For most Singapore residents, CPF is part of our lives. It is something that follows us through our working years, shaping how we pay for big-ticket items like our home, and how we prepare for our retirement nest egg.

When it comes to determining whether we are on track with our retirement plans, CPF provides two important reference points. The Full Retirement Sum (FRS) helps us gauge whether we may have set enough for monthly payouts in retirement, while the Basic Healthcare Sum (BHS) indicates whether our Medisave savings are sufficient for future medical costs.

These two figures are not just abstract CPF milestones. They are meant to answer a very practical question most of us worry about: will our CPF savings be enough to support our retirement lifestyle and healthcare needs?

What The Full Retirement Sum Means For Your Retirement Income

As of 2026, the Full Retirement Sum (FRS) is set at $220,400. This amount isn’t arbitrary but carefully calibrated to provide CPF members with a reasonable level of financial security in retirement through lifelong monthly payouts under CPF LIFE.

For example, if you turn 55 in 2026 and manage to set aside the full FRS, you can expect to receive roughly $1,780 a month from age 65 under the CPF LIFE Standard Plan.

Source: CPF

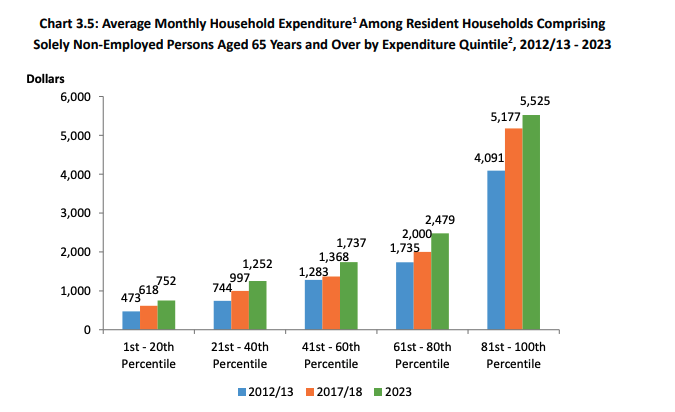

Interestingly, this figure isn’t far off from what seniors actually spend. Data from SingStat shows that resident households with at least one non-working person aged 65 and above spend an average of $1,737 per month, in the 41st to 60th percentile.

Source: Singstats

Why The FRS Keeps Going Up Over Time

It’s important to note that the FRS gradually increase over time. This is intentional. Inflation slowly eats away at purchasing power, so the FRS is adjusted upward to make sure future retirees aren’t left short. This means someone who is 45 today will face a higher FRS when they reach 55.

There are limits on how you can top up your CPF along the way. If you’re under 55, voluntary top-ups are capped at the FRS for your Special Account. Your regular CPF contributions from work, however, can still push your balance beyond the FRS over time.

Hitting the FRS is not just about meeting a target. It is also about the interest you earn along the way. The Special Account pays a base interest rate of 4 per cent per year, which is significantly higher than most low-risk savings options.

If you manage to reach the FRS before 55, that 4 per cent can do a lot of the work for you. For example, it helps your savings keep pace with future FRS increases even if you stop working or no longer make CPF contributions.

For example, someone who has set aside $220,400 in their Special Account in 2026 would see this grow to about $229,216 in 2027 purely from interest. That amount is already higher than the 2027 FRS of $228,200.

In practical terms, reaching the FRS early puts your retirement savings on a kind of autopilot. Even without additional contributions, you are likely to stay on track with future FRS requirements.

Achieving The Basic Healthcare Sum (BHS)

The Basic Healthcare Sum (BHS) is meant to cover basic subsidised healthcare needs in old age, and it also caps how much you can hold in your MediSave account. Like the Special Account, the BHS isn’t a fixed number. It rises over time to keep up with inflation and higher healthcare costs. As of 2026, the BHS is $79,000.

MediSave earns a base interest rate of 4 per cent a year, and that interest matters more than many people realise. For one, it can be used directly to pay for healthcare-related expenses. This includes insurance premiums for MediShield Life, CareShield Life, and approved supplementary plans, as well as medical treatments and health screenings when needed.

To put this into perspective, someone with $75,000 in MediSave would earn about $3,000 in interest per year. That alone can cover a large portion of annual insurance premiums, easing the need to rely on cash.

Over time, the interest also helps you grow towards the BHS, even if your contributions slow later in life. As with the Special Account, compounding does a lot of quiet work in the background.

Read Also: How Much Medisave Would A Healthy Adult Use Each Year?

What Happens After You Hit The BHS

The real change comes once you have actually hit the BHS. From that point on, you can’t add more to MediSave. Any CPF contributions from work that would normally go there are instead channelled into your Ordinary Account.

For many people, this is a welcome shift. More money flowing into the Ordinary Account means more flexibility, whether that’s servicing a home loan or building up retirement savings. In that sense, reaching the BHS gives your CPF contributions more room to work elsewhere.

The Benefits of Reaching the FRS and BHS Early

Reaching both the Full Retirement Sum (FRS) and the Basic Healthcare Sum (BHS) early, say, in your 40s, can take a real weight off your shoulders.

On the retirement side, hitting the FRS early locks in a baseline income level for later life. Thanks to the Special Account’s 4.0% annual interest, your savings can usually keep up with future increases in the FRS on their own. That reduces the pressure to keep topping up your CPF or worry about whether your cash investments will deliver.

Reaching the BHS early offers a different kind of relief. Once you have hit the cap, more of your CPF contributions flow into your Ordinary Account instead. That can help with housing loans or give you more for your retirement. At the same time, your MediSave balance continues earning interest that can offset insurance premiums and medical bills, especially during periods when you are no longer working.

Read Also: What Happens To Your CPF Contributions After You Hit Full Retirement Sum (FRS)?

Photo Credit: DollarsAndSense/Raymond Quek