Corporate income tax is charged on a company’s income, which is calculated by total revenue, less operating costs. Some of the company’s operating costs falls into business expenses such as salary expense, or purchase of consumables. However, another form of operating costs come in the form of equipment which the company needs to operate. These are capital assets and are given a different tax treatment through capital allowances.

Read Also: How To Choose (Or Change) Your Company’s Financial Year End (FYE)

Capital Assets Differ From Other Business Expenses

Aside from being one-off purchases, capital assets differ from other business expenses in that it generally suffers from wear and tear with use and may eventually need to be disposed of and replaced as its useful lifespan is depleted. Assets may also be sold mid-way through its useful lifespan to be upgraded or to recoup capital.

This is in comparison to business expenses such as salaries, office rental, and purchase of consumables which generally do not depreciate and cannot be later sold to recoup capital.

Capital Assets are therefore given a different treatment under tax, where they are claimed for as capital allowances. Capital allowances still subtract from taxable income just like other tax deductions, but they are calculated differently.

Read Also: Complete Guide To Singapore Corporate Taxes: Tax Rates, Tax Rebates And Tax Exemptions

Qualifying Fixed Assets

In order to qualify for capital allowances, fixed assets must be ‘plant and machinery’ used in the company’s business. It needs to meet some specific requirements, but in general the fixed asset must:

- Not be something meant for resale.

- Is machinery that is used for the main business of the company.

- Is a part of the renovation or business premises (these are given different tax treatments).

Capital allowances can be claimed on motor vehicles except cars unless these cars are directly used as a main part of the company’s business. (e.g. in a car rental business)

Read Also: Best Business Laptops (From $2000) For Small And Medium Enterprises (SMEs)

Calculating Capital Allowances

Regardless of whether the assets were paid for in cash or through a loan, the company must claim for capital allowances in the year of assessment where the purchase was made. Thereafter, the company may write off the cost of the equipment using the following 3 methods:

- Over 1 year (For IT equipment, specific assets, and low-value assets only)

- Over 3 years

- Over prescribed working life of the asset

Writing off is the process where the in the eyes of the law, the value of the equipment is gradually reduced. The amount written off each year can be claimed as capital allowance, which is tax-deductible.

Write-Off In 1 Year

Computers, prescribed automation equipment (such as printers), and other low-value assets can be fully written off in 1 year, and capital allowances can be claimed on the value of the asset for that year of assessment.

For low-value assets, the value of each asset cannot exceed $5,000, and the value of all low-value assets purchased in the year cannot exceed $30,000.

Write-Off Over 3 Years

Companies can write off all types of assets over 3 years. In this option, the annual allowance that can be claimed each year is 1/3 the cost of the asset.

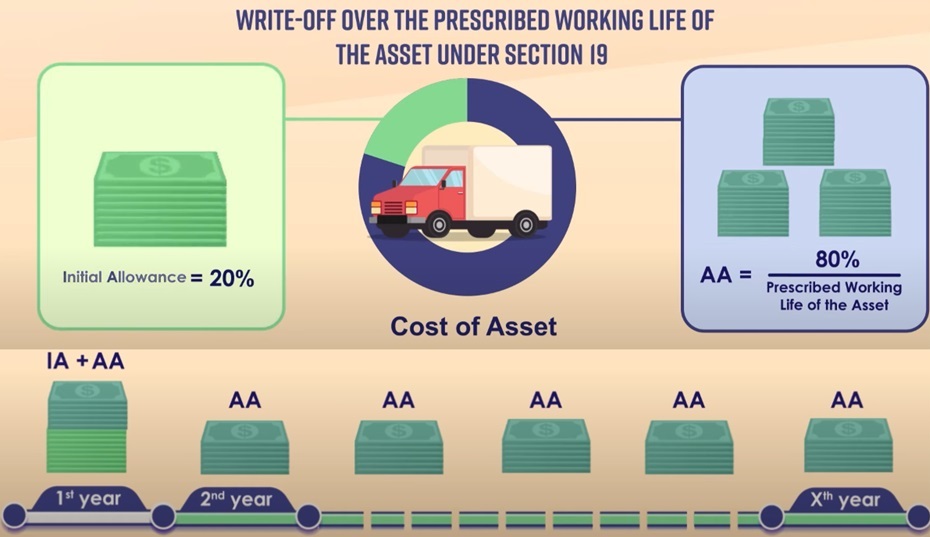

Write-Off Over The Prescribed Working Life The Asset

Companies can also choose to write off their assets over the prescribed working life of the asset.

In this option, the initial allowance is 20% of the asset’s value, and the annual allowance is 80% of the asset’s value divided by the prescribed working life of the asset. In the first year, the company can claim the initial allowance along with the annual allowance. In subsequent years, the company can claim the annual allowance.

Sale Of Assets

The total capital allowances the company is entitled to claim is the cost of the asset minus its sale price.

When the asset is sold, if the sale price is lower than the capital allowances that have not yet been utilised, a balancing allowance will be given to make up the difference. Vice versa, if the sale price is higher than the unutilised capital allowances, a balancing charge will be given instead, which will be added to taxable income.

Read Also: Where To Buy Or Sell Your Second-Hand Furniture When You Shift Offices

Asset Transfer

A company can opt to transfer fixed assets to a related company where there are 50% or more common shareholders.

In this case, the asset is treated as having been sold for a sum equal to the unutilised capital allowances of the asset immediately before the sale. The company taking over can claim the remaining capital allowances as if it purchased the asset for that price.

Companies Can Defer Capital Allowances

New companies or companies that are currently in a loss position can defer their capital allowances to be claimed in another year of assessment.

If a company could not fully utilise its capital allowances for the year, the remainder will be carried forward to offset taxable income in future years.

Read Also: From Loss Carry-Back Relief To BIPS: How To Save Corporate Income Tax In Singapore

Subscribe To The DollarsAndSense Business Pass

Enjoy what you are reading and want more? Join The DollarsAndSense Business Pass and unlock access to valuable tools, exclusive networking opportunities, and tap into the wisdom of industry experts to fuel your business expansion!