As Singapore celebrates 60 years of independence, younger Singaporeans are already imagining what life decades ahead might look like. According to the SG60 Financial Future Poll conducted by Prudential Singapore, about half of Gen Z (51%) believe they will retire comfortably, confident that they will have enough for daily expenses, healthcare, and lifestyle needs.

Optimism Without A Roadmap?

This optimism is also striking.

While Gen Zs are more confident about retirement than Millennials (45%) and Gen Xs (38%), but there is a catch — 72% of Gen Zs have no concrete retirement plan.

Many are still in school or just starting in the workforce, where their immediate focus is on building careers and income. For now, retirement feels like something they can only think about once they have “real money” to set aside.

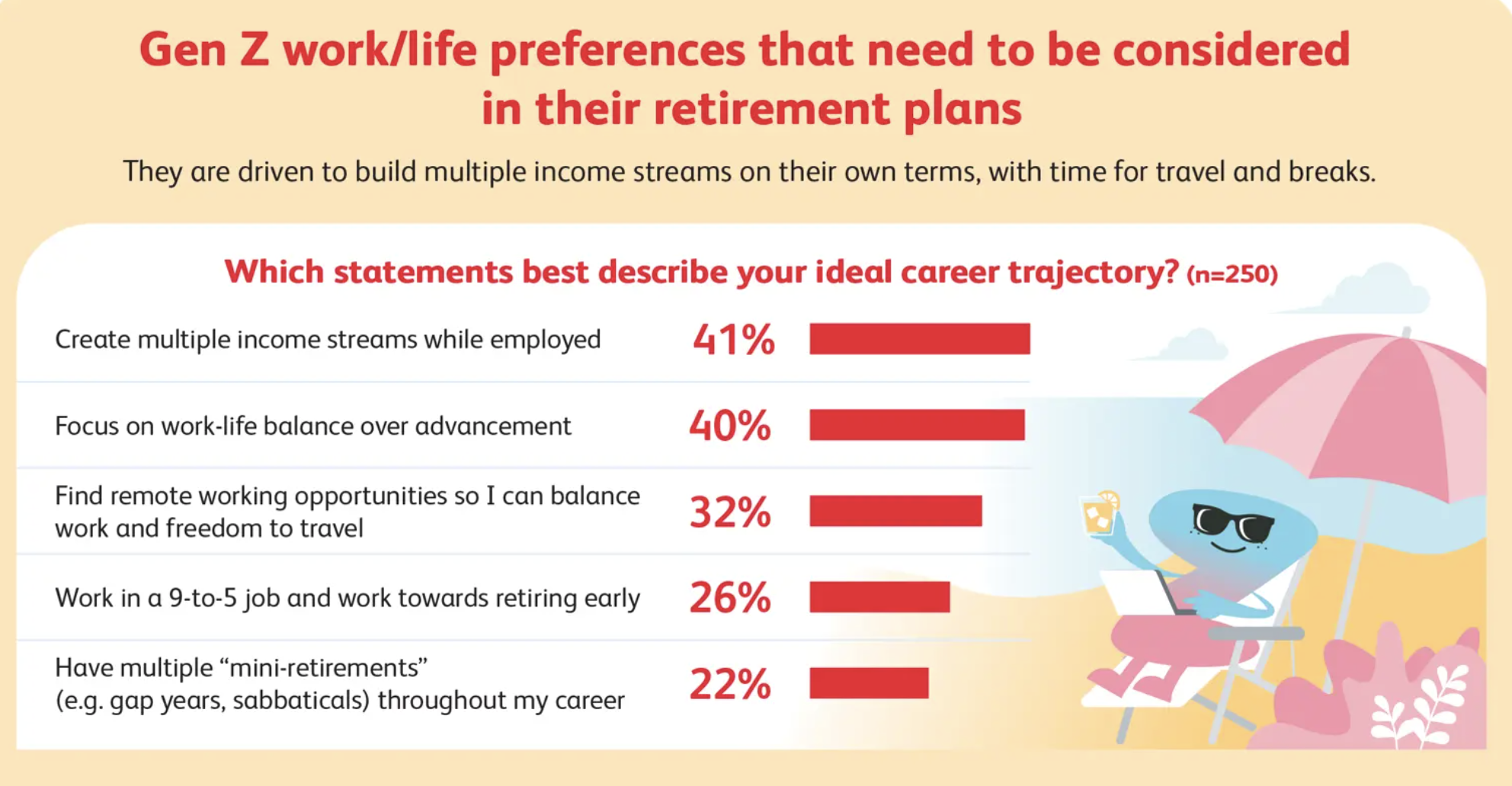

How Gen Z Views Work & Retirement

What sets Gen Z apart is not just their optimism, but their different approach to work and life. Many want multiple income streams, do not want a 9-to-5 job and also hope to find remote work opportunities so they can balance work and travel. Some even hope for “micro-retirements” — taking extended breaks throughout their lives rather than waiting until their 60s.

A sizeable group also aspires to retire earlier than past generations, with some aiming to stop work by 60, and a few even by 50. It is a refreshing mix of ambition and flexibility. But without a clear financial plan, these aspirations risk remaining just that — aspirations.

Read Also: 5 Insurance Tips From InsureXpo by CIMB For Young Graduates Entering The Workforce

The Hard-Earned Lessons From Baby Boomers

The poll also asked Baby Boomers to reflect on their financial journeys, and their advice was unambiguous: start earlier than you think you need to.

Almost all Baby Boomers said they would have done things differently if given the chance. On average, they wished they had started retirement planning 12 years earlier, at 28 instead of 40. Many now realise that the years lost to inaction cannot be bought back, and that the compounding effect of time in investing is one of the most valuable assets they missed out on.

Their top regrets included not developing stronger financial habits, missing out on an earlier retirement, and living with unnecessary financial stress. Some wished they had invested their spare cash sooner instead of leaving it idle, while others admitted that overspending set them back.

As one 62-year-old retiree put it: “I thought retirement would be 10–20 years, but it may be 30 years or more. I should have invested my spare cash much earlier.”

A Reality Check Across Generations

Regardless of age, Singaporeans today share many of the same concerns: rising cost of living, growing healthcare expenses, and income growth that may not keep pace. These challenges are unlikely to ease; if anything, they may intensify as life expectancies increase and retirement stretches longer than many anticipate.

When asked how they would fund retirement, most respondents pointed to CPF and bank savings as their anchors. But many also considered investments such as stocks, ETFs, bonds and insurance-linked plans to supplement their retirement income.

Interestingly, Gen Zs and Millennials leaned more towards index funds and ETFs, while older generations placed heavier reliance on insurance. This generational gap could leave younger Singaporeans under-protected if unexpected healthcare costs arise.

Why It Pays To Start Early

The key takeaway is simple: optimism alone is not enough. Starting early matters far more than most realise. Even modest sums saved and invested in one’s 20s can compound significantly by the time retirement arrives in the 50s or 60s.

Baby Boomers today wish they had started earlier. Gen Zs, with time on their side, have the opportunity to avoid repeating the same mistake. Building a plan now, however small, is the best way to turn retirement confidence into reality.

In other words, optimism is a good beginning. But optimism paired with action is what truly sets the foundation for long-term success.

Source: Prudential