For savers in Singapore, earning a decent return on idle cash is getting harder again.

Banks have been lowering the interest rates on their savings accounts, which matters for anyone who keeps a meaningful amount of cash in the bank while waiting to invest, build an emergency fund or set aside money for near-term expenses. Most recently, OCBC announced that it will reduce the interest rates on its OCBC 360 Account from 1 May 2026.

This creates a familiar problem for depositors. If bank savings accounts are no longer offering an attractive yield, where should short-term cash go instead?

One option that has been getting more attention is money market funds. These products were less visible to everyday retail investors in the past but have grown in popularity in recent years, thanks to wealth platforms such as Endowus and Syfe offering them. Another FinTech firm, Chocolate Finance, has also introduced a similar proposition for consumers looking for a place to park their cash, combining conservative short-duration fixed-income funds and money market funds.

Such money market funds are often positioned as a way to earn a potentially higher return on short-term cash than a standard savings account, without taking on the kind of volatility associated with stocks or long-term bond funds. That said, they are not the same as keeping money in a bank account.

A Savings Account Is Not An Investment

The first, and more important, difference is that a savings account is not an investment while a money market fund is. This matters because for some people, a savings account and a money market fund may appear to serve a similar purpose (earn higher interest on their excess savings), yet they are structured very differently.

When you place money in a savings account with DBS, OCBC or UOB, you are making a bank deposit, not buying into an investment product. The savings in your eligible Singapore-dollar deposits are protected by the Singapore Deposit Insurance Corporation, up to S$100,000 per depositor per scheme member.

In other words, the bank is taking the risk on its balance sheet, not you. On the rare occasion that the bank runs into trouble, SDIC ensures that insured deposits are protected by law. While the interest rate on the account may change over time, whatever rate the bank has promised is still something the bank is obliged to pay.

A money market fund, or MMF, works differently. When you put money into an MMF, you are buying units in a collective investment scheme. The fund then pools money from many investors and invests it in short-term debt instruments such as Singapore Treasury Bills, certificates of deposit and high-quality commercial paper. These instruments generate income, which is then reflected in the fund’s returns (after fees) to investors.

This is why an MMF should be considered a very low-risk investment rather than a deposit account in a different wrapper. It is designed to be conservative, and many MMFs do indeed hold short-duration, high-quality assets to keep volatility low. But it is still an investment product and not covered by SDIC. Thus, it is not capital guaranteed in the same way as a Singapore bank deposit is.

Why Money Market Funds Are Worth Considering Right Now

Even without SDIC protection, there are still valid reasons why money market funds have become more popular, especially now that savings account interest rates are falling again.

Part of the appeal comes down to how savings accounts actually work in practice. On paper, accounts such as the OCBC 360 Account and DBS Multiplier can still advertise relatively attractive rates. But the headline figure often does not reflect what most people will realistically earn. To get the highest effective interest rate, you usually need to credit your salary, spend on an eligible credit card, increase your account balance, and sometimes buy insurance or investment products from the same bank.

This is where MMFs start to look more attractive. The proposition is much simpler. You put money into the fund, the fund invests in short-term instruments, and you receive whatever yield the portfolio generates after fees. There is no need to credit your salary, meet a minimum card spend, or buy additional financial products just to unlock a better rate.

For example, Endowus currently projects a yield of between 1.3% and 2.6% p.a. on its Cash Smart portfolios, while Syfe offers 1.6% on its Cash+ Flexi (SGD) portfolio.

Endowus Cash Smart. As you can see, even solutions from the same provider can yield different results. If you’re interested in starting to invest with Endowus, you’ll be happy to know that DollarsAndSense readers can enjoy $50 off their access fee. Sign up using this link to claim this special offer. Terms & Conditions apply.

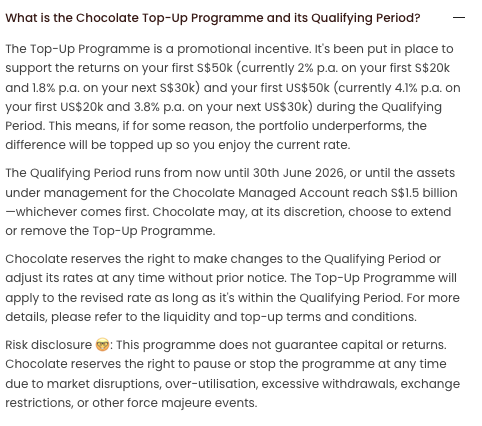

Chocolate Finance has an interesting proposition: it’s running a Top-Up Programme that “supports the returns on your first S$50k (currently 2% p.a. on your first S$20k and 1.8% p.a. on your next S$30k)” during a qualifying period (which runs till 30th June 2026).

Chocolate Finance, details of its Top-Up Programme

If you prefer a managed approach to investing, Syfe offers portfolios for different objectives — from globally diversified Core portfolios and Equity100 for long-term growth, to REIT+ and Income+ for investors seeking income. You can also use its Cash+ solutions to put short-term funds to work while maintaining liquidity.

Find out more about the different Syfe portfolios and which may suit your financial goals.

Regardless of which platform you choose to invest through, the point remains: earning higher interest rates via MMFs is going to be subject to market returns, notwithstanding a time-limited promotional offer where platforms say they will give you a top-up if returns fall short. Even then, there is no guarantee.

Should You Switch To MMFs?

The answer depends on the role your savings account already plays in your finances.

If you are currently meeting the full bonus criteria on your savings account, the effective interest rate you earn may still be competitive, even after the recent cuts. For some depositors, especially those who already credit their salaries, regularly spend on the right credit card, and maintain the required balances, the extra effort may be minimal. In that case, there may not be a strong reason to move your cash out just because rates have come down.

The situation looks different for people who are consistently missing some of those conditions. If you are keeping cash in a savings account but only earning the base rate, or a rate far below the headline figure, then an MMF or cash management account may be a more suitable place for that money.

As interest rates continue to adjust, the relative appeal of savings accounts and MMFs will continue to shift. But the core question remains the same. Investors should understand what each product actually is, what protections apply, and whether the return they are getting is worth the conditions attached.

Read Also: Complete Guide To Cash Management Accounts In Singapore

This article contains affiliate links. DollarsAndSense may receive a share of the revenue from your sign-ups. You can refer to our editorial policy here.