The Singapore economy is on the mend from COVID-19 – with GDP forecasted to grow 6% to 7% in 2021. Despite this, many companies continue to navigate the pandemic with caution, and there are smaller pockets of the economy still subdued and possible even shrinking.

This has resulted in a generally positive labour market. The Citizen unemployment rate has dropped from 4.9% in September 2020 to 3.7% today. However, this is still higher than pre-pandemic levels. On the other hand, retrenchments have actually fallen to below pre-pandemic levels after spiking during 2020.

As we can see in the chart above, there are about 2,000 retrenchments in the third quarter of 2021, this is lower than last quarter. In fact, the last time retrenchments in a single quarter came in lower than the current level was in 2011.

Nevertheless, retrenchments continue to be a topic relevant to every business and employee. In 2020, there were 26,110 retrenchments in total – which made it the top reason for employees left their job during the year. In 2021, there are already 6,610 retrenchments. Over the last 10 years, an average of over 14,000 retrenchments take place each year.

Read Also: 4 Things We Learned From Labour Market Report In 2Q 2021

Do Employers Have To Pay Retrenchment Benefits?

With the spike in the number of retrenchments in 2020, the Tripartite Partners – consisting the government (through MOM), unions (through NTUC) and employers (through SNEF) – updated their advisory on managing excess manpower and responsible retrenchments.

While retrenchment benefits are not inked in law, the tripartite advisory strongly encouraged employers to provide retrenchment benefits to their laid-off workers. Some of the guidelines provided include:

1. Employees who had worked for 2 years or more should be eligible for retrenchment benefits. Those who had worked for less than 2 years could be provided ex-gratia payments.

2. The prevailing norm is to pay a retrenchment benefit of 2 weeks to 1 month of salary for every year of service. This would also depend on the financial position of the company. Unionised companies would also have a stipulated retrenchment benefit in a collective agreement. The norm in such collective agreements is 1 month of salary for every year of service.

3. If the retrenchment exercise comes shortly after a salary cut, the salary prior to the cut should be used for the purpose of paying retrenchment benefits. This way, cuts would not be implemented just to reduce retrenchment benefit payouts for companies.

Read Also: MOM Responsible Retrenchments – Guideline For Companies To Be Fair And Decent

Are CPF Contributions Required For Retrenchment Benefits?

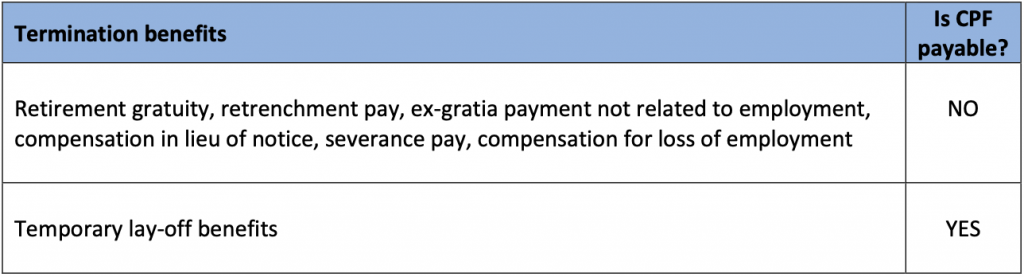

Employees have to pay CPF on wages that is paid to their employees. However, termination benefit or retrenchment benefit is typically not considered as compensation paid for services or work done. As such, CPF payments are not required.

However, it’s also important to distinguish the difference between a retrenchment and a temporary lay-off. This is because CPF contributions are still required for any benefits paid due to temporary lay-offs.

Read Also: 10 Types Of Employee Payments (Apart From Salary) That Businesses Need To Pay CPF For

A total of 128,860 workers were put on temporary lay-offs during 2020 – a huge number compared to previous years, mainly because of COVID-19 safe management measures.

A retrenchment means that the employee is let go.

A temporary lay-off is usually the result of the workplace shutting down for a designated period. Most employees are affected, while some administrative functions will typically be performed. In such cases, employers may:

- Request employees use their annual leave during this period. The tripartite advisory gives the example of up to 50% of their annual leaves be used for this purpose

- Implement a layoff period. Again, the tripartite advisory states that this should not exceed one month in any one instance

- Pay affected employees a portion of their wages during the lay-off period. The tripartite advisory puts this figure at no less than 50%

Paying employees a temporary lay-off benefit is quite different to a retrenchment benefit as employees would be expected to come back to work after the lay-off period. Hence, this is most likely why CPF contributions – both employer’s and employee’s contributions – would be required.

Read Also: Complete Guide To Employer’s CPF Contributions In Singapore

Do Employees Have To Pay Income Tax On Retrenchment Benefits?

Any payments that an employee gets CPF contributions for are usually also taxable. However, there may also be other types of payments that employees do not get CPF contributions for that they also have to pay income tax on. These may include certain allowances and benefits.

Read Also: 10 Types Of Company Benefits That Employees Have To Pay Income Tax On

In general, employees do not have to pay income tax on retrenchment benefits. However, any temporary lay-off benefits, which also requires CPF contributions as explained above, would also require employees to pay income taxes.

IRAS also makes clear that compensation for the less of employment (i.e. retrenchment benefits) are not taxable because they are “capital receipts”. Other payments such as salary in lieu of notice, ex-gratia and gratuity for past services are not considered payment for loss of employment, and therefore taxable. IRAS states that companies performing retrenchment exercises should check with them on the taxability of payments once the retrenchment package has been finalised. Once IRAS confirms the taxability of the payments, employers only need to declare the taxable components on the Form IR8A.

For employers on the Auto-Inclusion Scheme (AIS), this is “item d4” on Form IR8A. For employers participating in AIS, this is “item d4(i)” and “item d4(ii)” of Form IR8E.

Read Also: How To Calculate Leave Encashment Or Salary-In-Lieu Of Notice Period For Your Employees

Retrenchment support such as outplacement support are not taxable either. These kinds of support usually include the provision of counselling and moral support for affected employees. According to IRAS, such support is not taxable if all the following factors are met:

- The outplacement support is provided as part of a retrenchment package to compensate for loss of employment and is only available to employees who are retrenched;

- The only expense incurred by the employer to provide the outplacement support is the fees paid to the outplacement agents or cost incurred to provide the outplacement support; and

- Employees who choose not to accept the support package are not entitled to other compensation in lieu, whether in cash or otherwise.

If these conditions are not met, the outplacement support may be considered taxable. Hence, this is why IRAS recommends companies to check with it.

Read Also: Retrenching Some Staff VS Pay Cut For All: Pros And Cons Of Each Cost-Saving Method

Subscribe To The DollarsAndSense Business Pass

Enjoy what you are reading and want more? Join The DollarsAndSense Business Pass and unlock access to valuable tools, exclusive networking opportunities, and tap into the wisdom of industry experts to fuel your business expansion!