This commentary was contributed by Timothy Ho, Managing Editor of DollarsAndSense. Drop us a message to share your thoughts on entrepreneurship, the Singapore startup scene, or the gig economy.

Disruption is a big and commonly used word over the past decade. From entrepreneur networking sessions, startup pitch decks to government outreach programs, you be hard-pressed to have a conversation about business today without someone inevitably bringing up disruption.

Because disruption is synonymous with change, many of us start to overlook just how disruptive disruption can be for us. It’s even cited by many with good intent as the reason why we must continue innovating and learning, just like how our parents used to tell us to study hard in order to get a good job.

But disruption isn’t natural evolvement. It’s largely unpredictable. Often, it’s not even welcomed by certain groups of people.

Disruption Is Unlikely To Come From Incumbents In The Same Industry

During one of our lunchtime conversations, some of us were discussing the topic of disruption in the financial industry. Here’s what I think:

True disruption for an industry isn’t likely to come from incumbents in the industry.

Think about it. Incumbents are companies that have solidified their position after decades of hard work. Most of these companies have done well, offer products and services which their customers are happy…or at least satisfied with. Incumbents want to enjoy improvements over time (because no business should ever be contended with the status quo) but natural evolvement shouldn’t be confused as disruption.

Technically, incumbents are in the best position to disrupt themselves. They have more money, existing customers, sufficient talent and business partners that they can leverage on to build something different – but only if they want to.

The reason why incumbents won’t disrupt themselves is precisely because they are incumbents. There is no financially logical reason to be spending tons of money to be killing off your own profits.

Just ask yourself this. Would Grab have spent billions of dollars in marketing and product development to acquire drivers and consumers if they started off in Comfort Delgro’s position?

Effective Disruption Can Easily Come From Existing Incumbents In A Different Industry

New markets tend to be created by startups. Social media is an example. While they have now disrupted the advertising world and change the way media companies operate, independently owned media companies were never likely to be the ones building social media businesses.

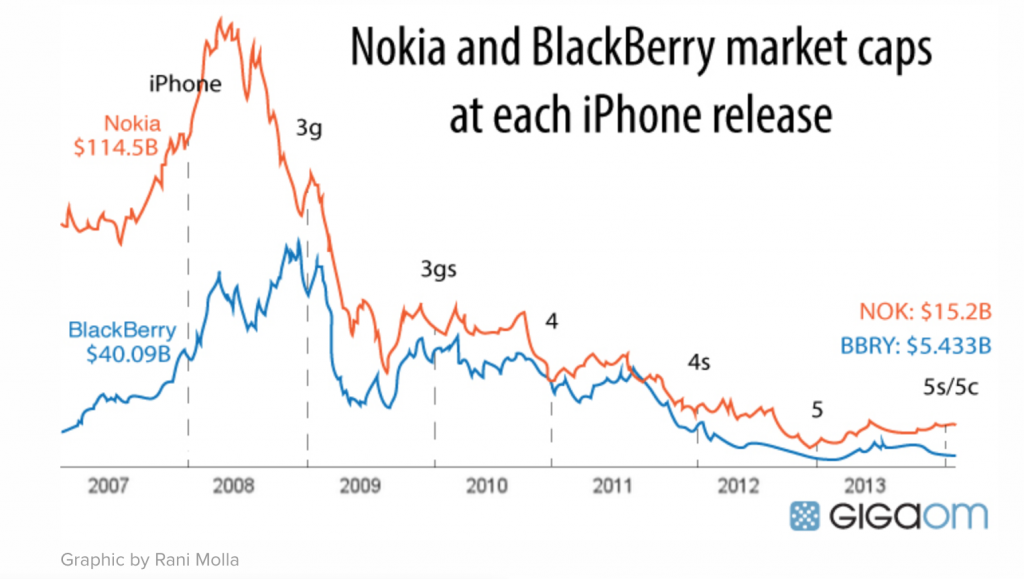

But what about the likes of Nokia who were operating in an established, growing market?

Once a company with a market capitalization of $250 billion, it’s worth noting that Nokia’s valuation actually peaked when the iPhone was first launched. If anything, Nokia should have been in prime position to capitalise on the smartphone boom that was to come.

They couldn’t do it. Neither could BlackBerry, which was the world’s first innovator of the Smartphone. Nor Motorola, which invented the mobile phone.

Instead, a good computer company and a leading search engine portal found themselves taking the lion’s share of the market. Sure, Apple and Google were already leaders in their respective space but that’s exactly my point, the biggest potential disruptor in your industry today is more likely to be an incumbent you already know from another industry, than a startup.

This is why I think it’s worth paying very close attention to some of the potential applicants for the digital bank license in Singapore. This includes Singtel (an established telco company), Grab (a unicorn startup/super app) and Razer (a leading gaming company).

These established incumbents from other industries have 1) the funding to pull it off, 2) a market it wants to disrupt without needing to worry about cannibalizing its own sales, 3) the capabilities to build a team from scratch like a startup and 4) the right management and control in place so that it can scale up its operation quickly when it wants to.

Regulation At The Cost Of Innovation

Similar to healthcare, the banking industry is a tightly regulated industry (for good reasons) and typically that becomes an advantage for incumbents.

The taxi industry wasn’t regulated much and it was easily disrupted by Uber & Grab

The travel industry didn’t have to be regulated and some of the biggest players today are AirBnb, Expedia, Skyscanner and Booking.com.

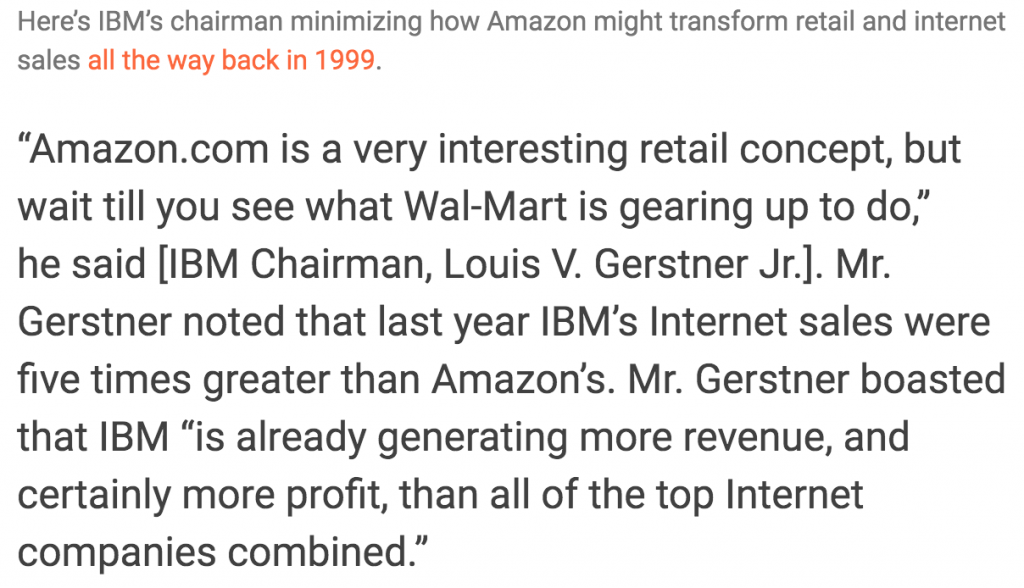

The book industry didn’t need to be regulated and it produced Amazon, a bookstore which went on to become the most valuable company in the world today. Amazon subsequently went out to disrupt other ‘bigger’ industries such as groceries, video distribution, commerce and web services.

If anyone were to disrupt a bank in Singapore, it’s unlikely to be a foreign bank or even a FinTech startup, but likely an established player from another industry.

Subscribe To The DollarsAndSense Business Pass

Enjoy what you are reading and want more? Join The DollarsAndSense Business Pass and unlock access to valuable tools, exclusive networking opportunities, and tap into the wisdom of industry experts to fuel your business expansion!