For many Singaporean men, National Service (NS) may be their first introduction to insurance coverage. During full-time National Service (NSF), servicemen receive complimentary insurance coverage under the MINDEF & MHA Group Insurance Scheme, which is currently administered by Singapore Life Ltd (Singlife).

Under the MINDEF Group Insurance Core Scheme, NSFs receive $350,000 in Group Term Life (GTL) coverage and $350,000 in Group Personal Injury (GPI) coverage. This provides financial protection in the event of death, Total Permanent Disability (TPD) and Permanent Dismemberment (PD). The coverage is also provided without underwriting, meaning pre-existing medical conditions are covered, with premiums paid in full by MINDEF or MHA.

After You ORD, You Can Continue Your Coverage Under The MINDEF Voluntary Scheme

While the complimentary coverage under the MINDEF Group Insurance Core Scheme ends when you complete your full-time National Service, your access to the MINDEF & MHA Group Insurance Scheme does not.

After you ORD, you can continue your coverage via the MINDEF Voluntary Scheme, allowing you to continue your insurance coverage at group rates, while also increasing your level of protection if you want. The Voluntary Scheme is not limited to just NSmen, but also regulars, volunteers, public officers working with MINDEF or MHA, and employees of selected affiliated entities.

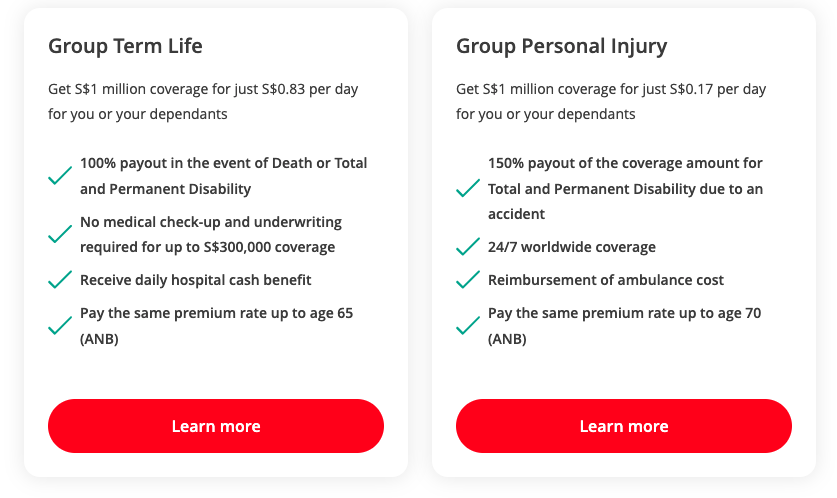

One of the biggest advantages of the Voluntary Scheme is the significantly higher coverage limits. According to Singlife, you can purchase up to $1 million in Group Term Life (GTL) coverage for yourself. At current premium rates, $1 million of coverage costs from just $0.83 a day, making it one of the more affordable ways for young adults to secure a substantial amount of life insurance.

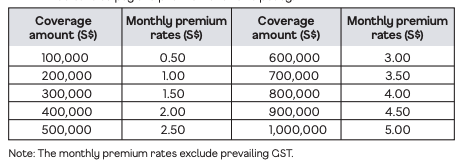

Similarly, you can purchase up to $1 million in Group Personal Injury (GPI) coverage from just $0.17 a day. This provides additional financial protection in the event of accidental death or permanent disability, whether the accident occurs during NS activities or in your daily life.

For example, if you wish to enjoy group term life insurance coverage of $500,000, your monthly premium will be $12.50. For maximum coverage of $1 million, the monthly premium is $25.

Source: Singlife

For Group Personal Injury, premiums are just $5/month for $1 million in coverage.

Source: Singlife

Beyond life and personal accident insurance, the MINDEF Voluntary Scheme also allows you to enhance your protection with optional riders and additional plans. For example, the Living Care rider provides coverage of up to $500,000 against 37 critical illnesses, while Living Care Plus extends protection to include 10 early-stage critical illnesses, with coverage of up to $500,000. Depending on your needs, you can also add Disability Income and Outpatient Medicare plans to build a more comprehensive insurance portfolio.

NSFs also have the option to purchase additional coverage before they ORD, although the premiums for the extra coverage are payable by the individual.

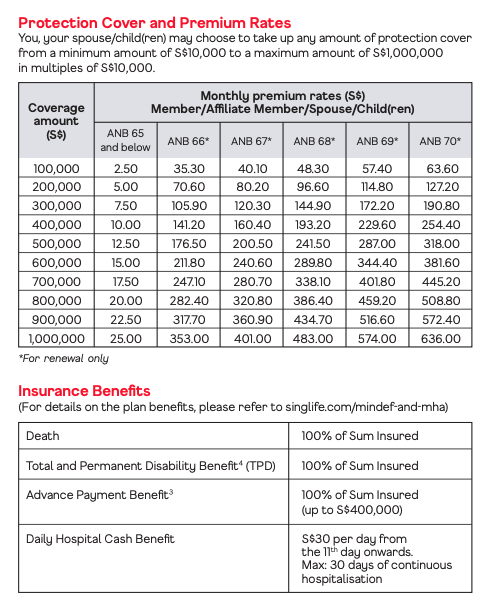

One thing worth noting is that the MINDEF Group Insurance is not limited to NSmen. Spouse and children can enjoy the same group rates, allowing families to obtain insurance coverage under a single scheme at relatively affordable premiums.

Group Insurance Coverage May Last Till 70, But Premiums Become Much Higher After 65

While the Group Term Life coverage can continue until age 70, policyholders should note that premiums may rise significantly from age 66 onward. For example, for $1 million in coverage, monthly premiums rise from $25/month (ages 65 and below) to $353/month at age 66.

In practical terms, this means the plan may be most useful as affordable term life coverage up to around age 65.

Why The MINDEF & MHA Group Insurance Scheme Is Worth Keeping After You ORD

The MINDEF & MHA Group Insurance Scheme remains one of the more affordable ways for eligible NSmen and employees of MINDEF and MHA to purchase term life and personal accident insurance coverage. Based on the premiums you pay, it offers good value for those looking to build basic financial protection for themselves and their families.

That said, it should not necessarily be viewed as a complete insurance solution. Depending on your stage of life and financial commitments, you may still need additional coverage, whether it is for critical illness, hospitalisation, disability income or a higher level of life insurance.

Read Also: Guide To Understanding The Singlife MINDEF And MHA Group Insurance