This article was contributed to us by Sebastian Sieber, Founder of Cashew.sg

Ask anyone in Singapore whether to rent or buy and you’ll get the answer before you finish the question. With home ownership above 90 percent (SingStat, 2024), this isn’t really an opinion here.

I share the instinct. You have to live somewhere, and every month you rent is a month you pay for a roof without owning an inch of it. Buying turns part of that cost into equity. Leverage makes it more powerful: if you buy with 25 percent down, even a 2 percent year-on-year rise in the property’s value is a much larger return on the cash you actually put in, because you captured the gain on the whole asset while funding only a quarter of it. That’s the real engine behind property wealth here.

The instinct to own is sound. Where it goes astray is the assumption riding along with it: that because owning beats renting in general, any property you buy must be a good buy. After sitting across the table from buyers running their numbers, I’ve come to think the sharper question isn’t whether to buy, but which property, and at what price. A home earns its keep simply by housing you. But some properties compound into real wealth while others merely keep pace with what your money could have done elsewhere.

Most rent-versus-buy debates line up the monthly mortgage against the monthly rent, see they’re similar, and conclude buying wins. There’s an insight buried there. Rent leaves your pocket and never comes back. A mortgage splits in two: interest, a genuine cost gone the same way rent is, and principal, which builds equity you own. So the true monthly cost of owning is closer to the interest alone.

But the monthly view misses the larger contest. Buying also costs a large slug of capital upfront, such as the downpayment and Buyer’s Stamp Duty. That capital has an alternative life. It could be in a diversified portfolio compounding for you instead. So the honest comparison isn’t mortgage versus rent. It’s the total wealth you end up with after buying, versus the total wealth you end up with if you rent and invest every dollar you didn’t sink into the property.

Framed that way, the outcome turns on three numbers, and small changes in any of them can flip the answer.

Lever One: How Much Will The Property Actually Appreciate?

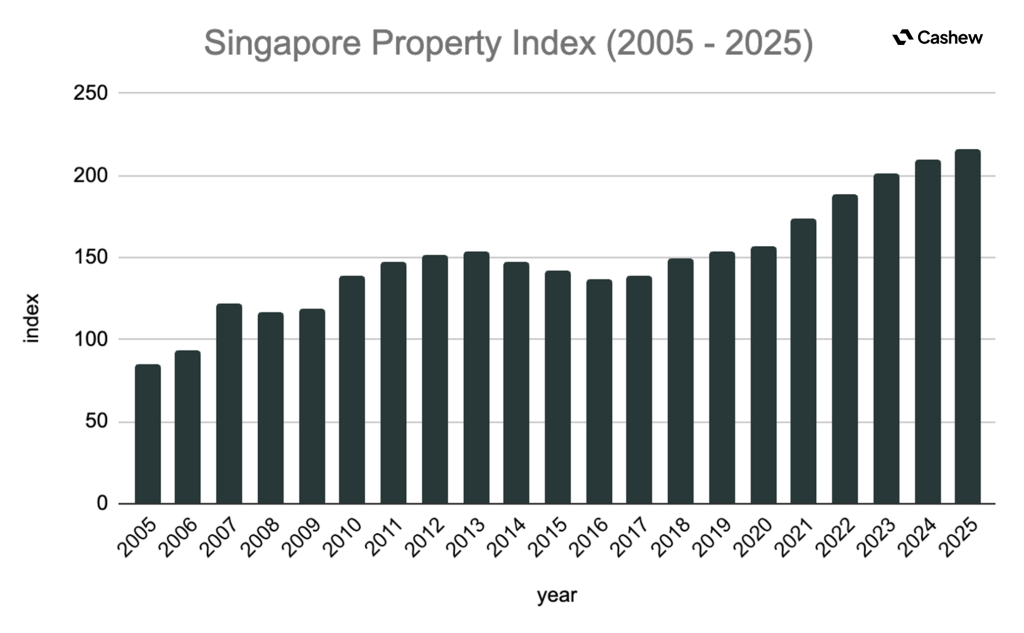

Singapore property has gone up. Over the past twenty years, private residential prices have risen by roughly 155 percent, about 4 to 5 percent a year.

Source: URA Private Residential Property Price Index)

But that 4 to 5 percent is an index across the whole market. Individual projects, locations and entry prices scatter widely around it. Two buyers can purchase in the same year and walk away with completely different outcomes. The market average is not a promise attached to your front door.

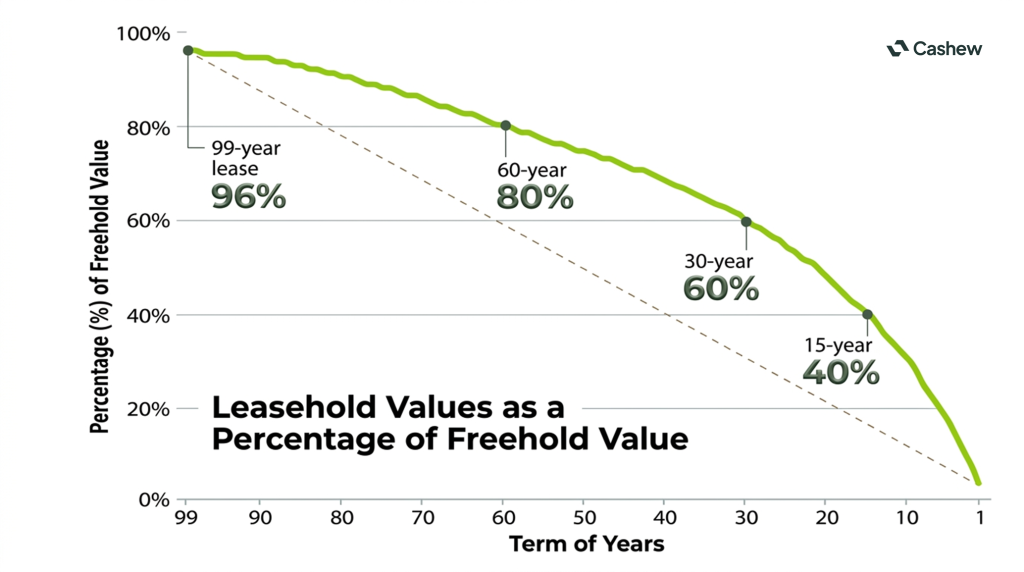

Tenure is a big reason why. Every HDB flat sits on a 99-year lease, and so do a large and growing share of private condos, especially newer launches sold under government land sales (HDB; URA). A lease is a depreciating asset. Appreciation and decay happen at the same time, so the price growth you see is the net result. The decay isn’t gradual either. Under the SLA’s Bala’s Table, a fresh 99-year lease is worth about 96 percent of freehold; at 60 years remaining the land is worth about 80 percent, at the halfway mark around 75 percent, and by 30 years left closer to 60 percent, falling sharply from there. Think of it as compound interest in reverse.

Source: SLA, Bala’s Table

A new, sought-after property can still rise in its early decades, because demand and inflation outpace the lease. The drag usually bites around the 30 to 40 year mark. There’s a second sting that arrives earlier and lands in my world: financing. As the lease shortens, banks lend less and CPF usage gets restricted, shrinking the pool of buyers who can afford your unit when you sell. Private owners can apply to top up the lease by paying SLA a premium, but approval is discretionary, and most HDB flats have no such path. This is why tenure belongs near the front of the decision.

Lever Two: How Fast Will Rent Rise Underneath You?

The renter’s case isn’t “I save the difference forever at today’s rent.” Rent moves, and here it can move violently. Private rents surged more than 20 percent in 2022, climbed another 8.7 percent in 2023, slipped 1.9 percent in 2024, then rose about 1.9 percent in 2025 (URA rental index). Early 2026 has been calmer, with the rental index up just 0.3 percent in the first quarter (URA, Q1 2026).

That volatility is the renter’s central risk. A buyer locks in the cost of the asset and watches inflation erode a fixed-ish loan. A renter is exposed at every renewal. Assume rent rises 1 percent a year and renting looks comfortable. Assume 4 percent, compounding over a long horizon, and the renter’s advantage quietly evaporates.

Lever Three: What Could The Downpayment Earn Elsewhere?

This is the lever the property reflex ignores. The money you commit, the downpayment and stamp duty, isn’t free. It has an opportunity cost equal to whatever it could earn elsewhere. A cautious planning assumption sits in the mid to high single digits.

The point isn’t to pick a precise number. It’s that the comparison is brutally sensitive to it. If your property appreciates at 2 percent while an average alternative portfolio compounds at 7 percent, the renter who disciplines themselves to invest the freed-up capital is running a serious race, even before the buyer’s leverage pulls the other way.

Why The Answer Is A System

Buying is the right default for most people who plan to stay put. But the three levers explain why some purchases are far smarter than others. A property is a strong buy when appreciation is healthy, when you’ll hold it long enough to outrun the 3 to 5 percent in transaction friction that buying and selling incur, and when the rent you’d otherwise pay was set to climb steeply. It’s a weaker buy, sometimes weaker than renting and investing the difference, when your horizon is short, when the gap between your investment return and the property’s appreciation is wide, and when the entry price leaves little room to grow.

Change one assumption and the verdict can reverse. That’s why it’s important to run your own numbers rather than borrow a slogan.

That’s why we built a free rent-versus-buy tool which you can try here.

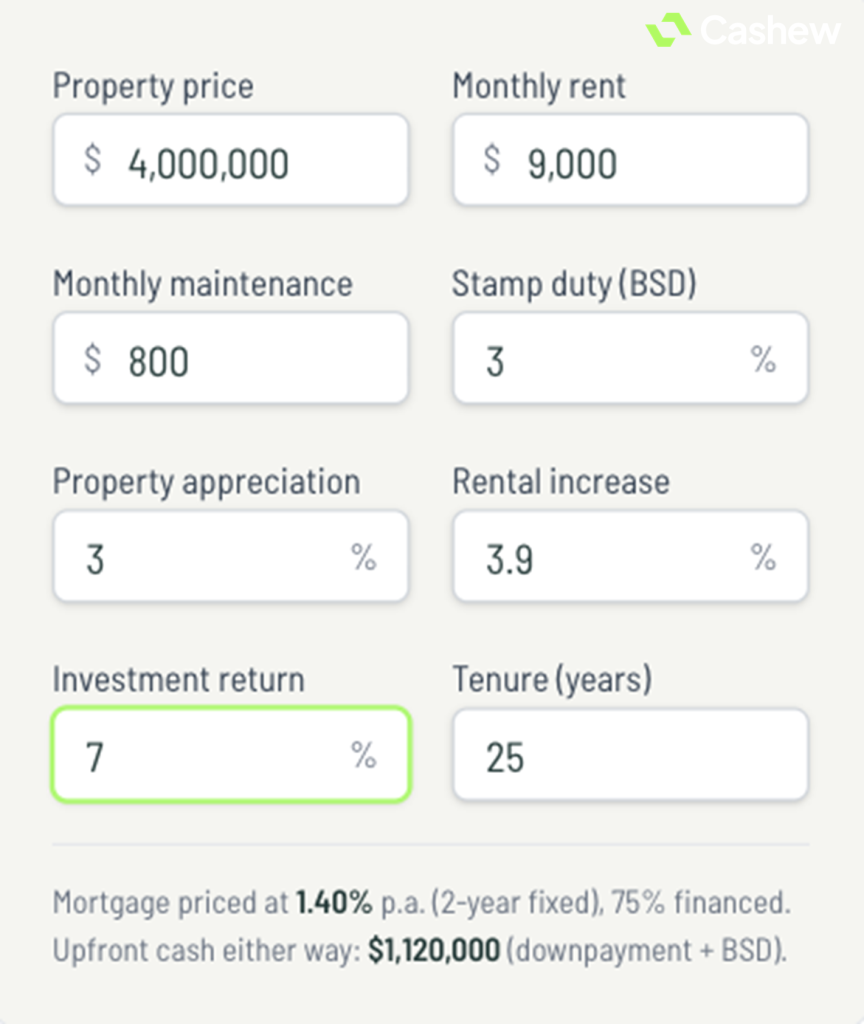

You enter the property price and your rent, set your own assumptions for appreciation, rent increases and investment return over the years you plan to stay, and it projects the net worth each path leaves you with.

Inputs you’ll need:

- Property price. The price the property is going for today, for the unit you’re actually considering.

- Monthly rent. What you’d pay to rent instead, whether that’s this same unit or a comparable home elsewhere.

- Property appreciation. Your annual growth assumption. Two to three percent is a sensible, conservative anchor. Condos appreciated by around 2.7%, while HDB resale prices grew by roughly 2.9% last year, according to CEIC data. But adjust it higher or lower for your property’s lease and location, and look at how similar nearby projects have actually moved rather than the market-wide average.

- Monthly maintenance. Condo MCST fees, or HDB conservancy charges, plus a buffer for upkeep.

- Stamp duty. Buyer’s Stamp Duty is tiered from 1 to 6 percent on the higher of price or valuation: 1 percent on the first 180,000 dollars, 2 percent on the next 180,000, 3 percent on the next 640,000, 4 percent on the next 500,000, and higher rates above that.

- Rental increase. Year-on-year rent growth, which is volatile. A reasonable rule of thumb is the long-run average: from 2001 to 2025, private residential rents rose about 3.9 percent a year on URA data.

- Investment return. A conservative estimate of what your downpayment plus stamp duty could earn if invested elsewhere instead.

- Tenure. How long you actually plan to hold the property.

Source: Cashew.sg, Rent vs Buy Calculator

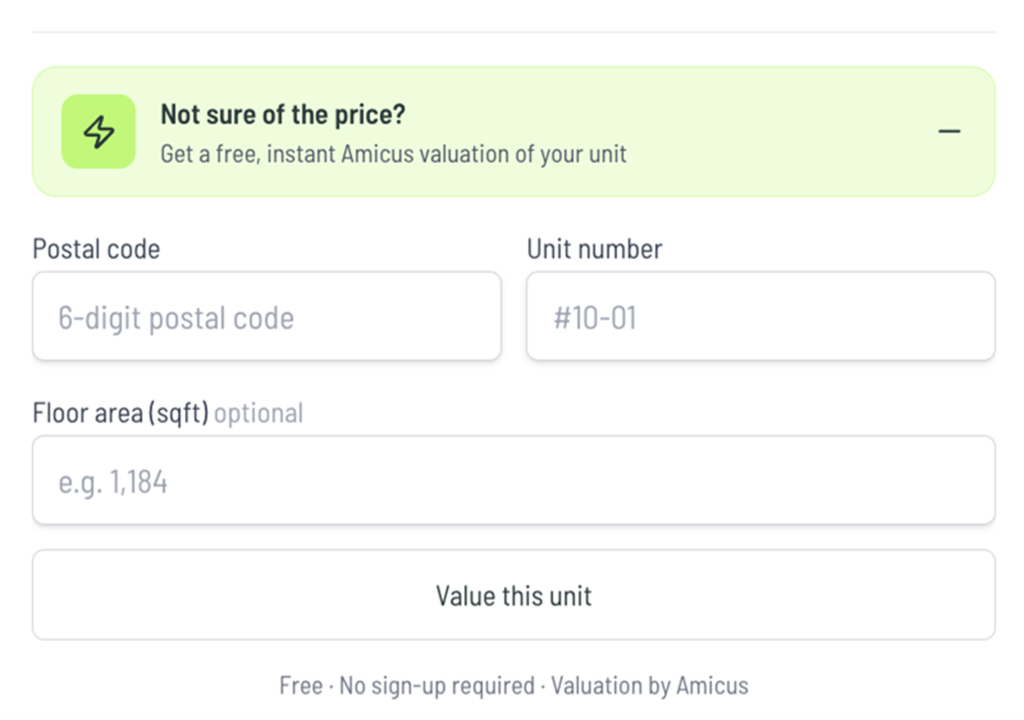

If you don’t have a price in mind, the same page has a free instant valuation tool: enter the postal code and unit for an independent estimate, immediately.

Source: Cashew.sg, Rent vs Buy Calculator

For the inputs in our worked example above, buying came out roughly 2 million dollars ahead.

Source: Cashew.sg, Rent vs Buy Calculator

For most people staying put, buying usually remains the right call. But “should I buy” is not the hard question in Singapore. The hard question is this property, at this price, on this lease, against what your money could otherwise do, over the years you’ll actually hold it. Get those right and ownership compounds quietly in your favour for decades.

Read Also: What Happens to Your Mortgage When You Sell and Buy a New Property?

Sebastian Sieber is the Founder of Cashew.sg, a digital mortgage platform in Singapore that uses AI and automation to help homeowners find and secure the right home loan. This article reflects the author’s personal views and does not constitute financial advice.