Your CPF is one of the most important financial assets you have for your retirement, housing and healthcare. Its versatility allows you to optimise the way you use your CPF funds, but you can also hurt your long-term financial security by making the wrong decisions.

Here are 8 CPF moves you may want to avoid, especially if you don’t have great reasons to make those moves in the first place. As a caveat, all of these moves can also be made for the right decision, based on your personal circumstances and reasons, so make sure you’re making them for the right reasons.

#1 Don’t Transfer From OA to SA – If You Haven’t Bought a Home

Moving your Ordinary Account savings to your Special Account gives you 1.5% p.a. more in interest return. Your OA only earns 2.5% p.a., while your SA balances earn 4.0% p.a.

But doing this before you buy a home can backfire, because it is irreversible. When you eventually want to buy a home, you might regret hollowing out your OA balances as it limits your housing options. This can be much more significant than the benefit of earning $150 (i.e. 1.5% p.a.) a year more on every $10,000 you transfer to your SA.

Even if you’ve bought a home, but intend to upgrade in the near-term, the same argument applies. Similarly, if you’ve crunched the numbers and don’t think you’ll need that much, either for a new home or for upgrading your home, it’s always good to have the option to use more OA.

It’s also noteworthy that you can use your OA to pay for home purchase-related expenses such as legal fees, stamp duty and survey fees.

#2 Do Not Leave Your OA Funds Idle – After You’ve Bought Your Home

This is the flipside of the argument after you’ve bought your home. Obviously, consider your upgrading aspirations before making any moves.

Leaving your OA funds alone means you continue to earn 2.5% p.a. But, you can now start considering more strategic, long-term uses for your OA.

Making partial transfers from your OA to SA to earn 1.5% more per year can make sense at this point. You can also invest your OA (above the first $20,000) via the CPF Investment Scheme (CPFIS). This can boost your return from 2.5% p.a. to 4% p.a. in your SA and over 10% p.a. on average in global equities.

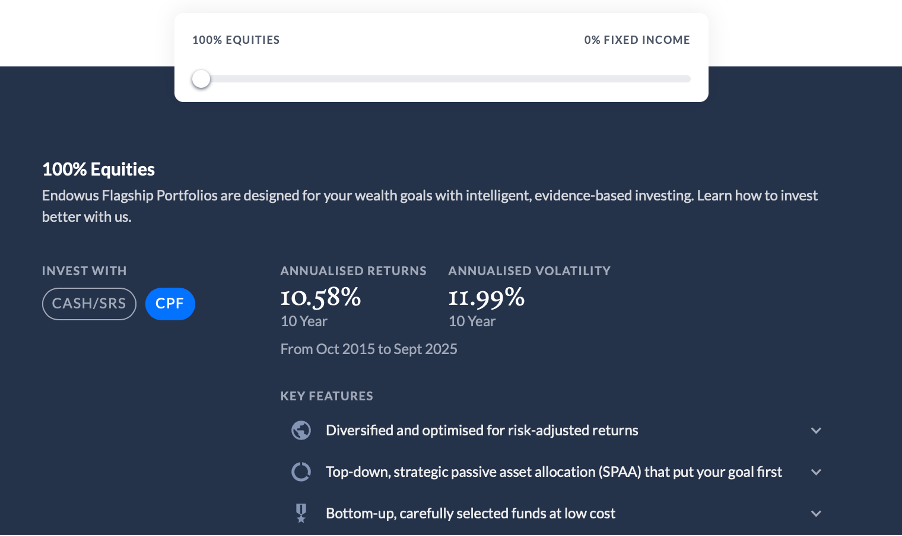

For example, you can invest your CPF in Endowus’ Flagship Funds. As you can see below, the portfolio comprising 100% equities has delivered over 10.5% p.a. over the past 10 years.

Source: Endowus

Invest Better With Endowus

If you’re interested to start investing with Endowus, you’ll be happy to know that DollarsAndSense readers can enjoy $20 off their access fee (equivalent to $10,000 advised free, assuming an access fee of 0.40%). Sign-up using this link to claim this special offer. Terms & Conditions apply.

#3 Do Not Pay Your Monthly Mortgage With CPF Alone – If You’re Not Investing Your Cash

Using your CPF to cover monthly home loan payments entirely might feel like you’re boosting your cashflow, but it’s not always the best decision in the long-term.

For a start, you won’t just be shrinking your CPF OA balances each month, but also increasing the amount you “owe” your own CPF. This is because you have to eventually refund the principal plus accrued interest back to your CPF when you sell your home.

By using cash to partially or even fully pay for your mortgage, you can preserve your OA balances, and set it aside for your retirement purposes – by topping up your SA or investing. This can help you reach the FRS much faster, providing greater peace of mind, knowing that your retirement is taken care of.

#4 Do Not Top-Up Your CPF SA – If Your Income Is Relatively Low

Lower-income earners often get limited benefit from tax relief because their annual tax is already low. Remember, the first $20,000 of your chargeable income is not taxed at all.

So, while you can reach your FRS more quickly by making CPF top-ups, other considerations should be your cashflow and tax benefit.

For example, an individual earning about $40,000 a year, or about 3,400 a month, may not get much benefit from topping up their CPF after taking into consideration the tax reliefs that nearly everyone in Singapore already get.

This includes the compulsory CPF contributions, Earned Income Relief, and NSman Relief. Based on your individual circumstances, many of you can also qualify for other types of tax relief, such as the Grandparent Caregiver Relief, Parent Relief, Qualifying Child Relief, Working Mother’s Child Relief and others.

- The compulsory CPF contributions (on a $40,000 annual salary) can reduce your chargeable income by $8,000 (i..e 20% of your income).

- The Earned Income Relief will reduce your chargeable income by at least $1,000 ($1,000 for 55 and below, $6,000 for 55 to 59, and $$8,000 for 60 and above)

- The NSman Relief can be worth at least another $1,500 in tax relief ($1,500 to $5,000 for self, $750 for NSman wife or parent)

- If you have one child and are caring for one parent, you will get another $4,000 of tax relief (per child) and $5,500 (per parent not staying with you, and $9,000 if they are staying with you).

If your current situation resembles this, your chargeable income would reduce to $20,000 – and you would be paying no income taxes.

Read Also: How Much Tax Savings Do You Get For Making SRS Contributions, Based On Your Salary

#5 Do Not Withdraw Any CPF at 55 – If You Don’t Have a Plan to Beat 4% p.a.

Your RA and SA funds earn a floor interest rate of 4% each year. At 55, you can withdraw up to $5,000 or anything above your Full Retirement Sum (FRS).

Making a withdrawal only to splash it on a holiday or car may give you a great experience and make you happy, but it’s short-lived and can set back your retirement timeline significantly.

If you’re determined and knowledgeable enough to grow the money at a higher rate, your money will not only last in the long-term, you’d be better off making the withdrawal.

Bear in mind that you’re not only trying to beat 4% p.a. Your first $60,000 in your CPF will earn an additional 1% p.a., and your first $30,000 will earn an extra additional 1% p.a. This means your RA balances may earn up to 6% p.a.

Another thing to bear in mind, though, is that the 4% p.a. is risk-free and hard to consistently replicate every year over the long-term.

And, even if you don’t withdraw the money from your CPF account, you can retain the flexibility to withdraw the money in future.

#6 Do Not Top-Up Your RA Above the FRS – If You’re Doing It Only for Tax Relief

Some of you may think that topping up to the Enhanced Retirement Sum (ERS) will continue to give you sizeable tax breaks.

While it will definitely leave you with a stronger retirement pot, any top-ups beyond your FRS may not give you any tax relief.

On the CPF website, it clearly states that “Tax relief is only granted up to the current year’s FRS”. This means that topping up beyond the FRS will not give you any tax breaks.

However, one thing that we could not uncover online is the meaning of the words “current year’s FRS”. Worded this way, it seems to suggest that we may get tax relif on top-ups up to the existing year’s FRS even if the person is above 55 and their cohort’s FRS is locked.

So, you may want to clarify with the CPF Board (and let us know!) if you intend to make CPF contributions to yourself or loved ones above 55 years old.

The bottomline is that while you’re beefing up retirement security, it may not give you any tax relief beyond the FRS.

#7 Do Not Top-Up RA or MA – Without Understanding the Govt’s Dollar-For-Dollar Matching Under MRSS & MMS Schemes

CPF top-ups into Retirement Account (RA) or MediSave (MA) can attract a dollar-for-dollar matching by the government. But, the mechanics matter.

Top-ups under the MRSS (Matched Retirement Savings Scheme) come with conditions. Firstly, the giver will not receive any tax relief if the recipient enjoys the dollar-for-dollar matching. Secondly, there are caps, including a $2,000 yearly cap and $20,000 lifetime cap for top-ups that enjoy dollar-for-dollar matching.

Besides conditions on MRSS, recipients also have to be eligible. They must have

- Retirement Account savings of less than $106,500 (i.e. the Basic Retirement Sum for the year)

- Average monthly income of not more than $4,000 a month

- Live in a home with Annual Value of $21,000 or less

- No more than one property ownership

Top-ups under the new MediSave Matching Scheme (MMS) starts from January 2026, also come with conditions.

- The scheme will last 5 years only – from 2026 to 2030.

- Recipients must also be:

- Aged 55 to 70 in the year

- Have less than 50% of the current Basic Healthcare Sum (BHS)

- Earn no more than $4,000 a month

- Live in a home with Annual Value of $21,000 or less

- Not owning more than one property.

- In addition, self-employed persons must have fully settled or be on a monthly instalment plan for their MediSave payments.

Without understanding these, you may miss out on the dollar-for-dollar government matching, essentially meaning that you top without getting the full benefits you had expected.

#8 Do Not Invest Your CPF Funds – If You’re Unsure How to Beat the Special Account’s 4% p.a.

While the CPF Investment Scheme lets you invest OA/SA funds above certain thresholds, it isn’t always better than earning the risk-free 4% p.a. in your Special Account.

Investment losses can reduce your CPF retirement funds, and significantly hamper your retirement plans.

Don’t invest CPF money unless you truly understand the risks. The Special Account’s 4% p.a. is hard to beat safely and consistently. Investing your CPF also opens you to other risks, such as over-trading instead of letting it slowly accumulate in the background.

If you’re keen to invest but also understand you may not make the best investment decisions, another solution is to take the decisions out of your hands. You can invest your CPF with Endowus.

Reiterating the point above, Endowus allows you to invest your CPF in its Flagship Funds that are globally diversified. For portfolios that have 100% exposure to equities, the returns are over 10.5% over the past year.

Furthermore, you can always sell your investments and see your funds flow back into your OA, rather than lock it into your SA by transferring it.

Invest Better With Endowus

If you’re interested to start investing with Endowus, you’ll be happy to know that DollarsAndSense readers can enjoy $20 off their access fee (equivalent to $10,000 advised free, assuming an access fee of 0.40%). Sign-up using this link to claim this special offer. Terms & Conditions apply.

Nevertheless, if you’re keen for your Ordinary Account balances to earn more than the 2.5% floor rate, but don’t want to take risks, then transferring your funds into your SA to earn a floor rate of 4.0% could be more attractive instead.

Don’t Do Anything With Your CPF Without A Plan

CPF is a tool that you can use with some flexibility. Some moves can sound good on paper (i.e. higher interest! tax relief! less cash outlay!), but may cost you long-term stability or short-term peace of mind.

Before you act, understand your purpose for making your CPF moves and know your short and long-term goals.

This article contains affiliate links. DollarsAndSense may receive a share of the revenue from your sign-ups. You can refer to our editorial policy here.