Rollover credit card balances in Singapore have reached $9.07 billion in the third quarter of 2025, setting a new record, according to figures from the Monetary Authority of Singapore (MAS). Rollover balance refers to credit card balances that are not paid in full before the due date. These outstanding balances will incur interest charges.

Rollover balances have been sharply increasing since 2021. This means that Singaporeans are spending more on their credit cards and getting further into debt as bill payments are deferred. Fortunately, credit card delinquency rates are currently still stable, remaining at below 1%, which means that most Singaporeans are still able to manage their debt. But instead of waiting till it’s too late to do something about it, here are six steps to take to better manage your credit card debt.

Read Also: Best Cashback Credit Cards In Singapore: Which One Suits Your Lifestyle?

#1 Make A List Of All Your Outstanding Debts

When tackling any problem, getting more visibility of what you’re dealing with is always the first step.

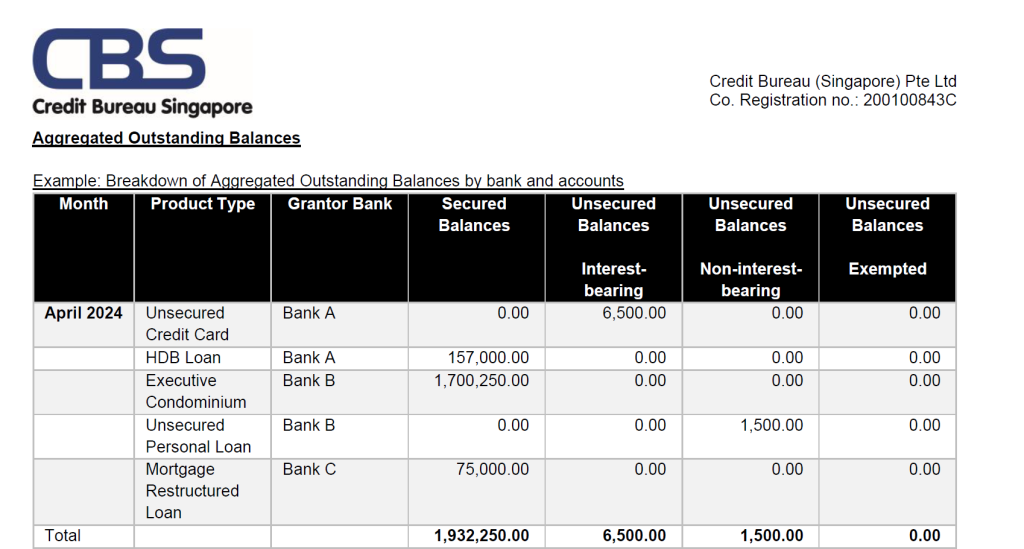

You can obtain your credit report online from Credit Bureau Singapore for just $8 (excluding GST). However, if you have applied for a new credit facility in Singapore in the past 30 days, you will be eligible for a complimentary credit report, regardless of whether your application was successful or not.

Within your credit report, under the section “Aggregated Outstanding Balances”, you’ll be able to see a breakdown of how much is outstanding to each credit facility, and more importantly, which amounts are earning interest.

Source: Screenshot of Credit Bureau Singapore’s Credit Report

#2 Find Out How Much Interest Each Credit Card Is Charging You

Credit cards in Singapore charge similar interest rate on outstanding balances, but if you’re managing credit card debt, it actually helps to know which credit cards have higher interest rates than others. Here’s a non-exhaustive list of card providers and their current effective purchase interest rates.

| Bank | Effective Interest Rate (per annum) |

| Standard Chartered, Citibank | 27.9% |

| DBS, UOB, HSBC, CIMB, American Express | 27.8% |

| OCBC | 27.78% |

One strategy to tackle credit card debt is to prioritise paying off the cards with higher interest rates. This is to avoid paying more interest overall.

Read Also: Ultra-High Net Worth Credit Cards In Singapore And How Are They Different From Regular Cards

#3 Ensure You Make At Least The Minimum Payment By The Payment Due Date

This is basic credit card discipline, but it still bears repeating. It is ideal to always pay your credit card bills in full and on time, but for those of us with outstanding credit card debt, we should at least avoid defaulting on them.

You are in default if you have not made the minimum payment on the payment due date indicated on your latest statement.

There are two main reasons why defaulting on credit card payments is bad. Firstly, card providers charge hefty late payment fees, typically about $100 per card, when the minimum payment is not made on time. Secondly, card providers can also raise your interest rates, typically by an additional 3%, if you have defaulted at least once.

Incurring additional charges and higher interest rates will make your efforts to deal with credit card debt that much harder.

#4 Try To Get Your Credit Card Annual Fees Waived, But Do Not Cancel Any Cards With Outstanding Balances

In the same vein as avoiding incurring late fees on your credit cards, you should also try to get any annual fees charged to your credit cards waived. Each card provider handles such requests differently, but these days, most annual fee waiver requests are done through the various chatbot channels offered by banks.

If your annual fee waiver request is not successful, you have the option to cancel the card. Since annual fees are charged for the upcoming year, then by cancelling the card, the annual fee will be automatically waived. However, there are two things to note before you decide to cancel a card.

Firstly, cancelling a credit card that you’ve held the longest will have a small effect on your credit score, especially if you have been diligently paying your dues promptly and in full. This is because you will lose the benefit of having a long credit history.

Secondly, cancelling a credit card with outstanding balances will have a major impact on your credit score. Both voluntary and involuntary account closures with outstanding balances are recorded in your credit report.

#5 Get A Personal Loan To Pay Off Credit Card Debt

It may seem counterintuitive to borrow more money to pay off outstanding credit card debt, but many personal loans in Singapore have significantly lower interest rates than credit cards. Several banks are currently advertising personal loans with effective interest rates as low as 3% to 5% per annum. Depending on the amount you borrow, however, you’re more likely to be offered between 10% to 15% per annum.

This is still lower than what you would be paying on your outstanding credit card balances, of course. Using the funds from a personal loan to pay off your credit card debt will reduce the overall interest payments you’ll need to make.

You’ll be able to structure your monthly personal loan repayment between one to five years. Typically, longer repayments have lower monthly repayment amounts and incur lower interest rates, but you will end up paying more interest overall.

Also note that applying for a personal loan will entitle you to a free report from Credit Bureau Singapore, as mentioned in step 1.

#6 As A Last Resort, Consider A Debt Consolidation Plan

Debt Consolidation Plan (DCP) is a debt refinancing program that allows you to consolidate all your unsecured credit facilities under one financial institution. In other words, all your outstanding credit cards and personal loans will be consolidated into one account.

To be eligible for DCP, the total interest-bearing unsecured debt on all your credit cards and unsecured credit facilities must exceed 12 times your monthly income.

Different financial institutions will have different terms and conditions for their DCP product, but ultimately, all your existing unsecured credit facilities will cease. You will not be able to apply for any new credit facilities, though you will be provided with a revolving credit facility with a credit limit fixed according to your monthly income.

This is obviously only to be used as a last resort, as the DCP will remain in your credit record for 3 years after you’ve made the last repayment, affecting any future credit facility applications.

Read Also: What Is The Debt Management Programme (DMP), And How It Can Help You Get Out of Credit Card Debt?

Advertiser Message

Thinking Of Switching Brokers Or Consolidating Your Holdings?

Tiger Brokers is currently running a transfer-in campaign where eligible clients can receive an iPhone 17 Pro Max* when they transfer in their assets.

For SGX investors, there is also a CDP Transfer promotion with 0* commissions on Singapore stocks.

Find out more here. *T&Cs apply.

Bonds and Fixed Income

StashAway Income Portfolio: How You Can Earn 4.6%* Dividends From Your Investments Each Year