interest charges will begin accruing from the 7th trading day after the buy trade.

– SG/HK Market: Interest charges will begin accruing from the 8th trading day after the buy trade.

It is also worth noting that the Cash Boost Account is not limited to the Singapore markets. We can also trade stocks and ETFs listed in the US, Hong Kong, China A-shares, in addition to Singapore. While the concept of buying a stock and freely choosing when to hold or sell it later does not apply to SRS investing, we can use SRS funds to invest in SRS-eligible products, for example, SGX-listed stocks and ETFs.

Integrating SRS Into Our Overall Investment Plan

Ultimately, investing our SRS savings shouldn’t be viewed in isolation, as it forms just one part of our broader investment strategy, alongside the cash we invest and the CPF savings we continue to build over time.

Each serves a different purpose. Our CPF provides stability and predictable returns, while our cash portfolio gives us the flexibility to invest in opportunities as they arise, with no restrictions. Our SRS investments, meanwhile, help us capture long-term market growth in Singapore, while reducing our tax burden today.

With the Cash Boost Account, we can use our SRS funds more strategically, as part of a balanced approach alongside our cash and CPF investments to build a stronger foundation for retirement.

From now till 31 December, complete your first Cash Boost Account trade with a trade amount of ≥ SGD 1,000* to get S$688* worth of Cash vouchers on Tiger Brokers! For more information, visit the promotion page here.

*T&Cs apply. For more info on Cash Boost Account and Fees: https://www.tigerbrokers.com.sg/commissions/fees.

Not financial advice. Investment involves risk. Cash Boost Account enables you to make purchases using credit limit, allowing you to buy beyond your current available funds and may potentially incur losses exceeding your account balance. Please make decisions according to your own risk tolerance. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Image Credit: iStock/Panuwat Dangsungnoen