This article was written in collaboration with DBS. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research, are purely for informational purposes, and should not be relied upon as financial advice. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions, and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

Passion is what got us started. Perseverance is what got us here.

DollarsAndsense started from a genuine interest in finance. We enjoyed writing about finance, discussing ideas and making complex topics easier to understand. Those are still some of the best parts of the job.

But running a business involves much more than the visible work. It also means dealing with the operational and financial realities that keep the business moving.

Behind Every “Stable” Business Are Invisible Moving Parts

Running a business involves a lot more than the work people see. Beyond the content and client work, there is payroll to meet, invoices to send, receivables to track, expenses to manage and payments to follow up on. Even with 30-day payment terms in place, cash flow does not always move as neatly as you want it to. And when you have headcount and recurring monthly costs to look after, timing matters.

That is something many SMEs will recognise. Cash flow is not just about whether revenue is coming in, but whether it is coming in at the right time to support the day-to-day needs of the business. Office costs, production expenses, subscriptions, travel and team spending continue regardless.

Over time, I have come to see that managing cash flow well is partly about discipline, but also about having the right tools in place for different needs. Some needs are immediate and operational, while others require a longer runway. For example, building a new product such as our DAS chatbot, or setting up a new business line like an events arm, often requires investment before the revenue fully catches up. This is where access to the right financing tools can matter. DBS Business Loans can help businesses access funding for growth without putting unnecessary pressure on day-to-day cash flow. For recurring operational expenses, DBS Commercial Credit Cards can offer short-term flexibility through up to 55 days of interest-free credit, while making it easier to consolidate spending, manage subscriptions and keep track of team and business expenses more clearly. With card controls through DBS IDEAL, businesses can also improve visibility over spending and reduce some of the admin that comes with monthly claims and expense tracking.

In that sense, the visible part of a business may be what people remember. But the less visible part: managing liquidity, staying on top of expenses and planning ahead, is often what keeps the business stable.

Systems Matter, But People Make Them Work

As DollarsAndSense grew, one thing became clearer. Stability does not come from systems alone. It also comes from building teams that can operate well across markets.

That is why I make it a point to spend time regularly with our remote teams. Managing across different markets requires more than assigning work from Singapore. It takes regular engagement to understand how each market operates, where the opportunities are and what support the team needs on the ground. Being there in person helps us stay closer to those realities and be more agile when it comes to growing the team.

Having a commercial credit card such as the DBS Platinum Business Card also helps ease some of the operational friction that comes with managing a business across markets. According to DBS, the DBS Visa Business Platinum Card is designed to support SMEs with operational flexibility and business travel coverage. For businesses with regular travel needs like ours, there are complimentary features such as travel accident insurance of up to S$1 million per cardholder when the full airfare is charged to the card, as well as annual coverage for employee misuse for companies with two or more cards issued. This can be useful for businesses that issue cards across a growing team.

Reducing Friction As The Business Scales

There was a time when we tracked payroll, expenses and revenue on a simple Excel sheet. At a smaller scale, that was manageable. But one missing entry could mean spending hours tracing the numbers just to make sure everything balanced.

As the business grows, that way of working becomes harder to sustain. Manual processes create more room for error, take up time that should be spent elsewhere and make it harder to maintain a clear view of cash flow and business performance. And when an investor, partner or stakeholder has a question, you need to be able to pull up the numbers and give a clear overview of the business without delay.

At a certain point, putting better systems in place is not just about efficiency. It becomes necessary for visibility, control and planning. The same applies to cash flow. As complexity grows, businesses need the right systems and financing tools in place to manage both everyday operations and longer-term growth with more confidence.

Looking At Cash Flow As A Whole

Over time, I have also come to see that cash flow needs are rarely one-dimensional. Some are immediate and operational. Others are tied to growth and require a longer runway.

That is where different financing tools play different roles. Commercial Credit Cards can offer flexibility for recurring business expenses and short-term liquidity needs. Business Loans, by contrast, are often more suitable for larger requirements such as working capital, new capabilities or longer-term growth plans.

Used well, the two are not substitutes for each other. They work best when paired as they support different parts of the business at the same time: one helping to manage ongoing operating needs, the other giving the business room to invest and grow with more confidence.

Source: DBS

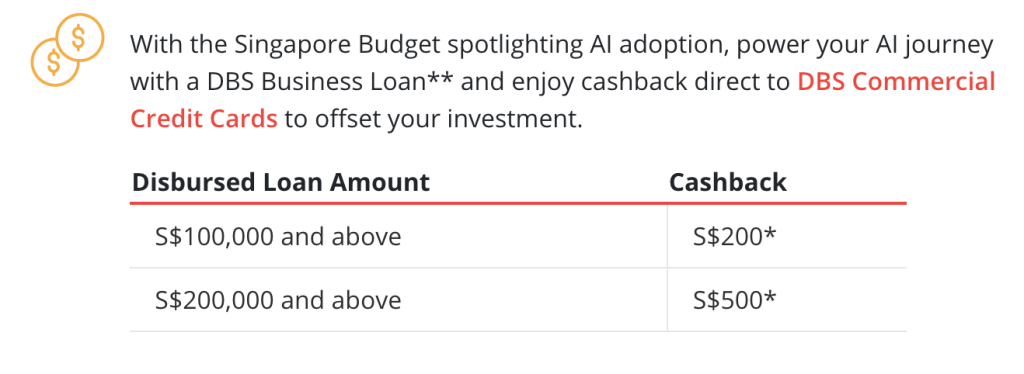

For businesses considering both, DBS is currently offering up to S$500 cashback on eligible business loans and working capital loans applied for by 31 July 2026.

On the cards side, the DBS World Business Card and DBS Platinum Business Card come with an 8% welcome bonus cashback with a minimum spend of $1,000 per month that is valid for the first 3 months from card issuance with a total cashback capped at S$240, up to 55 days credit terms and card controls on DBS IDEAL.

For businesses with overseas spending, the DBS World Business Card also offers an additional 2% rebate on foreign currency transactions. This means that businesses with overseas subscriptions, travel expenses, vendor payments or cross-border operational costs can offset part of their foreign currency spend more effectively.

What Keeps A Business Truly “Stable”

A stable business is not defined only by healthy cash flow or repeat clients. It takes real investment to build the right team, create alignment and put the right systems and support in place. In business, every wrong decision carries a cost, whether in time, money or momentum.

As the business grows, the challenges do not disappear. They simply evolve. At one stage, you may be trying to solve a hiring gap. At another, you may be finding the funds to bring an almost-finished product across the line. What matters is whether you have built the foundations early, so that when opportunities come, you are ready to act on them. You do not want to be looking for money, people or structure only after the moment has arrived.

That, to me, is what stability really means. Not standing still, but being ready to move with confidence. Not having fewer moving parts, but having the right ones in place when it matters.